Answered step by step

Verified Expert Solution

Question

1 Approved Answer

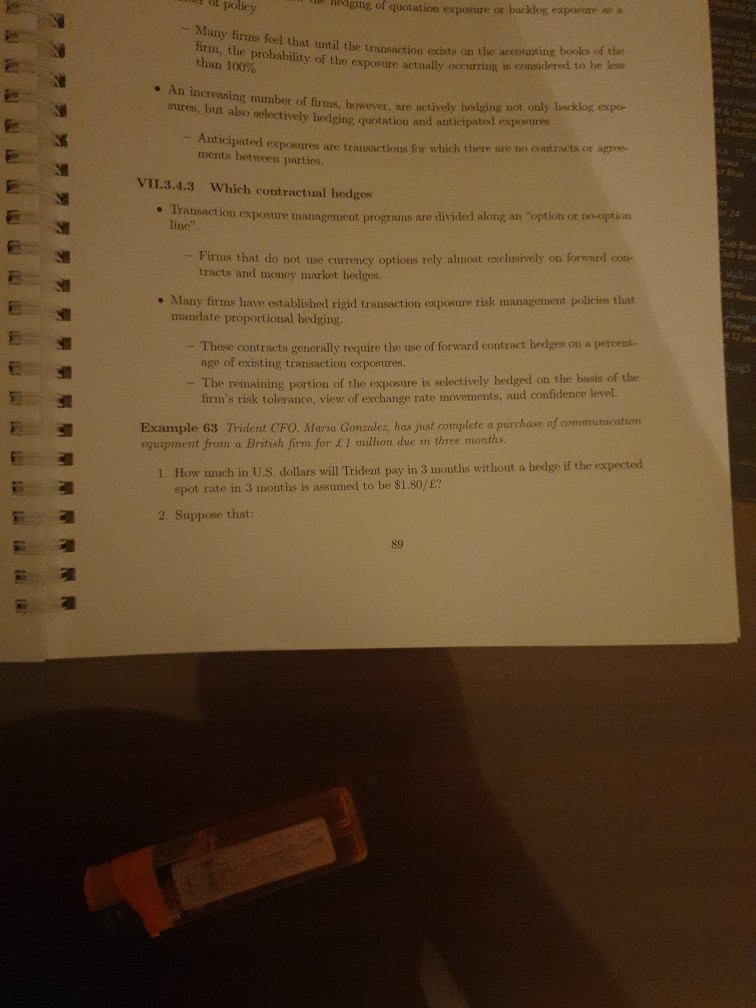

t policy hedging of quotation exposure or backlog exposurp -Many firms feel that until the transaction exists on the arcour , the probability of the

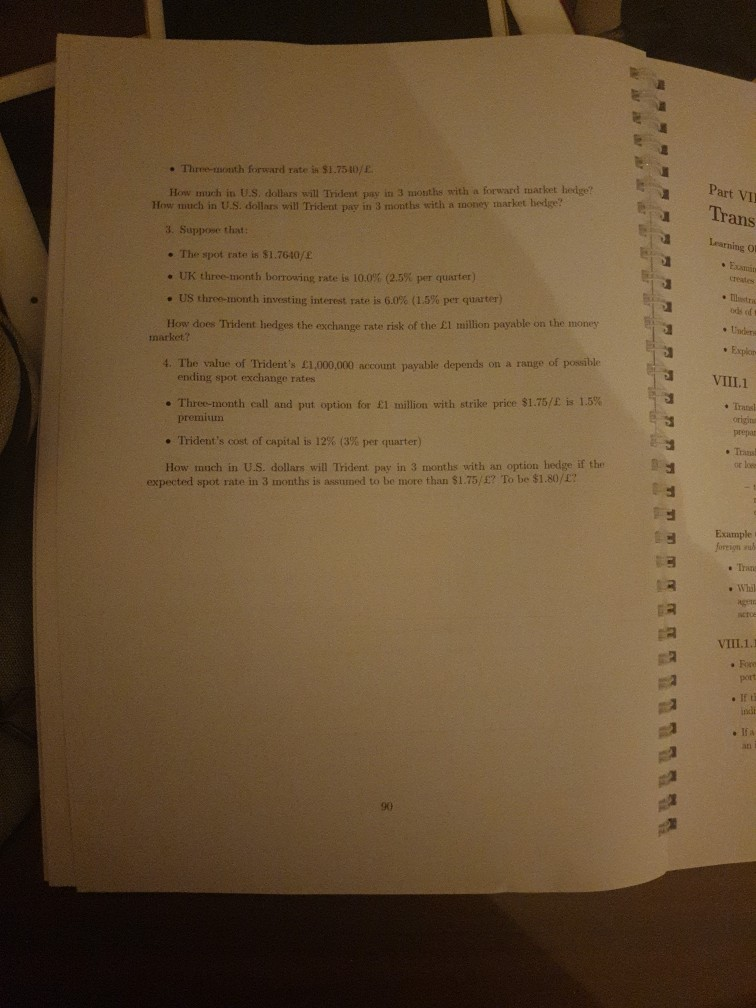

t policy hedging of quotation exposure or backlog exposurp -Many firms feel that until the transaction exists on the arcour , the probability of the exposure actually occurring is s than 100% . An increasing number of firns, however, are actively hedging, not only backlog expo- sures, but also selectively hedging quotation and anticipated expowures - Antici ted exposures are transactions for which there are no contracts or agree- ments between parties VII.3.4.3 Which contractual hedges . Transaction tion exposure management programs are divided along an "option or no-option line" - Firms that do not tuse currency options rely almost exclusively on forward co- e Many firms have established rigid transaction exposure risk management policies that These contracts generally require the use of forward contract hedges on a percent- tion of the exposure is selectively hedged on the basis of the Example 63 Trident CFO, Maria Gonzale, has just complete a purchase of commuucation tracts and money market hedges. mandate proportional hedging age of existing transaction exposures The remaining por firm's risk tolerance, view of exchange rate movements, and confidence level. equipment from a British firm for 1 million due in three months. 1. How much in U.S, dollars wil l Trident pay in 3 months without a hedge if the expected spot rate in 3 months is assumed to be $1.80/E 2. Suppose that 89 Three-tonth forward rate in $1.7510/E How much in U.S, dollars will Trident pay in 3 mosths with a forward market hedge? Part VII Trans How much in U.S. dollars will Trident pay in 3 months with a money market hesdge? 3. Suppose that: . The spot rate is $1.7610/E creates UK three-month borrowing rate is 10.0% (2.5% per quarter) US three-month investing interest rate is 6.0% (1.5% per quarter) How does Tident hedges the exchange rate risk of the 1 million payable on the money 4. The value of Trident's 1,000,000 account payable depends on a range of possible Eds market? VIII.1 ending spot exchange rates . Three-month call and put option for 1 million with strike price $1.75/E is 1.5% premiuun Trident's cost of capital is 12% (3% per quarter) How much in U.S. dollars will Trident pay in 3 months with an option hedge if the or los expected spot rate in 3 months is assumed to be more than S1.75/5? To be $1.80/E Example foreign suh . Tran Whi . Fe 90 t policy hedging of quotation exposure or backlog exposurp -Many firms feel that until the transaction exists on the arcour , the probability of the exposure actually occurring is s than 100% . An increasing number of firns, however, are actively hedging, not only backlog expo- sures, but also selectively hedging quotation and anticipated expowures - Antici ted exposures are transactions for which there are no contracts or agree- ments between parties VII.3.4.3 Which contractual hedges . Transaction tion exposure management programs are divided along an "option or no-option line" - Firms that do not tuse currency options rely almost exclusively on forward co- e Many firms have established rigid transaction exposure risk management policies that These contracts generally require the use of forward contract hedges on a percent- tion of the exposure is selectively hedged on the basis of the Example 63 Trident CFO, Maria Gonzale, has just complete a purchase of commuucation tracts and money market hedges. mandate proportional hedging age of existing transaction exposures The remaining por firm's risk tolerance, view of exchange rate movements, and confidence level. equipment from a British firm for 1 million due in three months. 1. How much in U.S, dollars wil l Trident pay in 3 months without a hedge if the expected spot rate in 3 months is assumed to be $1.80/E 2. Suppose that 89 Three-tonth forward rate in $1.7510/E How much in U.S, dollars will Trident pay in 3 mosths with a forward market hedge? Part VII Trans How much in U.S. dollars will Trident pay in 3 months with a money market hesdge? 3. Suppose that: . The spot rate is $1.7610/E creates UK three-month borrowing rate is 10.0% (2.5% per quarter) US three-month investing interest rate is 6.0% (1.5% per quarter) How does Tident hedges the exchange rate risk of the 1 million payable on the money 4. The value of Trident's 1,000,000 account payable depends on a range of possible Eds market? VIII.1 ending spot exchange rates . Three-month call and put option for 1 million with strike price $1.75/E is 1.5% premiuun Trident's cost of capital is 12% (3% per quarter) How much in U.S. dollars will Trident pay in 3 months with an option hedge if the or los expected spot rate in 3 months is assumed to be more than S1.75/5? To be $1.80/E Example foreign suh . Tran Whi . Fe 90

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sales Audit The Sales Managers Playbook For Getting Control Of The Selling Cycle And Improving Results

Authors: Corey Hutchison

1st Edition

0595421342, 978-0595421343