The applicable tax rate for Question 1 is 16.5%.

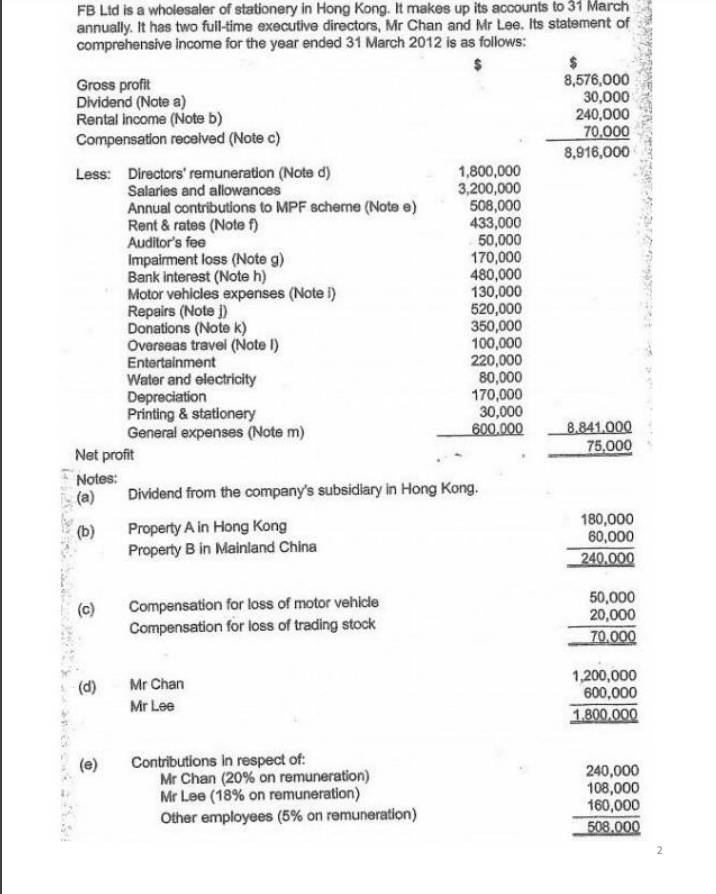

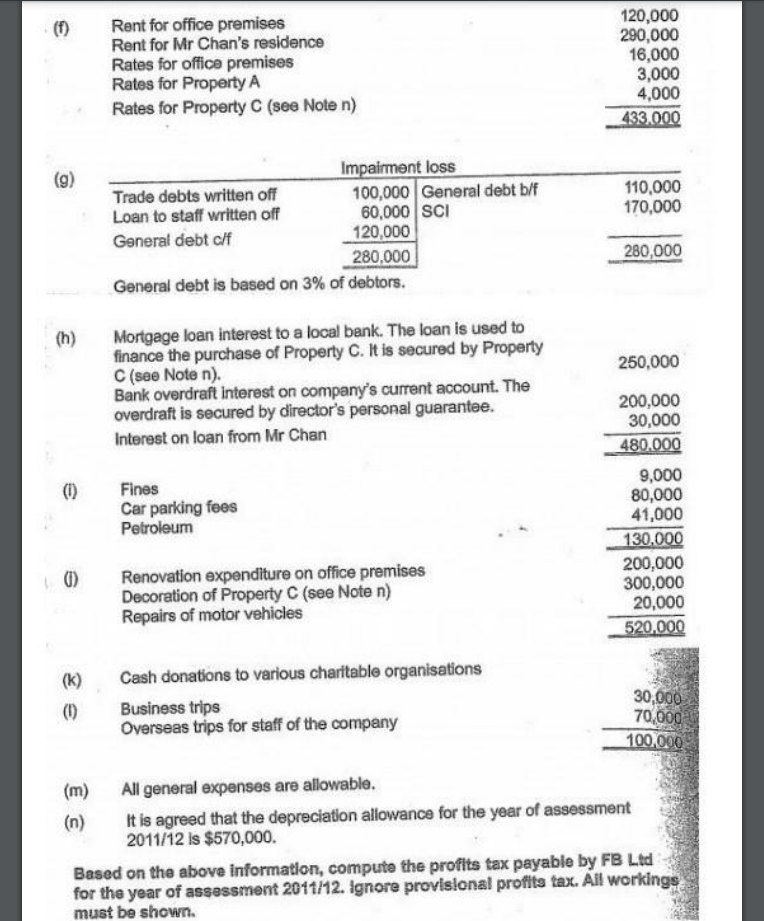

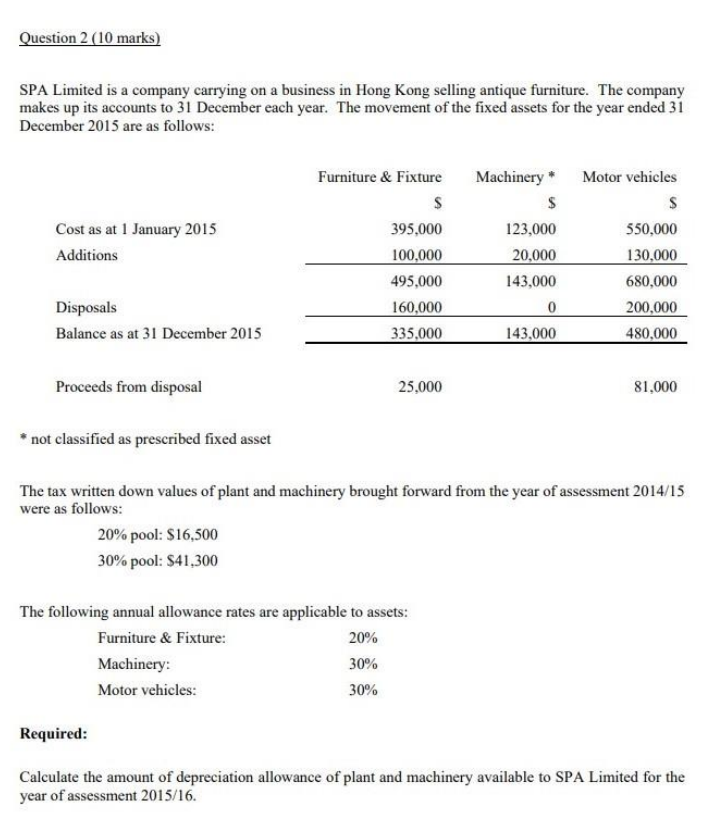

FB Ltd is a wholesaler of stationery in Hong Kong. It makes up its accounts to 31 March annually. It has two full-time executive directors, Mr Chan and Mr Lee. Its statement of comprehensive income for the year ended 31 March 2012 is as follows: 8,576,000 30,000 240,000 70,000 8,916,000 Gross profit Dividend (Note a) Rental income (Note b) Compensation received (Note c) Less: Directors' remuneration (Noted) 1,800,000 Salaries and allowances 3,200,000 Annual contributions to MPF scheme (Note e) 508,000 Rent & rates (Note f) 433,000 Auditor's fee 50,000 Impairment loss (Note g) 170,000 Bank interest (Note h) 480,000 Motor vehicles experises (Notei) 130,000 Repairs (Note 1) 520,000 Donations (Note k) 350,000 Overseas travel (Note 1) 100,000 Entertainment 220,000 Water and electricity 80,000 Depreciation 170,000 Printing & stationery 30,000 General expenses (Note m) 600.000 Net profit Dividend from the company's subsidiary in Hong Kong. (b) Property A in Hong Kong Property B in Mainland China 8.841.000 75,000 Notes: 180,000 60,000 240.000 (c) Compensation for loss of motor vehicle Compensation for loss of trading stock 50,000 20,000 70.000 (d) Mr Chan Mr Lee 1,200,000 600,000 1.800.000 Contributions in respect of: Mr Chan (20% on remuneration) Mr Lee (18% on remuneration) Other employees (5% on remuneration) 240,000 108,000 160,000 508,000 2 Rent for office premises Rent for Mr Chan's residence Rates for office premises Rates for Property A Rates for Property C (see Noten) 120,000 290,000 16,000 3,000 4,000 433.000 (g) 110,000 170,000 Impairment loss Trade debts written off 100,000 General debt b/f Loan to staff written off 60,000 SCI General debt clf 120,000 280,000 General debt is based on 3% of debtors. 280,000 (h) 250,000 Mortgage loan interest to a local bank. The loan is used to finance the purchase of Property C. It is secured by Property C (see Noten). Bank overdraft interest on company's current account. The overdraft is secured by director's personal guarantee. Interest on loan from Mr Chan (1) Fines Car parking fees Petroleum 200,000 30,000 480,000 9,000 80,000 41,000 130,000 200,000 300,000 20,000 520,000 (1) Renovation expenditure on office premises Decoration of Property C (see Noten) Repairs of motor vehicles (k) (6) Cash donations to various charitable organisations Business trips Overseas trips for staff of the company 30,000 70,000 100,000 (m) All general expenses are allowable. It is agreed that the depreciation allowance for the year of assessment 2011/12 is $570,000. Based on the above information, compute the profits tax payable by FB Ltd for the year of assessment 2011/12. Ignore provisional profits tax. All workings must be shown. Question 2 (10 marks) SPA Limited is a company carrying on a business in Hong Kong selling antique furniture. The company makes up its accounts to 31 December each year. The movement of the fixed assets for the year ended 31 December 2015 are as follows: Cost as at 1 January 2015 Additions Furniture & Fixture $ 395,000 100,000 495.000 160,000 335,000 Machinery * Motor vehicles $ $ 123,000 550,000 20,000 130,000 143,000 680,000 0 200,000 143,000 480,000 Disposals Balance as at 31 December 2015 Proceeds from disposal 25,000 81,000 * not classified as prescribed fixed asset The tax written down values of plant and machinery brought forward from the year of assessment 2014/15 were as follows: 20% pool: $16,500 30% pool: $41,300 The following annual allowance rates are applicable to assets: Furniture & Fixture: 20% Machinery: 30% Motor vehicles: 30% Required: Calculate the amount of depreciation allowance of plant and machinery available to SPA Limited for the year of assessment 2015/16. FB Ltd is a wholesaler of stationery in Hong Kong. It makes up its accounts to 31 March annually. It has two full-time executive directors, Mr Chan and Mr Lee. Its statement of comprehensive income for the year ended 31 March 2012 is as follows: 8,576,000 30,000 240,000 70,000 8,916,000 Gross profit Dividend (Note a) Rental income (Note b) Compensation received (Note c) Less: Directors' remuneration (Noted) 1,800,000 Salaries and allowances 3,200,000 Annual contributions to MPF scheme (Note e) 508,000 Rent & rates (Note f) 433,000 Auditor's fee 50,000 Impairment loss (Note g) 170,000 Bank interest (Note h) 480,000 Motor vehicles experises (Notei) 130,000 Repairs (Note 1) 520,000 Donations (Note k) 350,000 Overseas travel (Note 1) 100,000 Entertainment 220,000 Water and electricity 80,000 Depreciation 170,000 Printing & stationery 30,000 General expenses (Note m) 600.000 Net profit Dividend from the company's subsidiary in Hong Kong. (b) Property A in Hong Kong Property B in Mainland China 8.841.000 75,000 Notes: 180,000 60,000 240.000 (c) Compensation for loss of motor vehicle Compensation for loss of trading stock 50,000 20,000 70.000 (d) Mr Chan Mr Lee 1,200,000 600,000 1.800.000 Contributions in respect of: Mr Chan (20% on remuneration) Mr Lee (18% on remuneration) Other employees (5% on remuneration) 240,000 108,000 160,000 508,000 2 Rent for office premises Rent for Mr Chan's residence Rates for office premises Rates for Property A Rates for Property C (see Noten) 120,000 290,000 16,000 3,000 4,000 433.000 (g) 110,000 170,000 Impairment loss Trade debts written off 100,000 General debt b/f Loan to staff written off 60,000 SCI General debt clf 120,000 280,000 General debt is based on 3% of debtors. 280,000 (h) 250,000 Mortgage loan interest to a local bank. The loan is used to finance the purchase of Property C. It is secured by Property C (see Noten). Bank overdraft interest on company's current account. The overdraft is secured by director's personal guarantee. Interest on loan from Mr Chan (1) Fines Car parking fees Petroleum 200,000 30,000 480,000 9,000 80,000 41,000 130,000 200,000 300,000 20,000 520,000 (1) Renovation expenditure on office premises Decoration of Property C (see Noten) Repairs of motor vehicles (k) (6) Cash donations to various charitable organisations Business trips Overseas trips for staff of the company 30,000 70,000 100,000 (m) All general expenses are allowable. It is agreed that the depreciation allowance for the year of assessment 2011/12 is $570,000. Based on the above information, compute the profits tax payable by FB Ltd for the year of assessment 2011/12. Ignore provisional profits tax. All workings must be shown. Question 2 (10 marks) SPA Limited is a company carrying on a business in Hong Kong selling antique furniture. The company makes up its accounts to 31 December each year. The movement of the fixed assets for the year ended 31 December 2015 are as follows: Cost as at 1 January 2015 Additions Furniture & Fixture $ 395,000 100,000 495.000 160,000 335,000 Machinery * Motor vehicles $ $ 123,000 550,000 20,000 130,000 143,000 680,000 0 200,000 143,000 480,000 Disposals Balance as at 31 December 2015 Proceeds from disposal 25,000 81,000 * not classified as prescribed fixed asset The tax written down values of plant and machinery brought forward from the year of assessment 2014/15 were as follows: 20% pool: $16,500 30% pool: $41,300 The following annual allowance rates are applicable to assets: Furniture & Fixture: 20% Machinery: 30% Motor vehicles: 30% Required: Calculate the amount of depreciation allowance of plant and machinery available to SPA Limited for the year of assessment 2015/16