Answered step by step

Verified Expert Solution

Question

1 Approved Answer

The following information refers to parts ( 1-5 ) below, select the right answer from the drop-down menu and answer the compute questions. Consider a

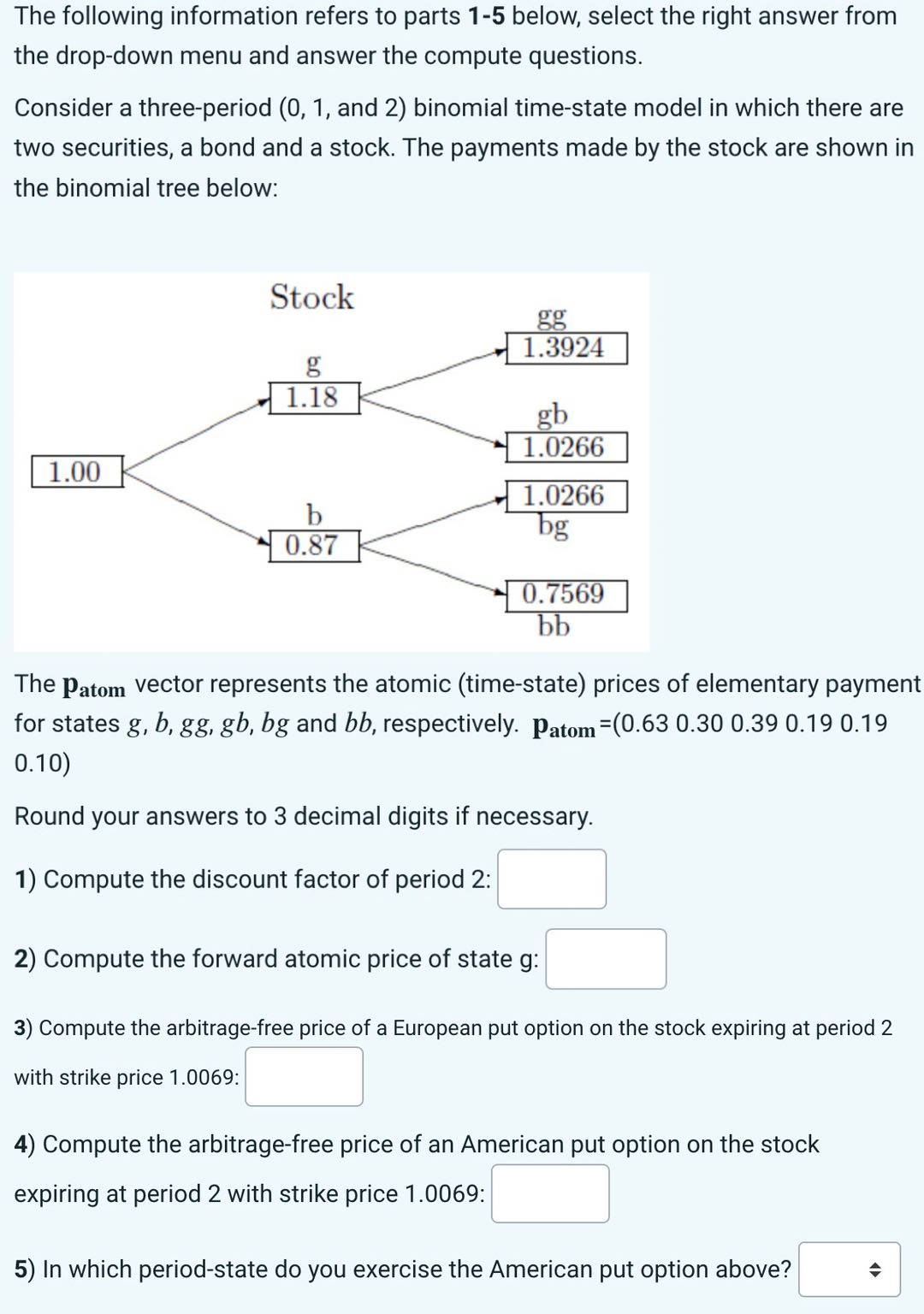

The following information refers to parts \\( 1-5 \\) below, select the right answer from the drop-down menu and answer the compute questions. Consider a three-period \\( (0,1 \\), and 2\\( ) \\) binomial time-state model in which there are two securities, a bond and a stock. The payments made by the stock are shown in the binomial tree below: The \\( \\mathbf{p}_{\\text {atom }} \\) vector represents the atomic (time-state) prices of elementary payment for states \\( g, b, g g, g b, b g \\) and \\( b b \\), respectively. patom \\( =\\left(\\begin{array}{lll}0.630 .30 & 0.390 .190 .19\\end{array}\ ight. \\) \\( 0.10) \\) Round your answers to 3 decimal digits if necessary. 1) Compute the discount factor of period 2 : 2) Compute the forward atomic price of state \\( g \\) : 3) Compute the arbitrage-free price of a European put option on the stock expiring at period 2 with strike price 1.0069: 4) Compute the arbitrage-free price of an American put option on the stock expiring at period 2 with strike price 1.0069 : 5) In which period-state do you exercise the American put option above

The following information refers to parts \\( 1-5 \\) below, select the right answer from the drop-down menu and answer the compute questions. Consider a three-period \\( (0,1 \\), and 2\\( ) \\) binomial time-state model in which there are two securities, a bond and a stock. The payments made by the stock are shown in the binomial tree below: The \\( \\mathbf{p}_{\\text {atom }} \\) vector represents the atomic (time-state) prices of elementary payment for states \\( g, b, g g, g b, b g \\) and \\( b b \\), respectively. patom \\( =\\left(\\begin{array}{lll}0.630 .30 & 0.390 .190 .19\\end{array}\ ight. \\) \\( 0.10) \\) Round your answers to 3 decimal digits if necessary. 1) Compute the discount factor of period 2 : 2) Compute the forward atomic price of state \\( g \\) : 3) Compute the arbitrage-free price of a European put option on the stock expiring at period 2 with strike price 1.0069: 4) Compute the arbitrage-free price of an American put option on the stock expiring at period 2 with strike price 1.0069 : 5) In which period-state do you exercise the American put option above Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Lectures Problems And Solutions For Ordinary Differential Equations

Authors: Yuefan Deng

1st Edition

9814632244,9814632279