Question

the following example is provided to answer the questions below: The stock A is currently trading at $100. Suppose that the standard deviation of the

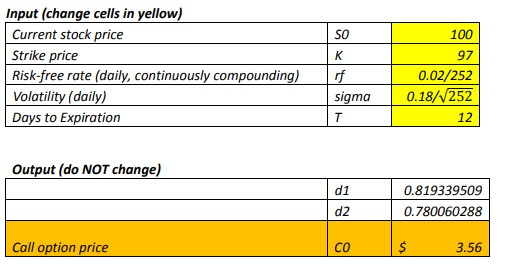

the following example is provided to answer the questions below: The stock A is currently trading at $100. Suppose that the standard deviation of the stock As returns is 18%/year. If the interest rate is 2% per year, continuously compounded, what is the price of a European call option with a strike price of $97 and a maturity of 12 days?

0 = $3.56

Question 1. The stock A is currently trading at $500. Suppose that the standard deviation of the stock As returns is 30%/year. If the interest rate is 2.5% per year, continuously compounded, what is the price of a European call option with a strike price of $480 and a maturity of 90 days?

1) $28.31

2) $33.31

3) $38.31

4) $43.31

5) $48.31

Input (change cells in yellow) Current stock price Strike price Risk-free rate (daily, continuously compounding)rf Volatility (daily) Days to Expiration SO 100 97 0.02/252 sigma0.18/V252 12 Output (do NOT change) d1 d2 0.819339509 0.780060288 Call option price co 3.56Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Private Funds Where And How

Authors: Dechert LLP

2018 Edition

152650300X,1526503018