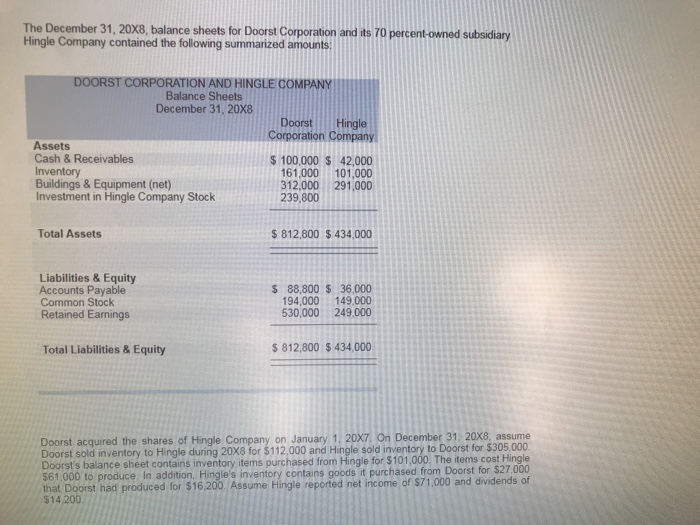

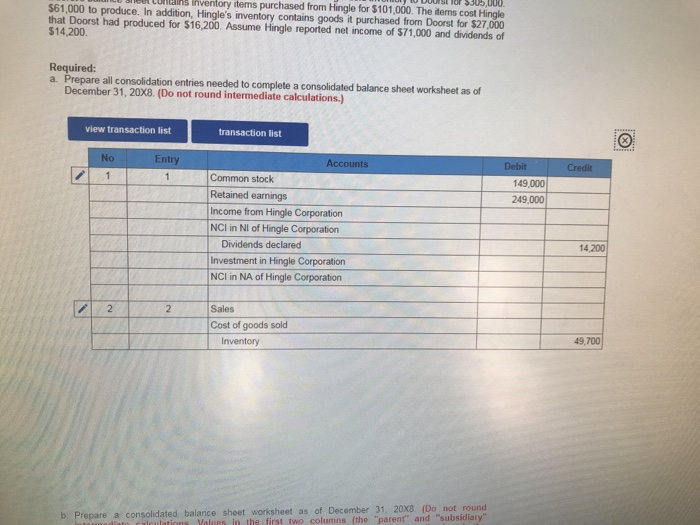

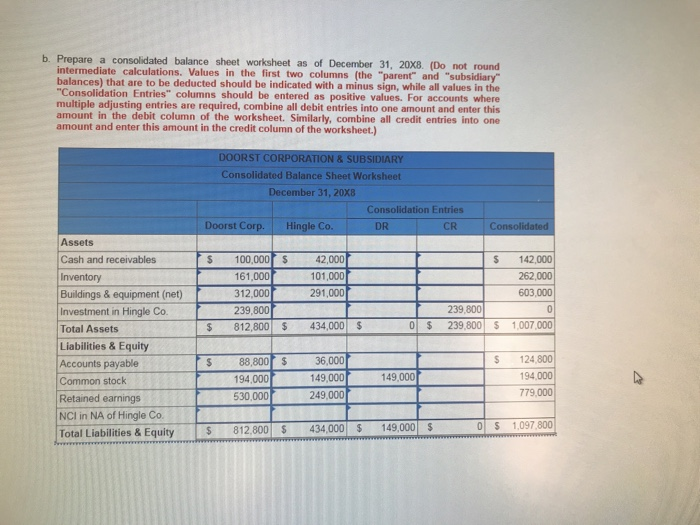

The December 31, 20X8, balance sheets for Doorst Corporation and its 70 percent-owned subsidiary Hingle Company contained the following summarized amounts: DOORST CORPORATION AND HINGLE COM Balance Sheets December 31, 20X8 Doorst Hingle Corporation C ompany Assets Cash & Receivables Inventory Buildings & Equipment (net) Investment in Hingle Company Stock $ 100,000 $ 42,000 161,000 101,000 312,000 291,000 239,800 Total Assets $ 812,800 $ 434,000 Liabilities& Equity Accounts Payable Common Stock Retained Earnings $ 88,800 $ 36.000 94,000 149.000 530,000 249,000 Total Liabilities & Equity 812,800 $ 434,000 Doorst acquired the shares of Hingle Company on January 1, 20X7 On December 31, 20X8, assume Doorst sold inventory to Hingle during 20X8 for $112,000 and Hingle sold inventory to Doorst for $305,000 Doorst's balance sheet contains inventory items purchased from Hingle for $101,000. The items cost Hingle $61,000 to produce In addition that Doorst had produced for $16200. Assume Hingle reported net income of $71.000 and dividends of $14,200 Meel Conailks inventory items purchased from Hingle for $101,000. The items cost Hingle $61,000 to produce. In addition, Hingle's inventory contains goods it purchased from Doorst for $27,000 that Doorst had produced for $16,200. Assume Hingle reported net income of $71,000 and dividends of $14,200 Required: a. Prepare all consolidation entries needed to complete a consolidated balance sheet worksheet as of December 31, 20X8. (Do not round intermediate calculations.) view transaction list transaction list No Entry Accounts Common stock 149,000 Retained earnings 249,000 Income from Hingle Corporation NCI in NI of Hingle Corporation Dividends declared Investment in Hingle Corporation NCI in NA of Hingle Corporation 14.200 2 Sales Cost of goods sold 49,700 Inventory re a consolidated balance sheet worksheet as of December 31, 20X8. (Do not round in the first two columns (the "parent" and "subsidiary" b. Prepar b. Prepare a consolidated balance sheet worksheet as of December 31, 20X8. (Do not round ations. Values in the first two columns (the "parent" and "subsidiary balances) that are to be deducted should be indicated with a minus sign, while all values in the Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet.) DOORST CORPORATION &SUBSIDIARY Consolidated Balance Sheet Worksheet December 31, 20X8 Consolidation Entries Doorst Corp Hingle Co. CR Assets Cash and receivables Inventory Buildings & equipment (net) Investment in Hingle Co. Total Assets Liabilities & Equity Accounts payable Common stock Retained earnings NCI in NA of Hingle Co. S 142,000 262,000 603,000 S 100,000 S 161,000 312,000 239,800 42,000 101,000 291,000 239,800 239,800 1,007,000 812,800 434,000 $ S 88,800 S 194,000 530,000 36,000 149,000 249,000 S 124,800 194.000 779,000 149,000 O S 1,097,800 Total Liabilities & EquityS 812 800 S 434 000 S149000 S