Answered step by step

Verified Expert Solution

Question

1 Approved Answer

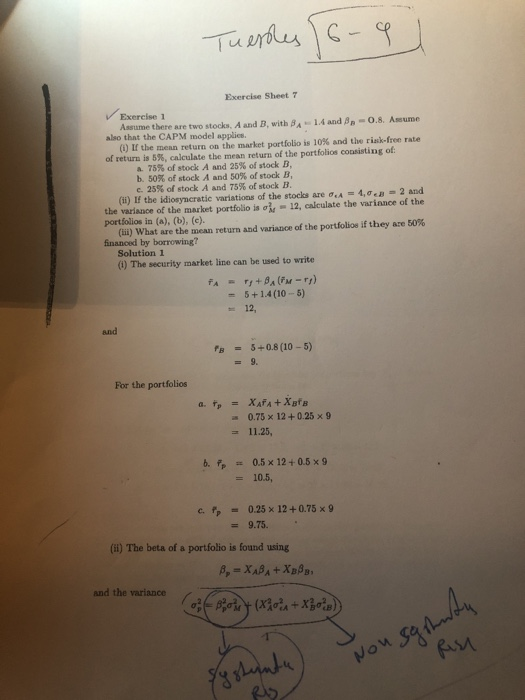

The first picture shows the question, part (iii) what are the mean return and variance of the portfolios if they are 50% finananced by borrowing?

The first picture shows the question, part (iii) what are the mean return and variance of the portfolios if they are 50% finananced by borrowing?

The first picture shows the question, part (iii) what are the mean return and variance of the portfolios if they are 50% finananced by borrowing? I dont know how to solve this one

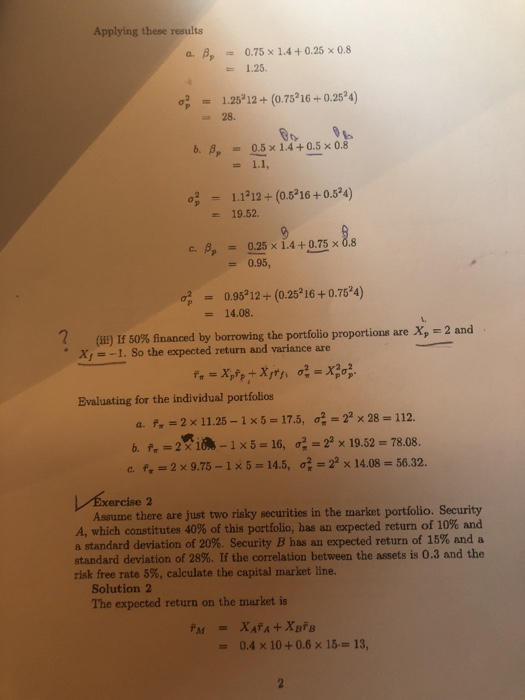

The second picture shows the answer

I am confused by the answer, from where did they get Xp=2 Xf= -1 and so on

Kindly show me the working out of part iii with maybe an explanation so I understand and get how to solve it

Thanks!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance Growth And Inequality

Authors: Louis-Philippe Rochon, Virginie Monvoisin

1st Edition

1788973682, 978-1788973687