Answered step by step

Verified Expert Solution

Question

1 Approved Answer

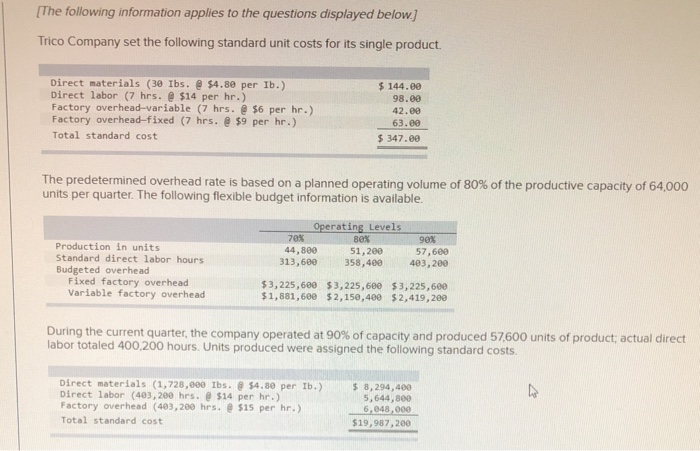

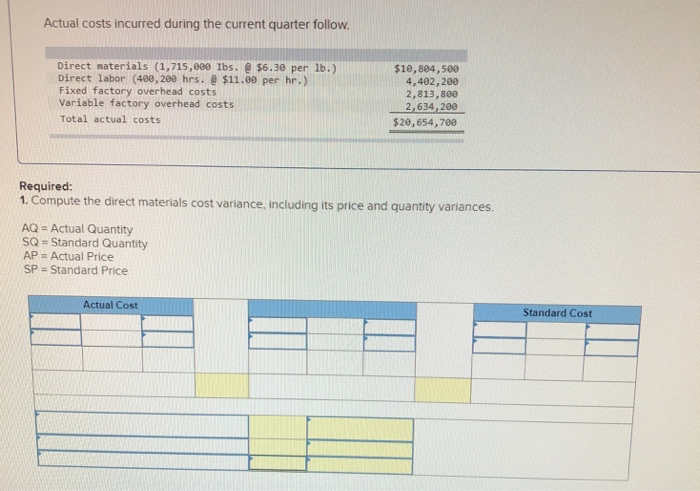

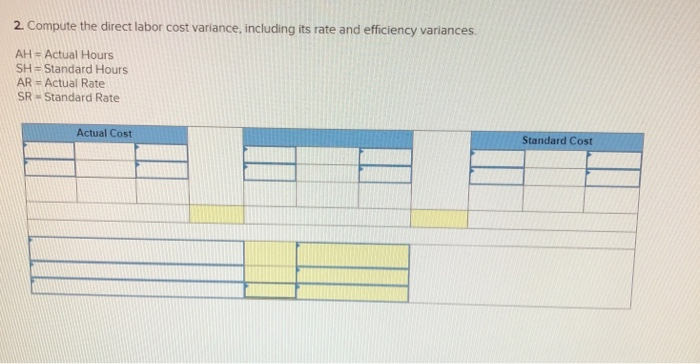

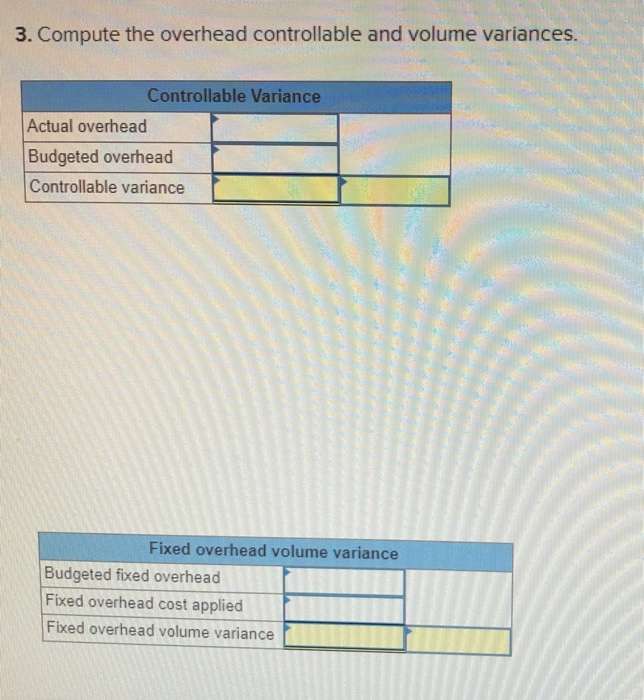

The following information applies to the questions displayed below] Trico Company set the following standard unit costs for its single product. Direct materials (30 Ibs.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Payroll Accounting

Authors: Bernard J. Bieg, Judith A. Toland

2013 edition

113396253X, 978-1133962533