Answered step by step

Verified Expert Solution

Question

1 Approved Answer

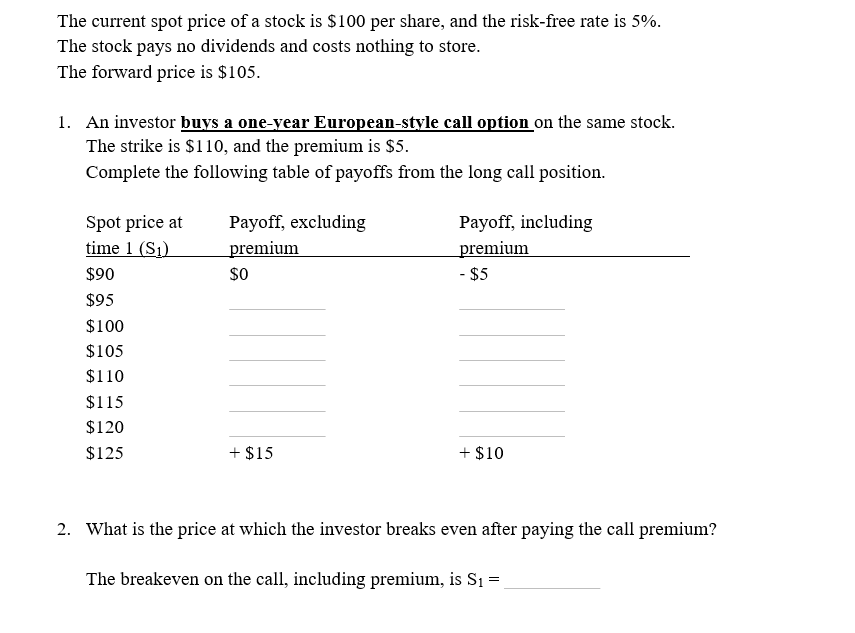

The current spot price of a stock is $100 per share, and the risk-free rate is 5%. The stock pays no dividends and costs nothing

The current spot price of a stock is $100 per share, and the risk-free rate is 5%. The stock pays no dividends and costs nothing to store. The forward price is $105. 1. An investor buys a one-year European-style call option on the same stock. The strike is $110, and the premium is $5. Complete the following table of payoffs from the long call position. 2. What is the price at which the investor breaks even after paying the call premium? The breakeven on the call, including premium, is S1=

The current spot price of a stock is $100 per share, and the risk-free rate is 5%. The stock pays no dividends and costs nothing to store. The forward price is $105. 1. An investor buys a one-year European-style call option on the same stock. The strike is $110, and the premium is $5. Complete the following table of payoffs from the long call position. 2. What is the price at which the investor breaks even after paying the call premium? The breakeven on the call, including premium, is S1=

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantum Investing Unlocking The Secrets Of The New Financial System

Authors: Hugh Webb

1st Edition

979-8388948823