Thanks God Bless.

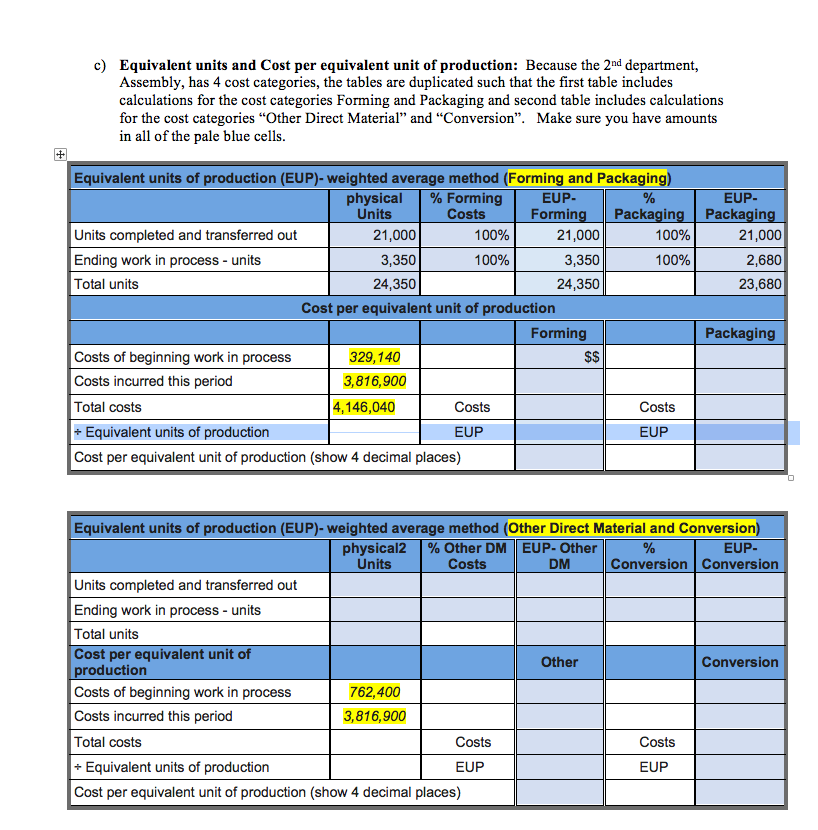

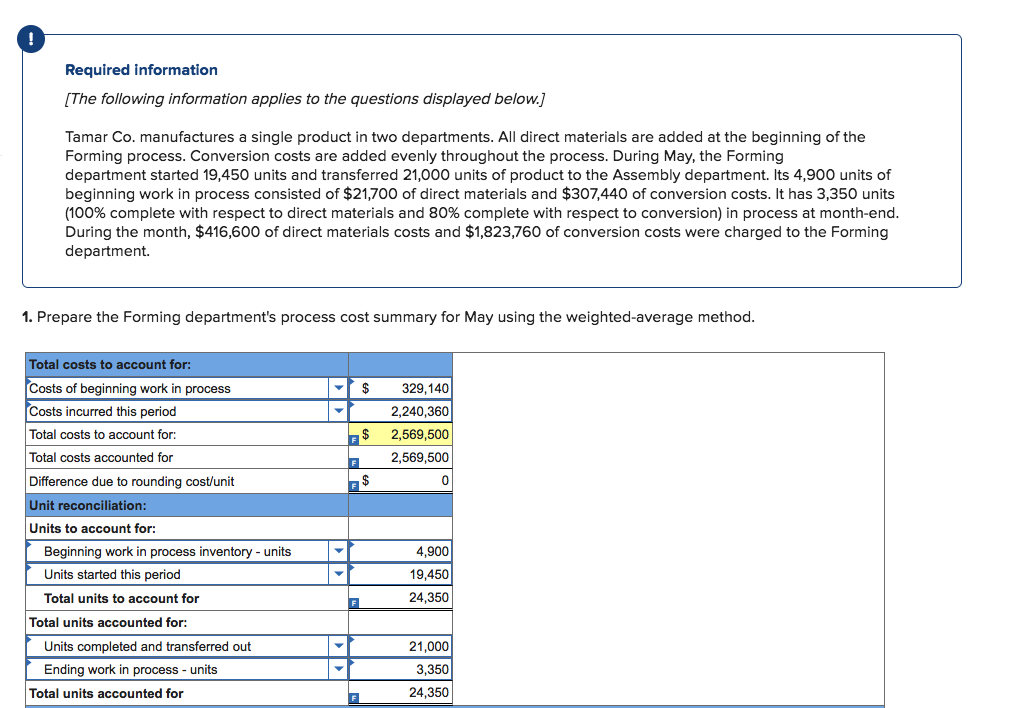

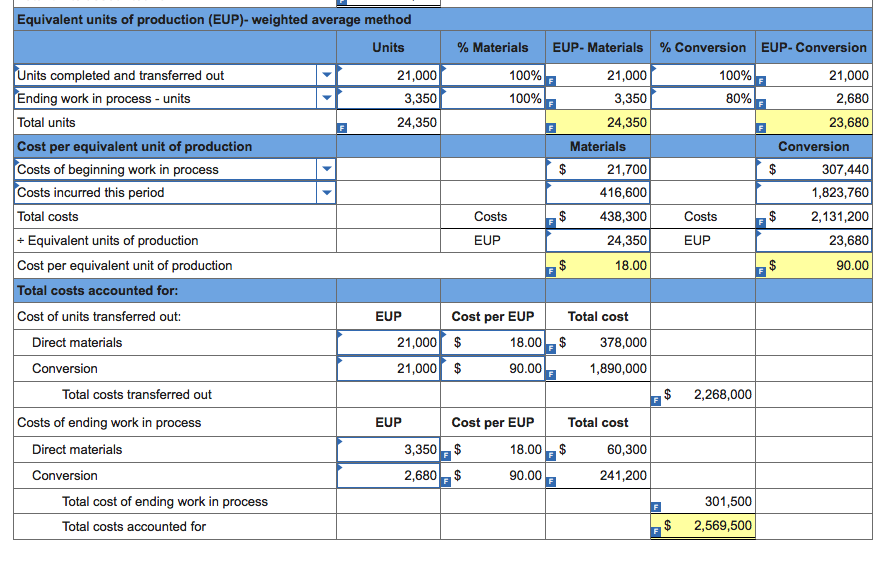

c) Equivalent units and Cost per equivalent unit of production: Because the 2nd department, Assembly, has 4 cost categories, the tables are duplicated such that the first table includes calculations for the cost categories Forming and Packaging and second table includes calculations for the cost categories "Other Direct Material" and "Conversion". Make sure you have amounts in all of the pale blue cells. Equivalent units of production (EUP)- weighted average method (Forming and Packaging) physical Forming EUP- % EUP- Units Costs Forming Packaging Packaging Units completed and transferred out 21,000 100% 21,000 100% 21,000 Ending work in process - units 3,350 100% 3,350 100% 2,680 Total units 24,350 24,350 23,680 Cost per equivalent unit of production Forming Packaging Costs of beginning work in process 329,140 $$ Costs incurred this period 3,816,900 Total costs 4,146,040 Costs Costs * Equivalent units of production EUP EUP Cost per equivalent unit of production (show 4 decimal places Equivalent units of production (EUP)- weighted average method (Other Direct Material and Conversion) physical2 % Other DM | EUP- Other EUP- Units Costs DM Conversion | Conversion Units completed and transferred out Ending work in process - units Total units Cost per equivalent unit of production Other Conversion Costs of beginning work in process 762,400 Costs incurred this period 3,816,900 Total costs Costs Costs + Equivalent units of production EUP EU Cost per equivalent unit of production (show 4 decimal places)Required information [The following information applies to the questions displayed below.] Tamar Co. manufactures a single product in two departments. All direct materials are added at the beginning of the Forming process. Conversion costs are added evenly throughout the process. During May, the Forming department started 19,450 units and transferred 21,000 units of product to the Assembly department. Its 4,900 units of beginning work in process consisted of $21,700 of direct materials and $307,440 of conversion costs. It has 3,350 units (100% complete with respect to direct materials and 80% complete with respect to conversion) in process at month-end. During the month, $416,600 of direct materials costs and $1,823,760 of conversion costs were charged to the Forming department. 1. Prepare the Forming department's process cost summary for May using the weighted-average method. Total costs to account for: Costs of beginning work in process 329,140 Costs incurred this period 2,240,360 Total costs to account for: F $ 2,569,500 Total costs accounted for F 2,569,500 Difference due to rounding cost/unit F $ Unit reconciliation: Units to account for: Beginning work in process inventory - units 4,900 Units started this period 19,450 Total units to account for 24,350 Total units accounted for: Units completed and transferred out 21,000 Ending work in process - units 3,350 Total units accounted for F 24,350Equivalent units of production (EUP)- weighted average method Units Materials EUP- Materials % Conversion EUP- Conversion Units completed and transferred out Y 21,000 100% F 21,000 100% F 21,000 Ending work in process - units 3,350 100% F 3,350 80% F 2,680 Total units F 24,350 F 24,350 F 23,680 Cost per equivalent unit of production Materials Conversion Costs of beginning work in process $ 21,700 $ 307,440 Costs incurred this period 416,600 1,823,760 Total costs Costs $ 438,300 Costs F 2,131,200 + Equivalent units of production EUP 24,350 EUP 23,680 Cost per equivalent unit of production 18.00 F S 90.00 Total costs accounted for: Cost of units transferred out: EUP Cost per EUP Total cost Direct materials 21,000 $ 18.00 378,000 Conversion 21,000 $ 90.00 F 1,890,000 Total costs transferred out F $ 2,268,000 Costs of ending work in process EUP Cost per EUP Total cost Direct materials 3,350 18.00 F $ 60,300 Conversion 2,680 F $ 90.00 F 241,200 Total cost of ending work in process F 301,500 Total costs accounted for F 2,569,500