Answered step by step

Verified Expert Solution

Question

1 Approved Answer

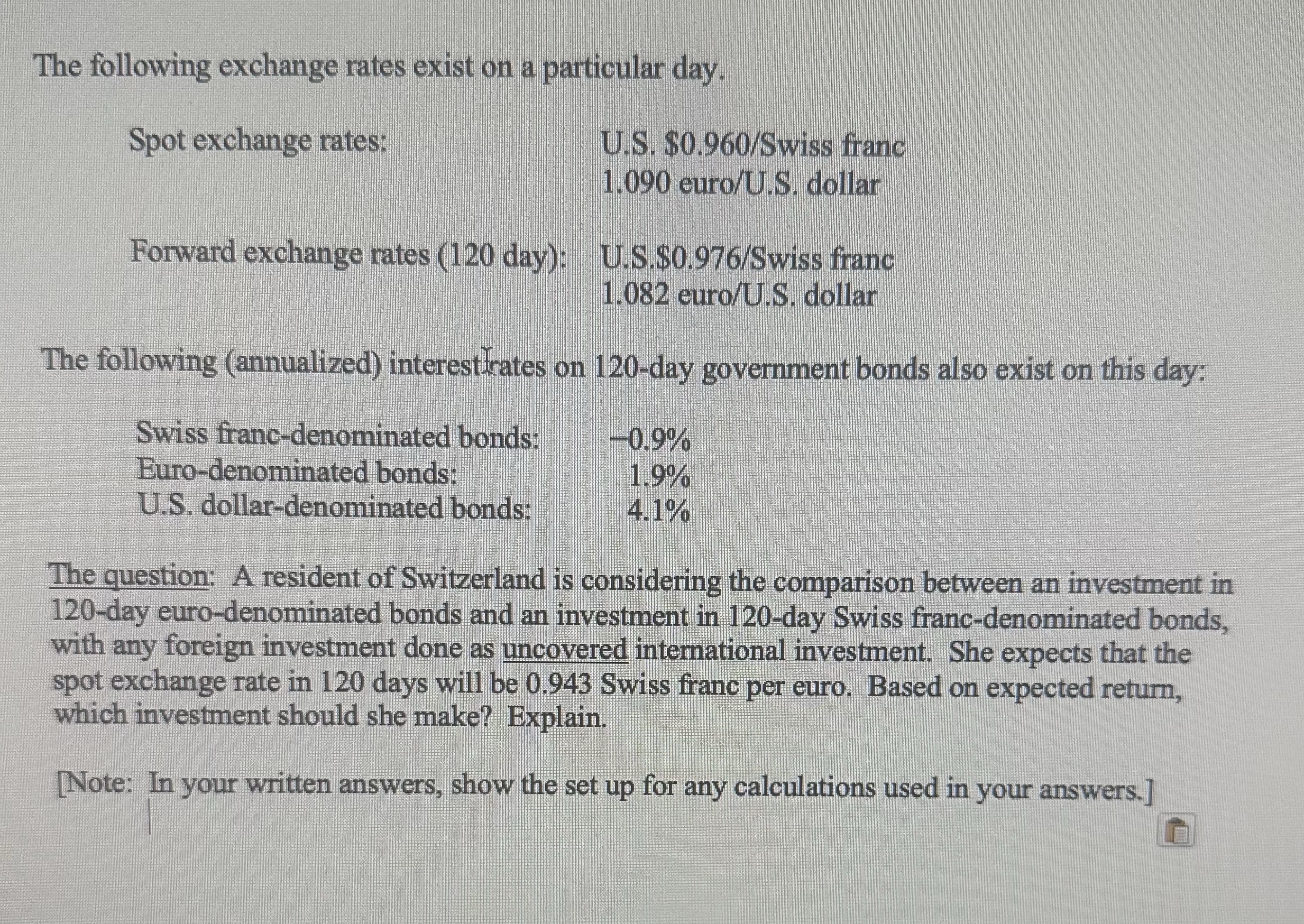

The following exchange rates exist on a particular day. Spot exchange rates: U.S. $0.960/Swiss franc 1.090 euro/U.S. dollar Forward exchange rates (120 day): U.S.$0.976/Swiss

The following exchange rates exist on a particular day. Spot exchange rates: U.S. $0.960/Swiss franc 1.090 euro/U.S. dollar Forward exchange rates (120 day): U.S.$0.976/Swiss franc 1.082 euro/U.S. dollar The following (annualized) interest rates on 120-day government bonds also exist on this day: Swiss franc-denominated bonds: U.S. dollar-denominated bonds: The question: A resident of Switzerland is considering the comparison between an investment in 120-day euro-denominated bonds and an investment in 120-day Swiss franc-denominated bonds, with any foreign investment done as uncovered international investment. She expects that the spot exchange rate in 120 days will be 0.943 Swiss franc per euro. Based on expected return, which investment should she make? Explain. [Note: In your written answers, show the set up for any calculations used in your answers.] Euro-denominated bonds: -0.9% 1.9% 4.1%

Step by Step Solution

★★★★★

3.31 Rating (142 Votes )

There are 3 Steps involved in it

Step: 1

Heres how to compare the expected returns for the Swiss resident considering eurodenominated and Swi...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Accounting

Authors: Joe Hoyle, Thomas Schaefer, Timothy Doupnik

10th edition

0-07-794127-6, 978-0-07-79412, 978-0077431808