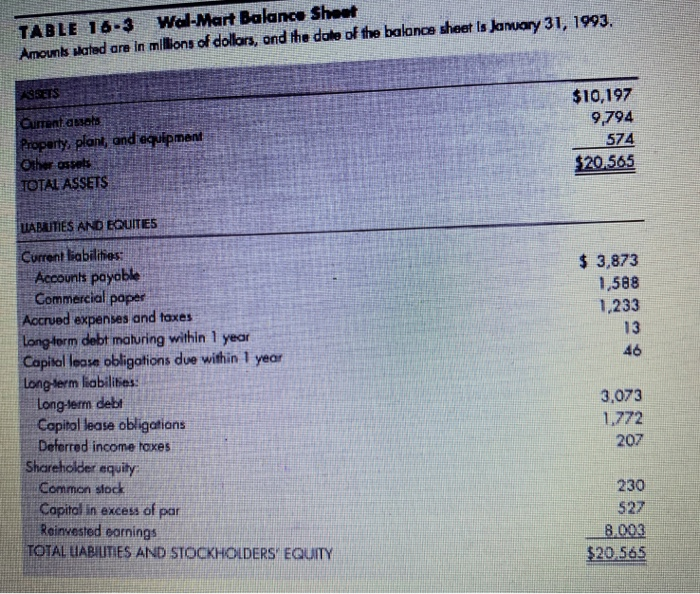

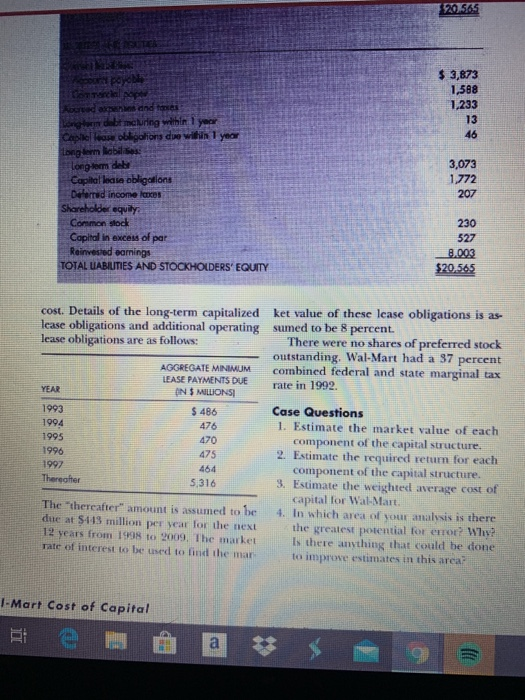

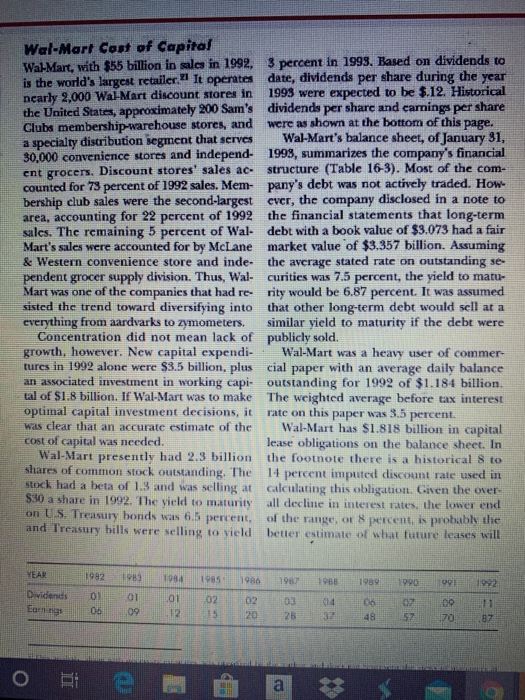

TABLE 16-3 Wal-Mart Balance Shoot Amounis slated are in millions of dollars, and the dole of the balance sheet Is January 31, 1993, $10,197 FASSETS Current angels Property, plant, and Other ossels TOTAL ASSETS 9,794 574 $20.565 $ 3,873 1,588 1,233 UABRITIES AND EQUITIES Current liabilities Accounts payable Commercial paper Accrued expenses and taxes long form debt maturing within 1 year Capital lease obligations due within 1 year Long term liabilities: long-term debt Capital lease obligations Deferred income taxes Shareholder equity Common stock Capital in excess of par Reinvested cornings TOTAL UABIUTIES AND STOCKHOLDERS' EQUITY 3,073 1,772 207 230 8.003 $20.565 3. Estimate the weighted average cost of capital lor Wal-Mart. 20.565 RE $ 3,873 1,568 1,233 ocedarenin and more keng tar debt meluring within 1 Caple les obligations due within 1 tongdern liebils long-term debe Capital lease obligations Deferred income taxes Shareholder equity Common stock Capital in excess of par Rainvested earnings TOTAL UABILITIES AND STOCKHOLDERS' EQUITY 230 527 8.003 $20,565 cost. Details of the long-term capitalized ket value of these lease obligations is as- Icase obligations and additional operating sumed to be 8 percent. lease obligations are as follows: There were no shares of preferred stock outstanding, Wal-Mart had a 37 percent AGGREGATE MINIMUM combined federal and state marginal tax LEASE PAYMENTS DUE YEAR IN $ MILLIONS rate in 1992. 1993 $ 486 Case Questions 1994 476 1. Estimate the market value of each 1995 470 component of the capital structure 1996 475 2. Estimate the required retum for each 1997 464 component of the capital structure. Thereafter 5,316 3. Estimate the weighted average cost of capital for Wal-Mart. The thereafter" amount is assumed to be 4. in which area of your analysis is there due at 5443 million per year for the next 12 years from 1998 to 2009. The market the greatest potential for error? Why? Is there anything that could be done Tate of interest to be used to find the mar to improve estimates in this area 1- Mart cost of capital e a * = 9 Wal-Mart Cost of Capital Wal-Mart, with $55 billion in sales in 1992. 3 percent in 1993. Based on dividends to is the world's largest retailer. It operates date, dividends per share during the year ncarly 2,000 Wal-Mart discount stores in 1993 were expected to be $.12. Historical the United States, approximately 200 Sam's dividende per share and carings per share Clubs membership-warehouse stores, and were as shown at the bottom of this page. a specialty distribution segment that serves Wal-Mart's balance sheet, of January 31, 30,000 convenience stores and independ- 1998, summarizes the company's financial ent grocers. Discount stores' sales ac structure (Table 16-3). Most of the com- counted for 78 percent of 1992 sales. Mem- pany's debt was not actively traded. How bership club sales were the second-largest ever, the company disclosed in a note to area, accounting for 22 percent of 1992 the financial statements that long-term sales. The remaining 5 percent of Wal- debt with a book value of $3.073 had a fair Mart's sales were accounted for by McLane market value of $3.357 billion. Assuming & Western convenience store and inde. the average stated rate on outstanding se pendent grocer supply division. Thus, Wal- curities was 7.5 percent, the yield to matu- Mart was one of the companies that had re- rity would be 6.87 percent. It was assumed that other long-term debt would sell at a everything from aardvarks to zmometers. similar yield to maturity if the debt were Concentration did not mean lack of publicly sold. growth, however. New capital expendi- Wal-Mart was a heavy user of commer- tures in 1992 alone were $3.5 billion, plus cial paper with an average daily balance an associated investment in working capi- outstanding for 1992 of $1.184 billion. tal of $1.8 billion. If Wal-Mart was to make the weighted average before tax interest optimal capital investment decisions, it rate on this paper was 3.5 percent. was clear that an accurate estimate of the Wal-Mart has $1.818 billion in capital cost of capital was needed. lease obligations on the balance sheet. In Wal-Mart presently had 2.3 billion the footnote there is a historical 8 to shares of common stock outstanding. The 14 percent imputer discount rate used in stock had a beta of 1.3 and was selling at calculating this obligation. Given the over- $30 a share in 1992. The yield to maturity all decline in interest rates, the lower end on U.S. Treasury bonds was 6.5 percent of the range, or 8 percent, is probably the and Treasury bills were selling to vield better estimate of what future leases will 1989 1990 DE 19 BAR .982 Dividends 0 Earnings 06 983 0 1 .09 1984 01 .12 1985 1985 02 15 1986 02 20 1987 03 25 1988 04 02 57 70 - TABLE 16-3 Wal-Mart Balance Shoot Amounis slated are in millions of dollars, and the dole of the balance sheet Is January 31, 1993, $10,197 FASSETS Current angels Property, plant, and Other ossels TOTAL ASSETS 9,794 574 $20.565 $ 3,873 1,588 1,233 UABRITIES AND EQUITIES Current liabilities Accounts payable Commercial paper Accrued expenses and taxes long form debt maturing within 1 year Capital lease obligations due within 1 year Long term liabilities: long-term debt Capital lease obligations Deferred income taxes Shareholder equity Common stock Capital in excess of par Reinvested cornings TOTAL UABIUTIES AND STOCKHOLDERS' EQUITY 3,073 1,772 207 230 8.003 $20.565 3. Estimate the weighted average cost of capital lor Wal-Mart. 20.565 RE $ 3,873 1,568 1,233 ocedarenin and more keng tar debt meluring within 1 Caple les obligations due within 1 tongdern liebils long-term debe Capital lease obligations Deferred income taxes Shareholder equity Common stock Capital in excess of par Rainvested earnings TOTAL UABILITIES AND STOCKHOLDERS' EQUITY 230 527 8.003 $20,565 cost. Details of the long-term capitalized ket value of these lease obligations is as- Icase obligations and additional operating sumed to be 8 percent. lease obligations are as follows: There were no shares of preferred stock outstanding, Wal-Mart had a 37 percent AGGREGATE MINIMUM combined federal and state marginal tax LEASE PAYMENTS DUE YEAR IN $ MILLIONS rate in 1992. 1993 $ 486 Case Questions 1994 476 1. Estimate the market value of each 1995 470 component of the capital structure 1996 475 2. Estimate the required retum for each 1997 464 component of the capital structure. Thereafter 5,316 3. Estimate the weighted average cost of capital for Wal-Mart. The thereafter" amount is assumed to be 4. in which area of your analysis is there due at 5443 million per year for the next 12 years from 1998 to 2009. The market the greatest potential for error? Why? Is there anything that could be done Tate of interest to be used to find the mar to improve estimates in this area 1- Mart cost of capital e a * = 9 Wal-Mart Cost of Capital Wal-Mart, with $55 billion in sales in 1992. 3 percent in 1993. Based on dividends to is the world's largest retailer. It operates date, dividends per share during the year ncarly 2,000 Wal-Mart discount stores in 1993 were expected to be $.12. Historical the United States, approximately 200 Sam's dividende per share and carings per share Clubs membership-warehouse stores, and were as shown at the bottom of this page. a specialty distribution segment that serves Wal-Mart's balance sheet, of January 31, 30,000 convenience stores and independ- 1998, summarizes the company's financial ent grocers. Discount stores' sales ac structure (Table 16-3). Most of the com- counted for 78 percent of 1992 sales. Mem- pany's debt was not actively traded. How bership club sales were the second-largest ever, the company disclosed in a note to area, accounting for 22 percent of 1992 the financial statements that long-term sales. The remaining 5 percent of Wal- debt with a book value of $3.073 had a fair Mart's sales were accounted for by McLane market value of $3.357 billion. Assuming & Western convenience store and inde. the average stated rate on outstanding se pendent grocer supply division. Thus, Wal- curities was 7.5 percent, the yield to matu- Mart was one of the companies that had re- rity would be 6.87 percent. It was assumed that other long-term debt would sell at a everything from aardvarks to zmometers. similar yield to maturity if the debt were Concentration did not mean lack of publicly sold. growth, however. New capital expendi- Wal-Mart was a heavy user of commer- tures in 1992 alone were $3.5 billion, plus cial paper with an average daily balance an associated investment in working capi- outstanding for 1992 of $1.184 billion. tal of $1.8 billion. If Wal-Mart was to make the weighted average before tax interest optimal capital investment decisions, it rate on this paper was 3.5 percent. was clear that an accurate estimate of the Wal-Mart has $1.818 billion in capital cost of capital was needed. lease obligations on the balance sheet. In Wal-Mart presently had 2.3 billion the footnote there is a historical 8 to shares of common stock outstanding. The 14 percent imputer discount rate used in stock had a beta of 1.3 and was selling at calculating this obligation. Given the over- $30 a share in 1992. The yield to maturity all decline in interest rates, the lower end on U.S. Treasury bonds was 6.5 percent of the range, or 8 percent, is probably the and Treasury bills were selling to vield better estimate of what future leases will 1989 1990 DE 19 BAR .982 Dividends 0 Earnings 06 983 0 1 .09 1984 01 .12 1985 1985 02 15 1986 02 20 1987 03 25 1988 04 02 57 70