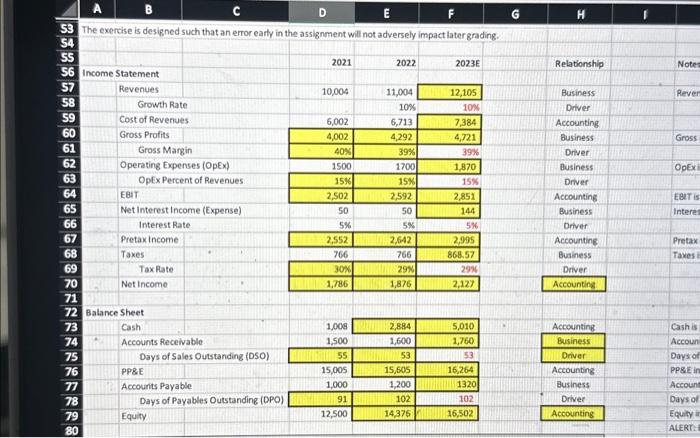

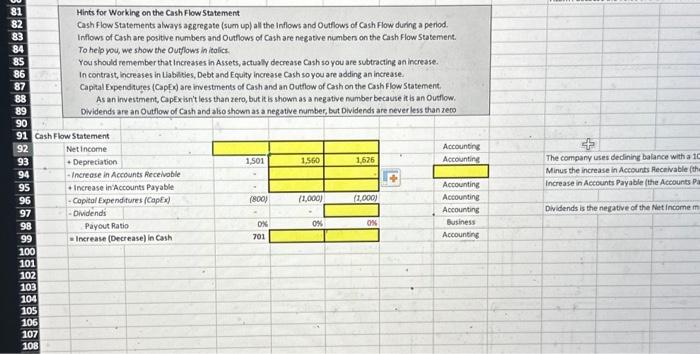

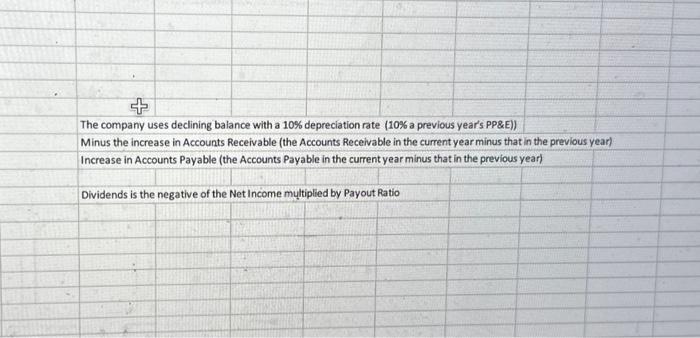

The exercise is designed such that an error earfy in the assignment will not adversely impact latergrading. \begin{tabular}{|c|c|c|c|c|c|c|} \hline \\ \hline \multirow{2}{*}{\multicolumn{7}{|c|}{\begin{tabular}{l} 54 \\ 55 \\ 56 \end{tabular}}} \\ \hline & & & & & & \\ \hline 57 & & Revenues & & 10,004 & 11,004 & 12,105 \\ \hline 58 & & \multicolumn{2}{|l|}{ Growth Rate } & & 10% & 10% \\ \hline 59 & & \multicolumn{2}{|c|}{ Cost of Revenues } & 6,002 & 6,713 & 7,384 \\ \hline 60 & & Gross Profits & & 4,002 & 4,292 & 4,721 \\ \hline 61 & & \multicolumn{2}{|c|}{ Gross Margin } & & 39% & 39% \\ \hline 62 & & \multicolumn{2}{|c|}{ Operating Expenses (OpEx) } & 1500 & 1700 & 1.870 \\ \hline 63 & & \multicolumn{2}{|c|}{ OpEx. Percent of Revenues } & 15% & 15% & 15% \\ \hline 64 & & EBIT & & \begin{tabular}{l|l|l|} 2,502 & \\ \end{tabular} & 2,592 & 2851 \\ \hline 65 & & \multicolumn{2}{|c|}{ Net Interest Income (Expense) } & 50 & 50 & 144 \\ \hline 66 & & \multicolumn{2}{|c|}{ Interest Rate } & 5% & 5% & 5% \\ \hline 67 & & Pretaxincome & & 2,552 & 2,642 & 2995 \\ \hline 68 & & Taxes & & 766 & 766 & 868.57 \\ \hline 69 & & Taxplate & H. & & 29 & 2996 \\ \hline 70 & 79 & Net Income & . & 1,786 & 1,876 & 2,127 \\ \hline 71 & & & & & & \\ \hline 72 & \multicolumn{6}{|c|}{ Balance Sheet } \\ \hline 73 & & Cash & F & 1,008 & \begin{tabular}{|l|l|} 2,884 & \\ \end{tabular} & 5,010 \\ \hline 74 & i. & \multicolumn{2}{|c|}{ Accounts Receivable } & 1,500 & 1,600 & 1,760 \\ \hline 75 & & \multicolumn{2}{|c|}{ Days of Sales Outstanding (DSO) } & 55 & & 53 \\ \hline 76 & & PPBE & & 15,005 & \begin{tabular}{l|l} 15,605 \\ \end{tabular} & 16,264 \\ \hline 77 & ifi & \multicolumn{2}{|c|}{ Accounts Payable } & 1,000 & 1,200 & 1320 \\ \hline 78 & & \multicolumn{2}{|c|}{ Days of Payables Outstanding (DPO) } & \begin{tabular}{|l|l|l} 91 & \\ \end{tabular} & 102 & 102 \\ \hline 79 & & Equity & & 12,500 & 14,376 & 16,502 \\ \hline \end{tabular} The company uses declining balance with a 10% depreciation rate ( 10% a previous year's PP\&E)) Minus the increase in Accounts Receivable (the Accounts Recelvable in the current year minus that in the previous year) Increase in Accounts Payable (the Accounts Payable in the current year minus that in the previous year) Dividends is the negative of the Net Income multiplied by Payout Ratio Hints for Working on the Cash Flow Statement Cash Flow Statements always aggregate (sum up) all the Inflows and Outflows of Cash Flow during a period. Inflows of Cash are positve numbers and Outlows of Cash are negave numbers on the Cash Flow Statement. To heip you, we show the Outflows in italics. You should remember that Increases in Assets, actualy decrease Cash so you are subtracting an increase. in contrast, increases in Liabilties, Debt and Ecuity increase Cash so you are adding an increase. Capital Expendituges (CapEx) are investments of Cash and an Outflow of Cash on the Cash Flow Statement. As an investment, CapExisn't less than zero, but it is shown as a negative number because it is an Oufliow. Dividendi are an Outflow of Cash and also shown as a negative number, but Dividends are never less than zeco