Answered step by step

Verified Expert Solution

Question

1 Approved Answer

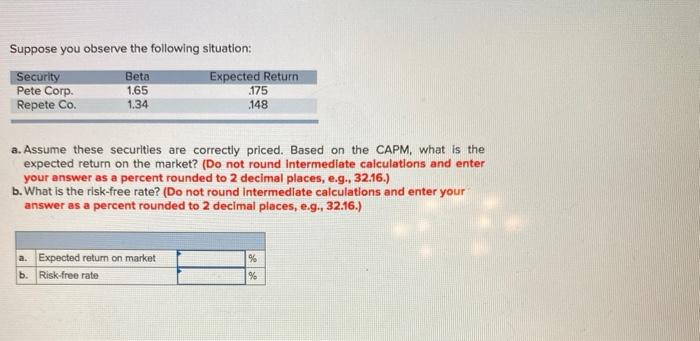

Suppose you observe the following situation: Security Beta Expected Return Pete Corp. 1.65 .175 Repete Co. 1.34 148 a. Assume these securities are correctly priced.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sound Investing, Chapter 10 - One-Time Charges And Other Format Fakes

Authors: Kate Mooney

2nd Edition

0071719326, 9780071719322