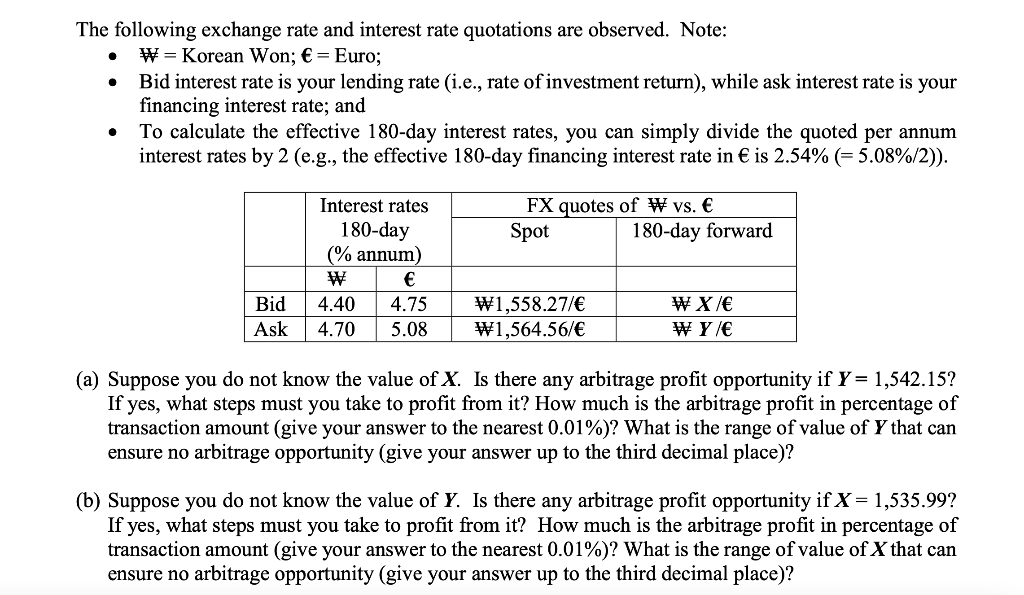

. The following exchange rate and interest rate quotations are observed. Note: W = Korean Won; = Euro; Bid interest rate is your lending rate (i.e., rate of investment return), while ask interest rate is your financing interest rate; and To calculate the effective 180-day interest rates, you can simply divide the quoted per annum interest rates by 2 (e.g., the effective 180-day financing interest rate in is 2.54% (=5.08%/2)). FX quotes of W vs. Spot 180-day forward Interest rates 180-day (% annum) W 4.40 4.75 4.70 5.08 Bid Ask W1,558.277 W1,564.56/ W X/ W Y/ (a) Suppose you do not know the value of X. Is there any arbitrage profit opportunity if Y = 1,542.15? If yes, what steps must you take to profit from it? How much is the arbitrage profit in percentage of transaction amount (give your answer to the nearest 0.01%)? What is the range of value of Y that can ensure no arbitrage opportunity (give your answer up to the third decimal place)? (b) Suppose you do not know the value of Y. Is there any arbitrage profit opportunity if X = 1,535.99? If yes, what steps must you take to profit from it? How much is the arbitrage profit in percentage of transaction amount (give your answer to the nearest 0.01%)? What is the range of value of X that can ensure no arbitrage opportunity (give your answer up to the third decimal place)? . The following exchange rate and interest rate quotations are observed. Note: W = Korean Won; = Euro; Bid interest rate is your lending rate (i.e., rate of investment return), while ask interest rate is your financing interest rate; and To calculate the effective 180-day interest rates, you can simply divide the quoted per annum interest rates by 2 (e.g., the effective 180-day financing interest rate in is 2.54% (=5.08%/2)). FX quotes of W vs. Spot 180-day forward Interest rates 180-day (% annum) W 4.40 4.75 4.70 5.08 Bid Ask W1,558.277 W1,564.56/ W X/ W Y/ (a) Suppose you do not know the value of X. Is there any arbitrage profit opportunity if Y = 1,542.15? If yes, what steps must you take to profit from it? How much is the arbitrage profit in percentage of transaction amount (give your answer to the nearest 0.01%)? What is the range of value of Y that can ensure no arbitrage opportunity (give your answer up to the third decimal place)? (b) Suppose you do not know the value of Y. Is there any arbitrage profit opportunity if X = 1,535.99? If yes, what steps must you take to profit from it? How much is the arbitrage profit in percentage of transaction amount (give your answer to the nearest 0.01%)? What is the range of value of X that can ensure no arbitrage opportunity (give your answer up to the third decimal place)