Question

Thank you in advance, help is much appreciated! (a) should equal -7.0459%, (b) should equal -8.8640%, and (c) should equal -14.6459%, I'm just not sure

Thank you in advance, help is much appreciated!

Thank you in advance, help is much appreciated!

(a) should equal -7.0459%, (b) should equal -8.8640%, and (c) should equal -14.6459%, I'm just not sure how to solve for these answers, particularly the first one.

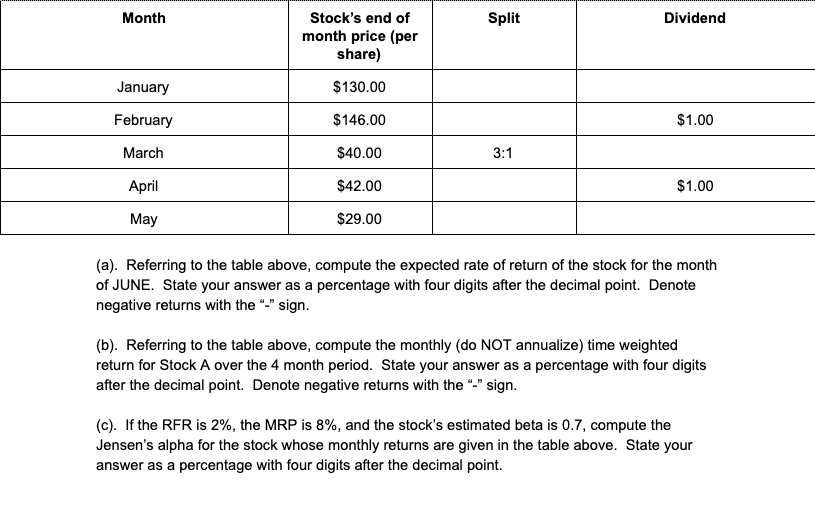

Month Split Dividend Stock's end of month price (per share) January $130.00 February $146.00 $1.00 March $40.00 April $42.00 $1.00 May $29.00 (a). Referring to the table above, compute the expected rate of return of the stock for the month of JUNE. State your answer as a percentage with four digits after the decimal point. Denote negative returns with the "-" sign. (b). Referring to the table above, compute the monthly (do NOT annualize) time weighted return for Stock A over the 4 month period. State your answer as a percentage with four digits after the decimal point. Denote negative returns with the "-" sign. (c). If the RFR is 2%, the MRP is 8%, and the stock's estimated beta is 0.7, compute the Jensen's alpha for the stock whose monthly returns are given in the table above. State your answer as a percentage with four digits after the decimal point. Month Split Dividend Stock's end of month price (per share) January $130.00 February $146.00 $1.00 March $40.00 April $42.00 $1.00 May $29.00 (a). Referring to the table above, compute the expected rate of return of the stock for the month of JUNE. State your answer as a percentage with four digits after the decimal point. Denote negative returns with the "-" sign. (b). Referring to the table above, compute the monthly (do NOT annualize) time weighted return for Stock A over the 4 month period. State your answer as a percentage with four digits after the decimal point. Denote negative returns with the "-" sign. (c). If the RFR is 2%, the MRP is 8%, and the stock's estimated beta is 0.7, compute the Jensen's alpha for the stock whose monthly returns are given in the table above. State your answer as a percentage with four digits after the decimal pointStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Marketing For Financial Advisors

Authors: Eric Bradlow, Keith Niedermeier, Patti Williams

1st Edition

0071605142, 978-0071605144