Answered step by step

Verified Expert Solution

Question

1 Approved Answer

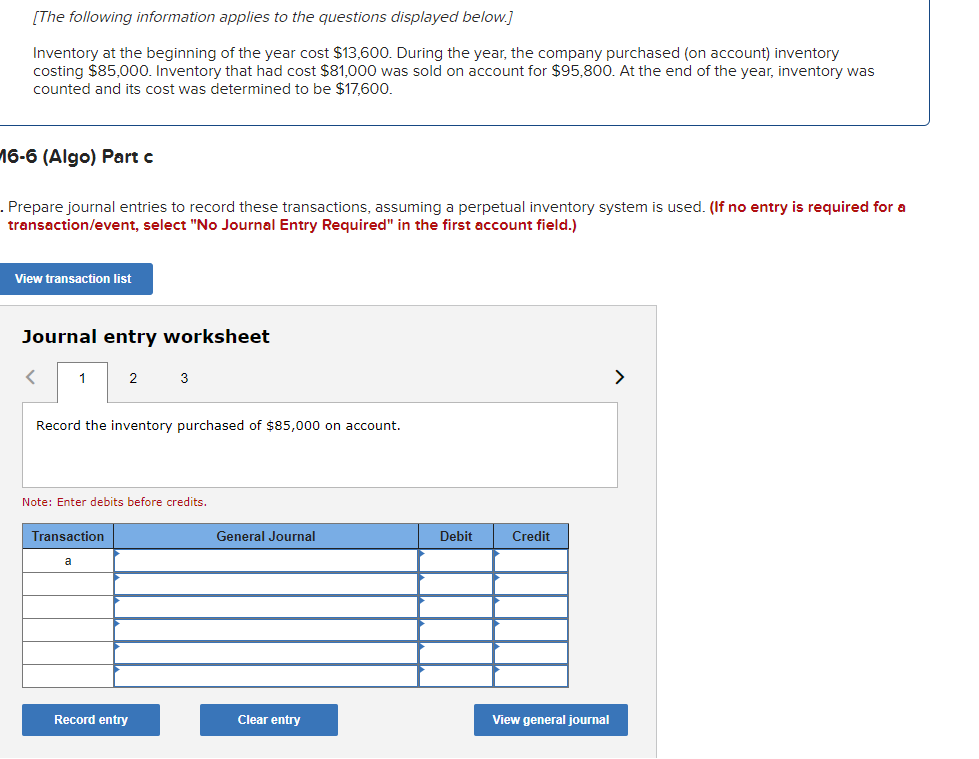

[The following information applies to the questions displayed below.] Inventory at the beginning of the year cost $13,600. During the year, the company purchased

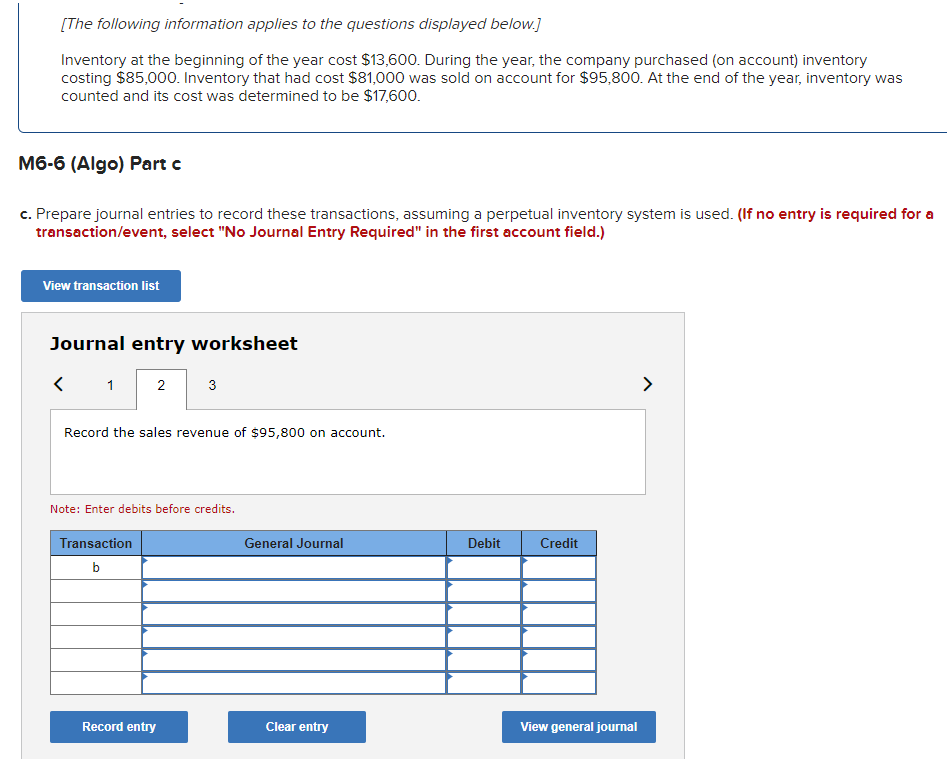

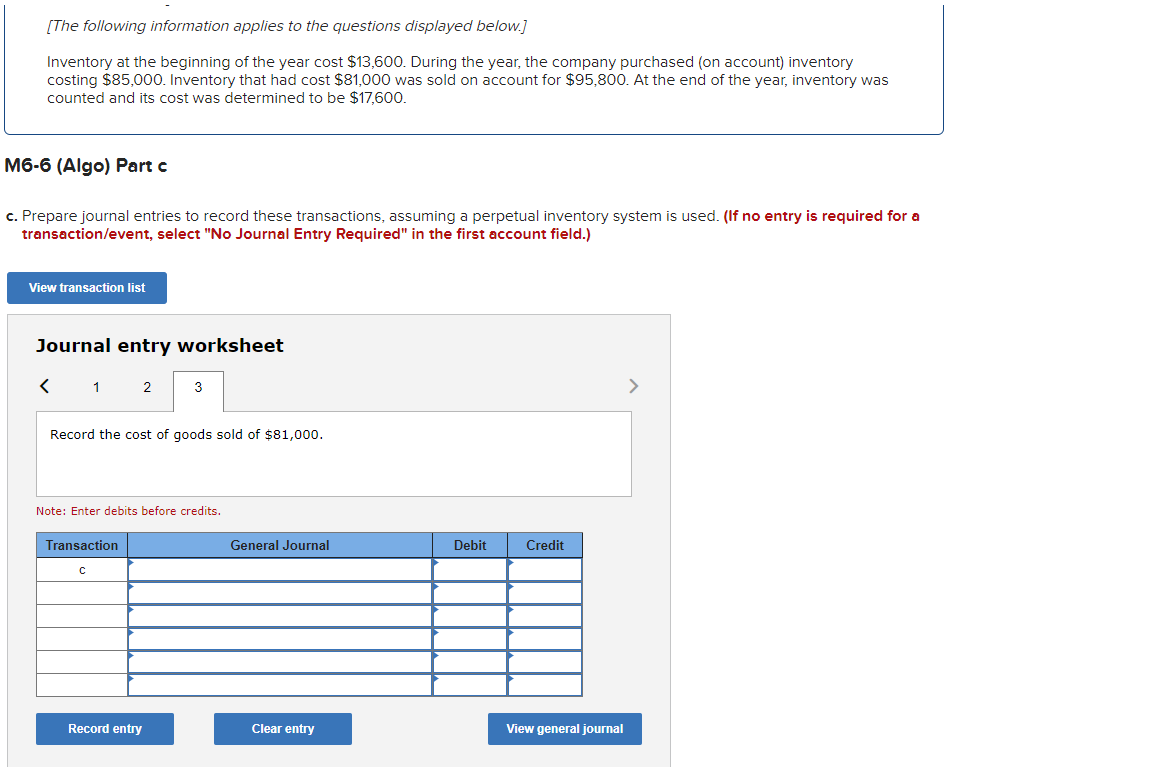

[The following information applies to the questions displayed below.] Inventory at the beginning of the year cost $13,600. During the year, the company purchased (on account) inventory costing $85,000. Inventory that had cost $81,000 was sold on account for $95,800. At the end of the year, inventory was counted and its cost was determined to be $17,600. 16-6 (Algo) Part c . Prepare journal entries to record these transactions, assuming a perpetual inventory system is used. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) View transaction list Journal entry worksheet 1 2 3 Record the inventory purchased of $85,000 on account. Note: Enter debits before credits. Transaction a General Journal Debit Credit Record entry Clear entry View general journal > [The following information applies to the questions displayed below.] Inventory at the beginning of the year cost $13,600. During the year, the company purchased (on account) inventory costing $85,000. Inventory that had cost $81,000 was sold on account for $95,800. At the end of the year, inventory was counted and its cost was determined to be $17,600. M6-6 (Algo) Part c c. Prepare journal entries to record these transactions, assuming a perpetual inventory system is used. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) View transaction list Journal entry worksheet 1 2 3 Record the sales revenue of $95,800 on account. Note: Enter debits before credits. Transaction b General Journal Debit Credit Record entry Clear entry View general journal [The following information applies to the questions displayed below.] Inventory at the beginning of the year cost $13,600. During the year, the company purchased (on account) inventory costing $85,000. Inventory that had cost $81,000 was sold on account for $95,800. At the end of the year, inventory was counted and its cost was determined to be $17,600. M6-6 (Algo) Part c c. Prepare journal entries to record these transactions, assuming a perpetual inventory system is used. (If no entry is required for a transaction/event, select "No Journal Entry Required" in the first account field.) View transaction list Journal entry worksheet < 1 2 3 Record the cost of goods sold of $81,000. Note: Enter debits before credits. Transaction C General Journal Debit Credit Record entry Clear entry View general journal >

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

Concise 6th Edition

324664559, 978-0324664553