Question

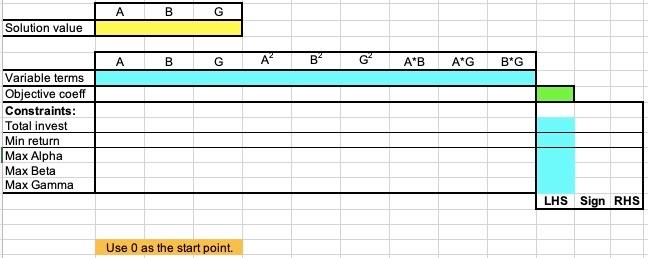

Susan Jones would like her investment portfolio to be selected from a combination of three stocks Alpha, Beta, and Gamma. Let variables A, B, and

- Susan Jones would like her investment portfolio to be selected from a combination of three stocks Alpha, Beta, and Gamma. Let variables A, B, and G denote the percentages of the portfolio devoted to Alpha, Beta, and Gamma, respectively. Susans objective is to minimize the variance of the portfolios return, given by the following function:

The expected returns for Alpha, Beta, and Gamma are 15%, 11%, and 9%, respectively. Susan wants the expected return for the total portfolio to be at least 10%. No individual stock can constitute more than 70% of the portfolio. Formulate this portfolio selection problem and solve using Excel

PLEASE USE TEMPLATE ABOVE. THANK YOU.

PLEASE USE TEMPLATE ABOVE. THANK YOU.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Forensic And Investigative Accounting

Authors: Larry Crumbley, Lester E. Heitger, G. Stevenson Smith

4th Edition

0808021435, 9780808021438