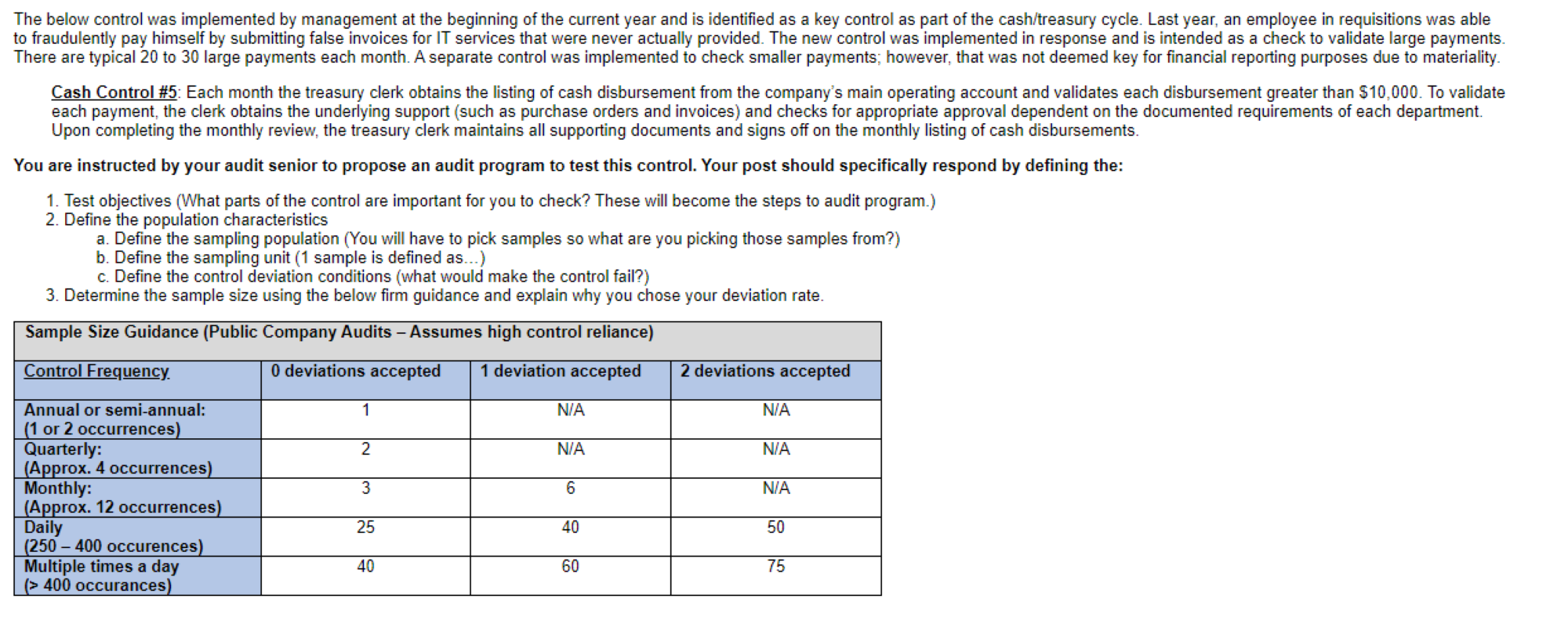

The below control was implemented by management at the beginning of the current year and is identified as a key control as part of the cash/treasury cycle. Last year, an employee in requisitions was able to fraudulently pay himself by submitting false invoices for IT services that were never actually provided. The new control was implemented in response and is intended as a check to validate large payments There are typical 20 to 30 large payments each month. A separate control was implemented to check smaller payments; however, that was not deemed key for financial reporting purposes due to materiality Cash Control #5: Each month the treasury clerk obtains the listing of cash disbursement from the company's main operating account and validates each disbursement greater than $10,000. To validate each payment, the clerk obtains the underlying support (such as purchase orders and invoices) and checks for appropriate approval dependent on the documented requirements of each department. Upon completing the monthly review, the treasury clerk maintains all supporting documents and signs off on the monthly listing of cash disbursements. You are instructed by your audit senior to propose an audit program to test this control. Your post should specifically respond by defining the: 1. Test objectives (What parts of the control are important for you to check? These will become the steps to audit program.) 2. Define the population characteristics a. Define the sampling population (You will have to pick samples so what are you picking those samples from?) b. Define the sampling unit (1 sample is defined as...) c. Define the control deviation conditions (what would make the control fail?) 3. Determine the sample size using the below firm guidance and explain why you chose your deviation rate. Sample Size Guidance (Public Company Audits - Assumes high control reliance) Control Frequency O deviations accepted 2 deviations accepted 1 deviation accepted N/A N/A N/A Annual or semi-annual: (1 or 2 occurrences) Quarterly: (Approx. 4 occurrences) Monthly: (Approx. 12 occurrences) Daily (250 - 400 occurences) Multiple times a day > 400 occurances) The below control was implemented by management at the beginning of the current year and is identified as a key control as part of the cash/treasury cycle. Last year, an employee in requisitions was able to fraudulently pay himself by submitting false invoices for IT services that were never actually provided. The new control was implemented in response and is intended as a check to validate large payments There are typical 20 to 30 large payments each month. A separate control was implemented to check smaller payments; however, that was not deemed key for financial reporting purposes due to materiality Cash Control #5: Each month the treasury clerk obtains the listing of cash disbursement from the company's main operating account and validates each disbursement greater than $10,000. To validate each payment, the clerk obtains the underlying support (such as purchase orders and invoices) and checks for appropriate approval dependent on the documented requirements of each department. Upon completing the monthly review, the treasury clerk maintains all supporting documents and signs off on the monthly listing of cash disbursements. You are instructed by your audit senior to propose an audit program to test this control. Your post should specifically respond by defining the: 1. Test objectives (What parts of the control are important for you to check? These will become the steps to audit program.) 2. Define the population characteristics a. Define the sampling population (You will have to pick samples so what are you picking those samples from?) b. Define the sampling unit (1 sample is defined as...) c. Define the control deviation conditions (what would make the control fail?) 3. Determine the sample size using the below firm guidance and explain why you chose your deviation rate. Sample Size Guidance (Public Company Audits - Assumes high control reliance) Control Frequency O deviations accepted 2 deviations accepted 1 deviation accepted N/A N/A N/A Annual or semi-annual: (1 or 2 occurrences) Quarterly: (Approx. 4 occurrences) Monthly: (Approx. 12 occurrences) Daily (250 - 400 occurences) Multiple times a day > 400 occurances)