Answered step by step

Verified Expert Solution

Question

1 Approved Answer

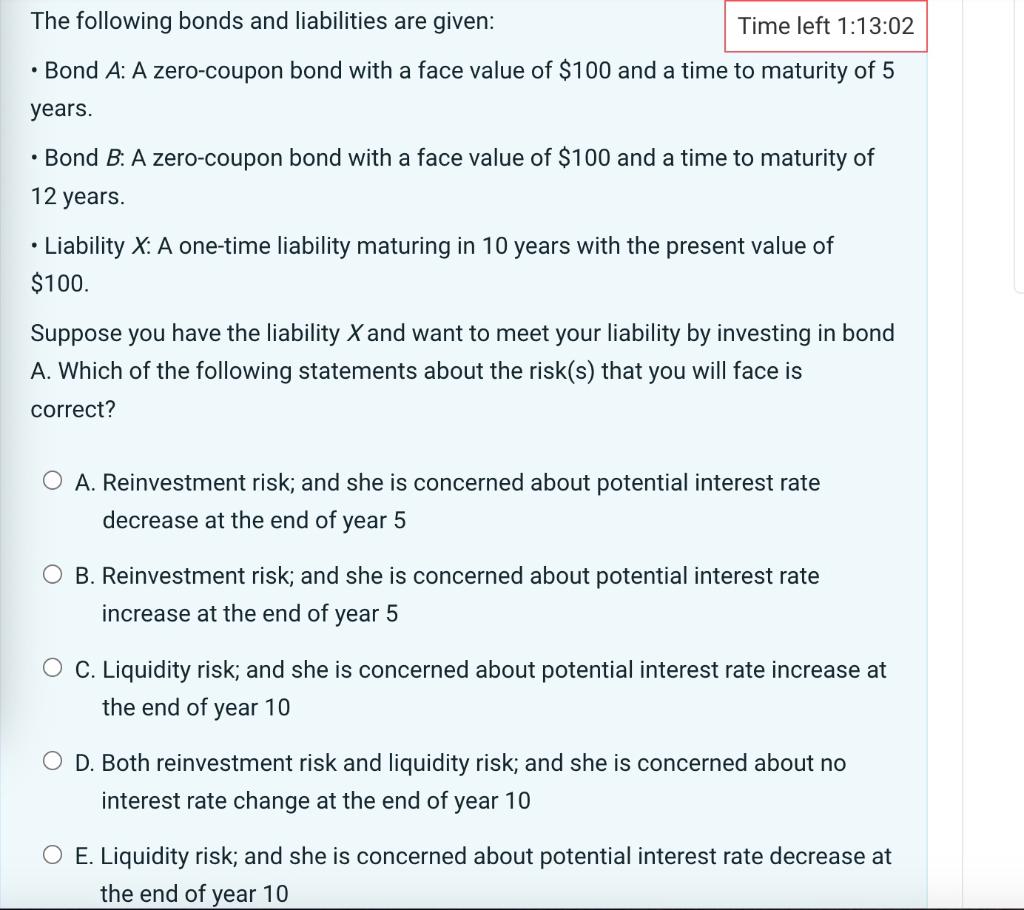

The following bonds and liabilities are given: - Bond A : A zero-coupon bond with a face value of $100 and a time to maturity

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Corporate Strategy

Authors: David Hillier , Mark Grinblatt , Sheridan Titman

2nd Edition

0077129423,0077141350