Answered step by step

Verified Expert Solution

Question

1 Approved Answer

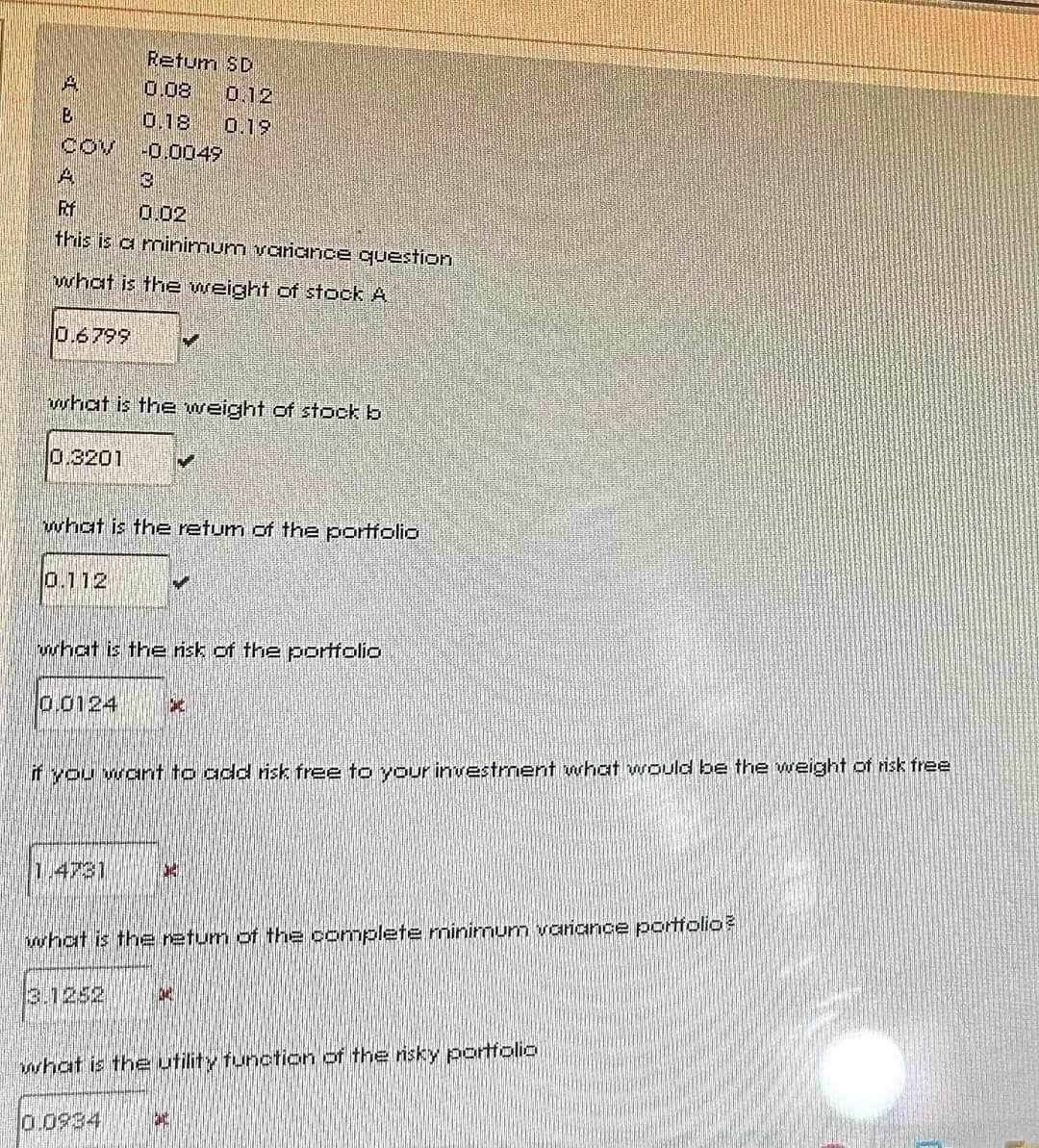

table [ [ , Retum,SD ] , [ A , 0 . 0 8 , 0 . 1 2 ] , [ E ,

tableRetum,SDE

this is a minimum variance question

what is the weight of stock

what is the weight of stack b

what is the retum of the portfolig

a

what is the risk of the portfolio

if you want to add risk free to your investment what would be the weight of risk tree

what is the retum of the pomplete minimum variance portioliae

what is the ufility function of the risky portfolig

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Capital Markets Institutions Instruments And Risk Management

Authors: Frank J. Fabozzi

5th Edition

0262029480, 9780262029483