Answered step by step

Verified Expert Solution

Question

1 Approved Answer

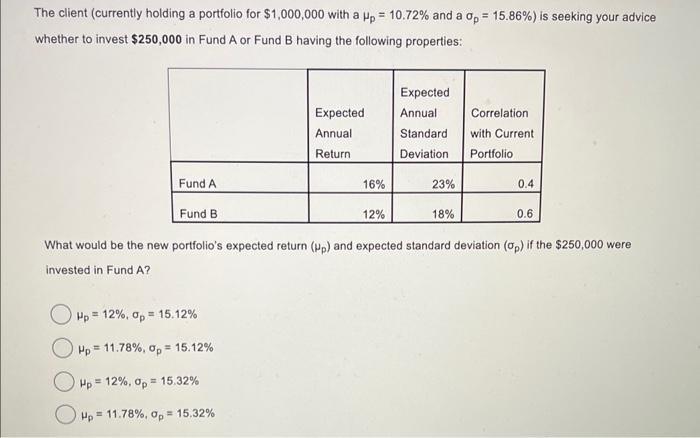

The client (currently holding a portfolio for $1,000,000 with a Hp = 10.72% and a op = 15.86%) is seeking your advice whether to

The client (currently holding a portfolio for $1,000,000 with a Hp = 10.72% and a op = 15.86%) is seeking your advice whether to invest $250,000 in Fund A or Fund B having the following properties: Expected Expected Annual Correlation Annual Return Standard Deviation with Current Portfolio Fund A 16% 23% 0.4 Fund B 12% 18% 0.6 What would be the new portfolio's expected return (up) and expected standard deviation (ap) if the $250,000 were invested in Fund A? Hp = 12%, p = 15.12% = Hp 11.78%, op 15.12% Hp = 12%, p = 15.32% Hp 11.78%, p= 15.32%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Financial Management

Authors: James Van Horne, John Wachowicz

13th Revised Edition

978-0273713630, 273713639