Question

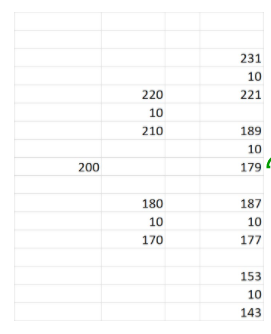

The current stock price is $200. The stock pays a dividend of $10 every quarter. The risk-free rate is 8%. Over each of the next

The current stock price is $200. The stock pays a dividend of $10 every quarter. The risk-free rate is 8%. Over each of the next three-month periods the stock could go up by 10% (u=1.1) or down by 10% (d=.90). The option expires in six months after the second dividend is paid. The price chart is given below.

What is the price of an European Style Put with a strike of $210? (Round to 2 decimal places)

231 10 221 220 10 210 139 10 179 200 180 10 170 187 10 177 153 10 143Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Protecting Main Street Measuring The Customer Experience In Financial Services For Business And Public Policy

Authors: Paul C. Lubin

1st Edition

1138864161,1136902546