Answered step by step

Verified Expert Solution

Question

1 Approved Answer

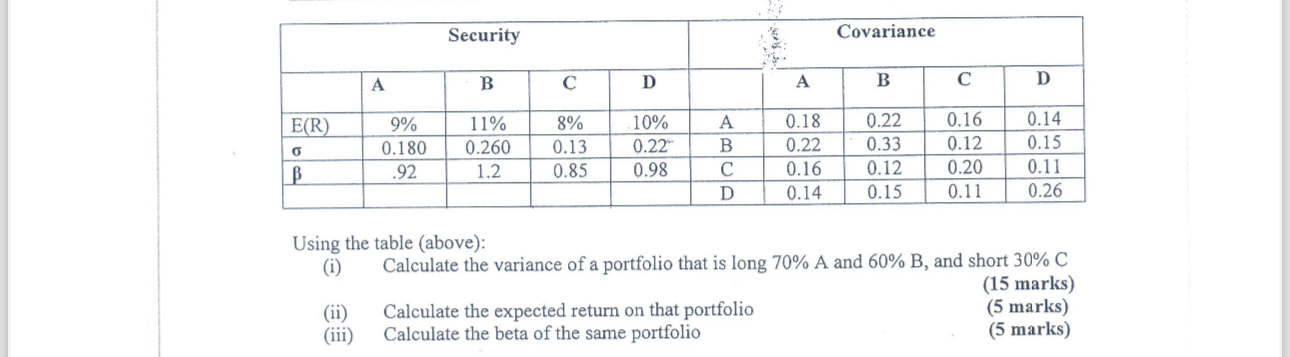

table [ [ Security , Covariance, ] , [ , A , B , C , D , , A , B , C

tableSecurityCovariance,ABCDABCDABCD

Using the table above:

i Calculate the variance of a portfolio that is long A and and short

ii Calculate the expected return on that portfolio

marks

iii Calculate the beta of the same portfolio

marks

marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Practical Guide To Quantitative Finance Interviews

Authors: Xinfeng Zhou

1st Edition

1735028800, 978-1735028804