Read the overview below and complete the activities that follow. The 1933 and 1934 acts are different in the way they protect investors and the

Read the overview below and complete the activities that follow.

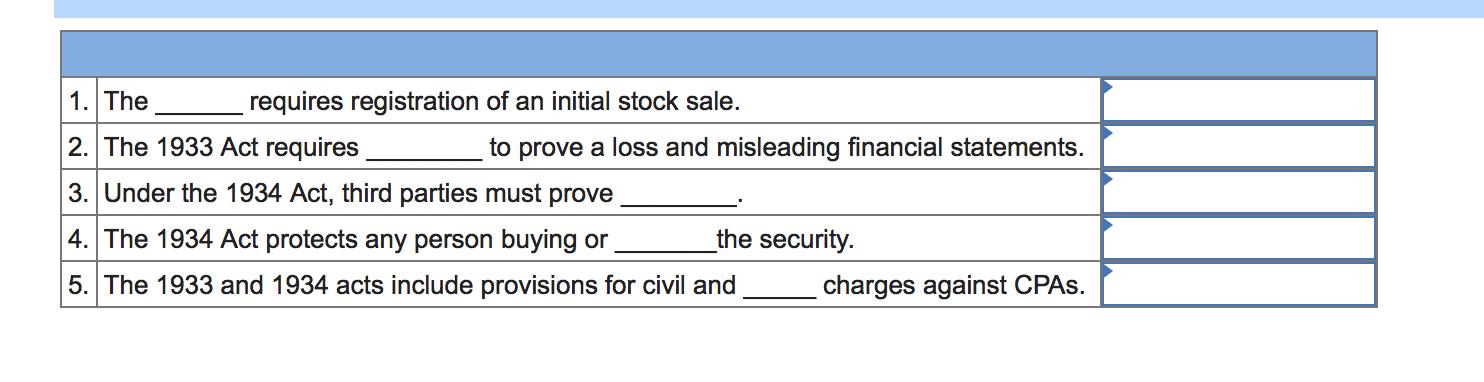

The 1933 and 1934 acts are different in the way they protect investors and the burden of proof required. The 1933 Act pertains to those acquiring an initial distribution of a security; the 1934 Act is for anyone buying or selling the security.

CONCEPT REVIEW:

Auditors have different liability/responsibility under the different acts. For example, under the 1933 Act, the third party does not need to prove reliance on the financial statements; under the 1934 Act, the third party must prove reliance. There is also a difference relating to which third parties the auditor is liable to.

1. The requires registration of an initial stock sale. 2. The 1933 Act requires to prove a loss and misleading financial statements. 3. Under the 1934 Act, third parties must prove 4. The 1934 Act protects any person buying or the security. 5. The 1933 and 1934 acts include provisions for civil and charges against CPAS.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

1 The 1933 Act requires registration of an initial stock sale 2 The 1933 Act requires third party ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws

6th edition

978-1259197109, 77632281, 77862341, 1259197107, 9780077632281, 978-0077862343