Answered step by step

Verified Expert Solution

Question

1 Approved Answer

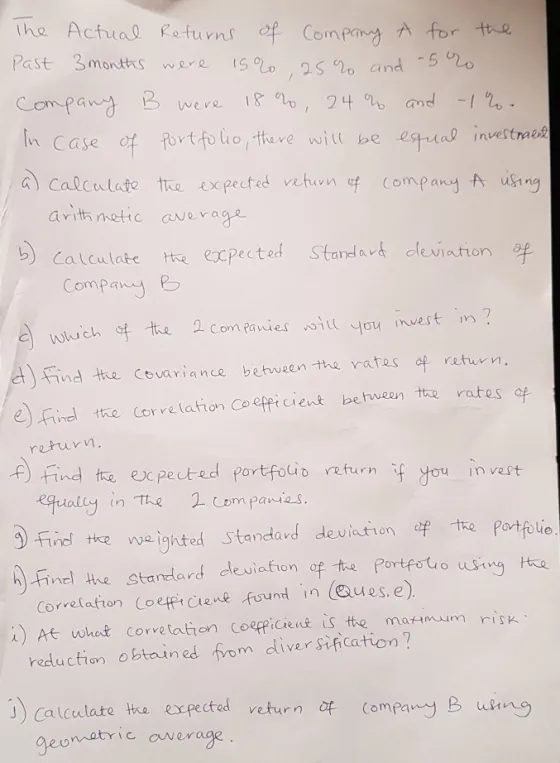

The Actual Returns of Company A for the Past 3 months were 15%, 25% and -5% Company B were 18 %, 24% and 1%-

The Actual Returns of Company A for the Past 3 months were 15%, 25% and -5% Company B were 18 %, 24% and 1%- In case of Portfolio, there will be estual investraent a) calculate the expected return of company A using arithmetic average. Calculate the expected Standard deviation of c) which of the 2 companies will invest in? you. d) Find the covariance between the rates of return. e) Find the correlation Coefficient between the rates of return. f) Find the expected portfolio return if you invest equally in the 2 companies. 9) Find the weighted Standard deviation of the portfolio. Find the standard deviation of the portfolio using the Correlation coefficient found in (Ques. e). i) At what correlation coefficient is the maximum risk: reduction obtained from diversification? 1) calculate the expected return of Company B using. geometric average.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Okay let me solve this stepbystep a Expected return of Company A using Arithmetic Average Returns 15...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516