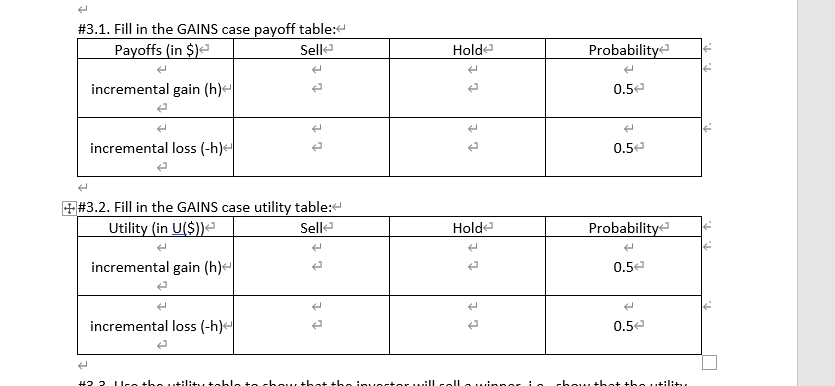

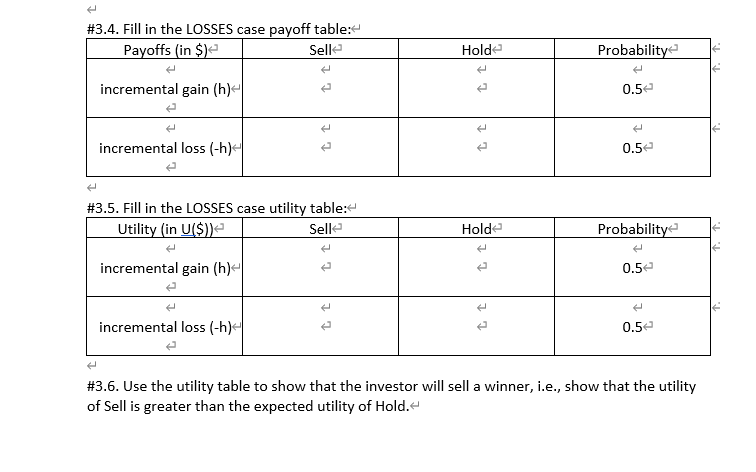

Question

The disposition effect has been characterized in various ways: the effect, whereby investors are anxious to sell their winners, but reluctant to sell their losers

The disposition effect has been characterized in various ways: the effect, whereby investors are anxious to sell their winners, but reluctant to sell their losers (Shefrin 2005, 419); the tendency to hold losers too long and sell winners too soon (Odean 1998, 1775), and the effect, whereby investors sell winners more readily than losers (Odean 1998, 1779). Basically, the disposition effect says investors will sell winners and hold losers. The key point is there is nothing irrational about this behavior. It is consistent with maximizing expected utility given that the investor has the S-shaped utility function of prospect theory.

Suppose Xo = $500, h = $300, the risk averse utility function is U(x) = SQRT(x), and the risk seeking utility function is U(x) = SQRT(x).

#3.3. Use the utility table to show that the investor will sell a winner, i.e., show that the utility of Sell is greater than the expected utility of Hold.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Beyond Agile Auditing Three Core Components To Revolutionize Your Internal Audit Practices

Authors: Clarissa Lucas

1st Edition

1950508676, 978-1950508679