Answered step by step

Verified Expert Solution

Question

1 Approved Answer

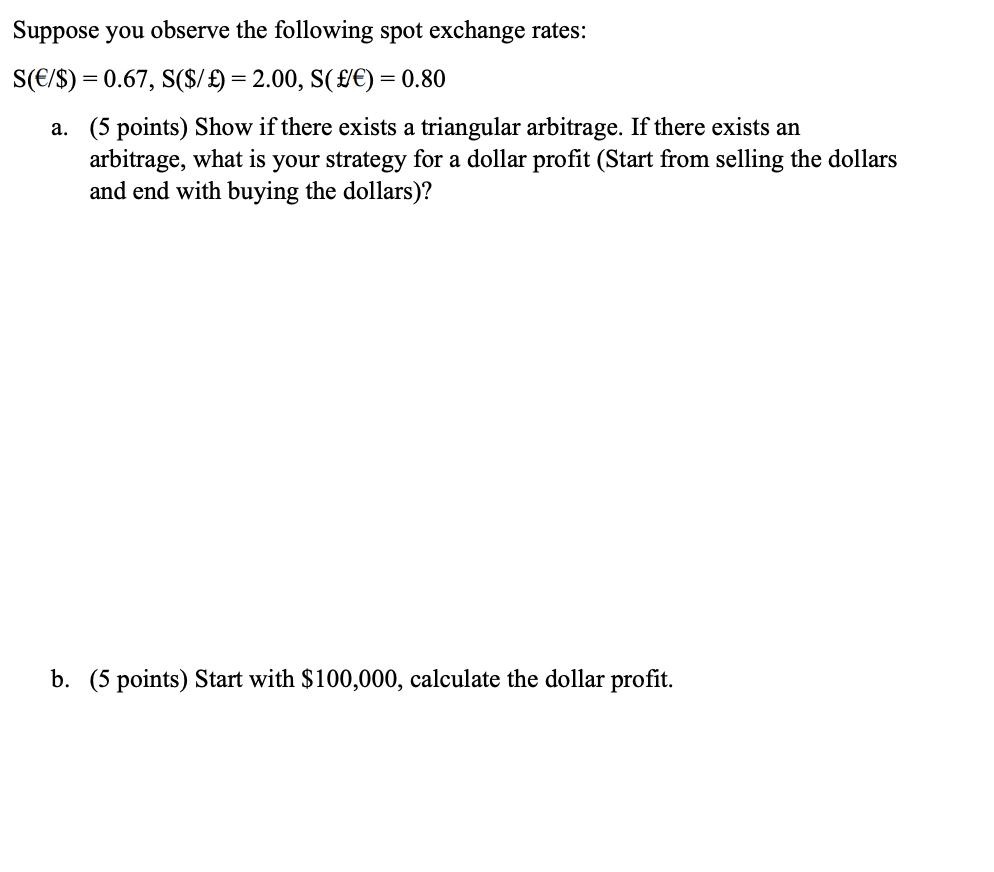

Suppose you observe the following spot exchange rates: S(/$) = 0.67, S($/ ) = 2.00, S( /C) = 0.80 a. (5 points) Show if there

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Elementary Introduction To Stochastic Interest Rate Modeling

Authors: Nicolas Privault

1st Edition

9812832734,9813107308