Answered step by step

Verified Expert Solution

Question

1 Approved Answer

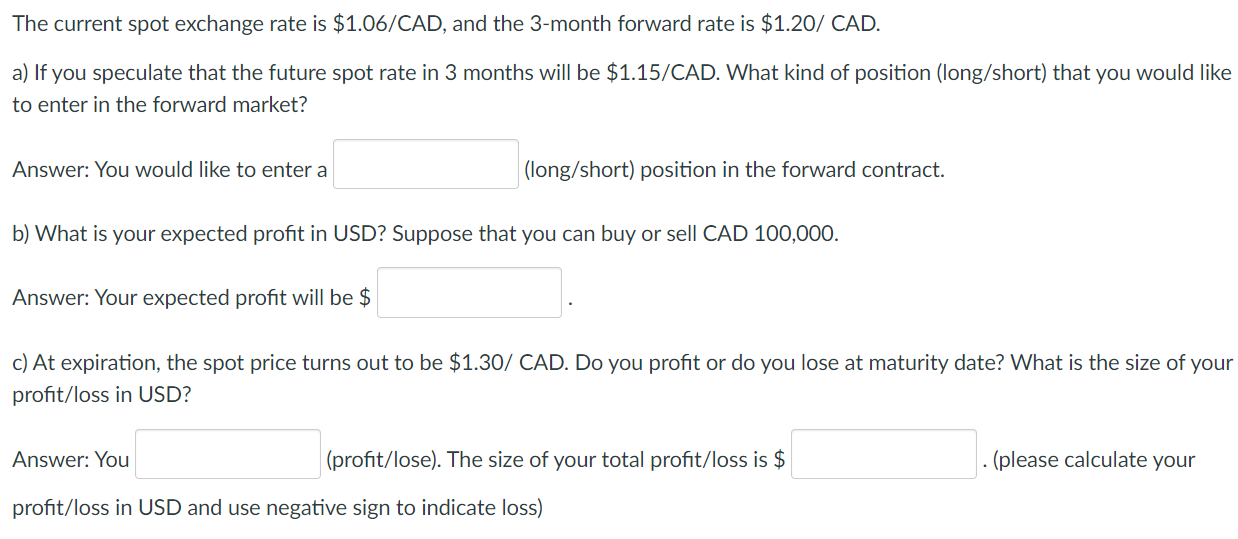

The current spot exchange rate is $1.06/CAD, and the 3-month forward rate is $1.20 / CAD. a) If you speculate that the future spot rate

The current spot exchange rate is $1.06/CAD, and the 3-month forward rate is $1.20 / CAD. a) If you speculate that the future spot rate in 3 months will be $1.15/CAD. What kind of position (long/short) that you would like to enter in the forward market? Answer: You would like to enter a (long/short) position in the forward contract. b) What is your expected profit in USD? Suppose that you can buy or sell CAD 100,000. Answer: Your expected profit will be \$ c) At expiration, the spot price turns out to be $1.30 / CAD. Do you profit or do you lose at maturity date? What is the size of your profit/loss in USD? Answer: You (profit/lose). The size of your total profit/loss is \$ . (please calculate your profit/loss in USD and use negative sign to indicate loss)

The current spot exchange rate is $1.06/CAD, and the 3-month forward rate is $1.20 / CAD. a) If you speculate that the future spot rate in 3 months will be $1.15/CAD. What kind of position (long/short) that you would like to enter in the forward market? Answer: You would like to enter a (long/short) position in the forward contract. b) What is your expected profit in USD? Suppose that you can buy or sell CAD 100,000. Answer: Your expected profit will be \$ c) At expiration, the spot price turns out to be $1.30 / CAD. Do you profit or do you lose at maturity date? What is the size of your profit/loss in USD? Answer: You (profit/lose). The size of your total profit/loss is \$ . (please calculate your profit/loss in USD and use negative sign to indicate loss)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Technology Start Ups

Authors: Alnoor Bhimani

2nd Edition

1398603082, 978-1398603080