Answered step by step

Verified Expert Solution

Question

1 Approved Answer

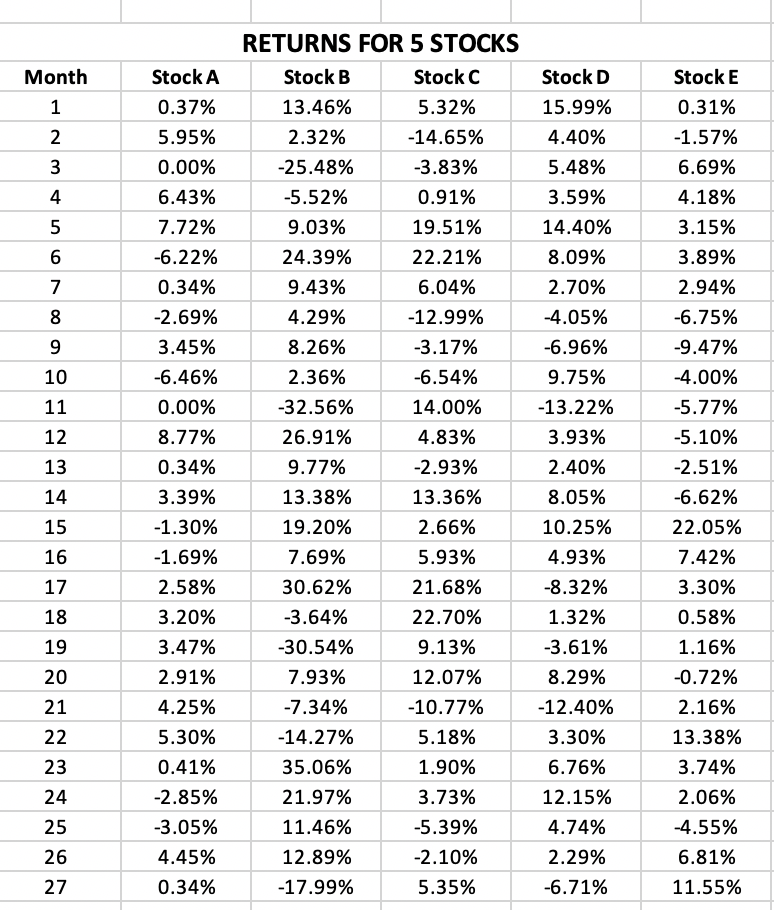

The Excel file Stock Data contains monthly return data for five ( 5 ) stocks. a . Use these returns and the Matrix of Excess

The Excel file Stock Data contains monthly return data for five stocks.

a Use these returns and the Matrix of Excess Returns to compute the VarianceCovariance Matrix for these five stocks. Do not use the varcovar VBA function

b Use the Variance Covariance Matrix for these five stocks to compute the individual stock proportions for the Global Minimum Variance Portfolio GMVP

c Calculate the Expected Return and Risk Standard Deviation for the Global Minimum Variance Portfolio GMVP

Please answer this question with screenshots of excel including the formulas so I can understand it better, thanks. RETURNS FOR STOCKS

tableMonthStock AStock BStock CStock DStock E

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Futures And Options Markets

Authors: John C. Hull

5th Edition

0131445650, 9780131445659