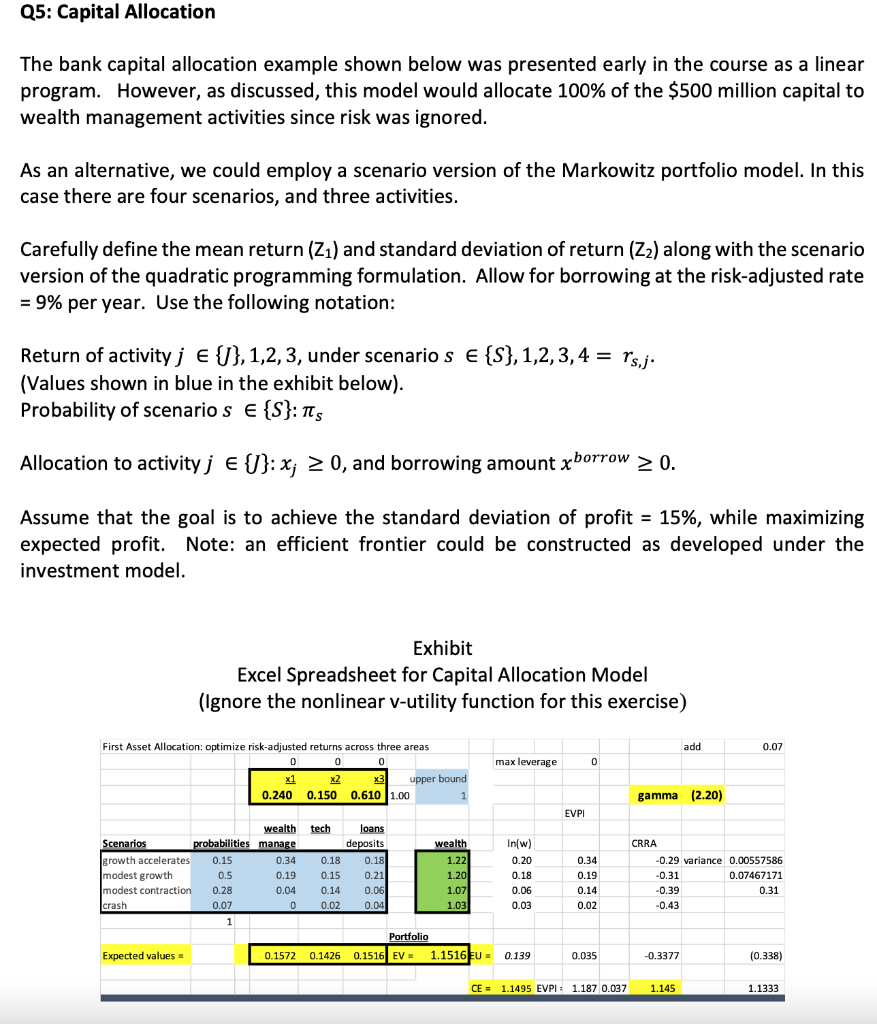

The bank capital allocation example shown below was presented early in the course as a linear program. However, as discussed, this model would allocate 100% of the $500 million capital to wealth management activities since risk was ignored. As an alternative, we could employ a scenario version of the Markowitz portfolio model. In this case there are four scenarios, and three activities. Carefully define the mean return (Z1) and standard deviation of return (Z2) along with the scenario version of the quadratic programming formulation. Allow for borrowing at the risk-adjusted rate =9% per year. Use the following notation: Return of activity j{J},1,2,3, under scenario s{S},1,2,3,4=rs,j. (Values shown in blue in the exhibit below). Probability of scenario s{S}:S Allocation to activity j{J}:xj0, and borrowing amount xborrow0. Assume that the goal is to achieve the standard deviation of profit =15%, while maximizing expected profit. Note: an efficient frontier could be constructed as developed under the investment model. Exhibit Excel Spreadsheet for Capital Allocation Model (Ignore the nonlinear v-utility function for this exercise) The bank capital allocation example shown below was presented early in the course as a linear program. However, as discussed, this model would allocate 100% of the $500 million capital to wealth management activities since risk was ignored. As an alternative, we could employ a scenario version of the Markowitz portfolio model. In this case there are four scenarios, and three activities. Carefully define the mean return (Z1) and standard deviation of return (Z2) along with the scenario version of the quadratic programming formulation. Allow for borrowing at the risk-adjusted rate =9% per year. Use the following notation: Return of activity j{J},1,2,3, under scenario s{S},1,2,3,4=rs,j. (Values shown in blue in the exhibit below). Probability of scenario s{S}:S Allocation to activity j{J}:xj0, and borrowing amount xborrow0. Assume that the goal is to achieve the standard deviation of profit =15%, while maximizing expected profit. Note: an efficient frontier could be constructed as developed under the investment model. Exhibit Excel Spreadsheet for Capital Allocation Model (Ignore the nonlinear v-utility function for this exercise)