Answered step by step

Verified Expert Solution

Question

1 Approved Answer

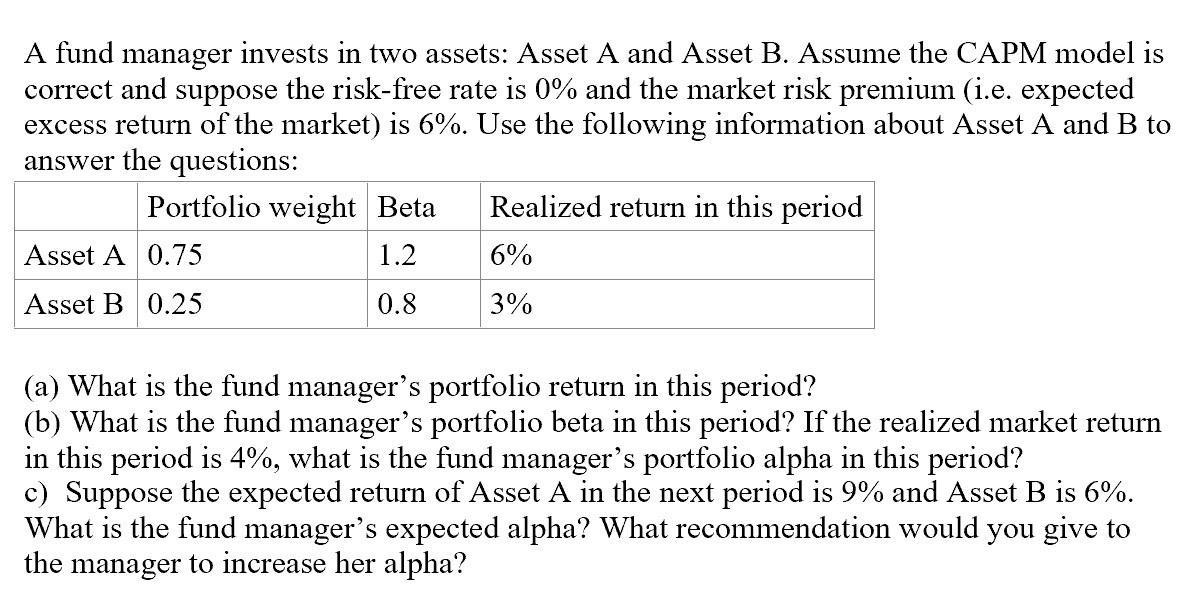

A fund manager invests in two assets: Asset A and Asset B. Assume the CAPM model is correct and suppose the risk-free rate is

A fund manager invests in two assets: Asset A and Asset B. Assume the CAPM model is correct and suppose the risk-free rate is 0% and the market risk premium (i.e. expected excess return of the market) is 6%. Use the following information about Asset A and B to answer the questions: Portfolio weight Beta 1.2 0.8 Asset A 0.75 Asset B 0.25 Realized return in this period 6% 3% (a) What is the fund manager's portfolio return in this period? (b) What is the fund manager's portfolio beta in this period? If the realized market return in this period is 4%, what is the fund manager's portfolio alpha in this period? c) Suppose the expected return of Asset A in the next period is 9% and Asset B is 6%. What is the fund manager's expected alpha? What recommendation would you give to the manager to increase her alpha?

Step by Step Solution

★★★★★

3.41 Rating (145 Votes )

There are 3 Steps involved in it

Step: 1

a The fund managers portfolio return in this period ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Using Financial Accounting Information The Alternative to Debits and Credits

Authors: Gary A. Porter, Curtis L. Norton

8th edition

1111534918, 978-1111534912