Answered step by step

Verified Expert Solution

Question

1 Approved Answer

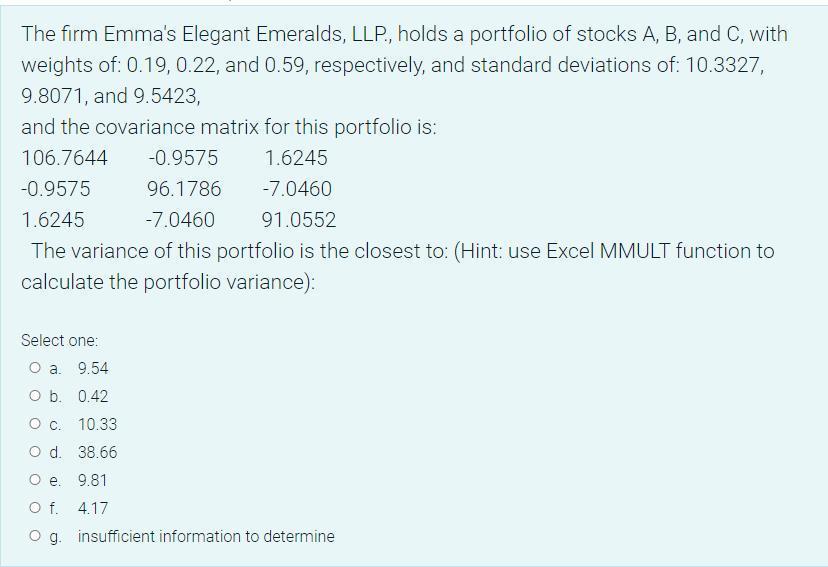

The firm Emma's Elegant Emeralds, LLP., holds a portfolio of stocks A, B, and C, with weights of: 0.19, 0.22, and 0.59, respectively, and

The firm Emma's Elegant Emeralds, LLP., holds a portfolio of stocks A, B, and C, with weights of: 0.19, 0.22, and 0.59, respectively, and standard deviations of: 10.3327, 9.8071, and 9.5423, and the covariance matrix for this portfolio is: 106.7644 -0.9575 1.6245 -0.9575 96.1786 -7.0460 1.6245 -7.0460 91.0552 The variance of this portfolio is the closest to: (Hint: use Excel MMULT function to calculate the portfolio variance): Select one: O a. 9.54 O b. 0.42 O c. O d. O e. 9.81 O f. 4.17 O g. insufficient information to determine 10.33 38.66

Step by Step Solution

There are 3 Steps involved in it

Step: 1

The formula to calculate the variance when 3 stocks are in portfolio i...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Operations Management

Authors: William J Stevenson

12th edition

2900078024107, 78024102, 978-0078024108