The following question will focus on different ideas for saving for retirement. This type of question sometimes I find boring in its lack of understanding of the real world. In the next series of questions, we will consider how much you need to save each month to make your retirement goal. The questions does so in total isolation, without the real-world problems of paying back student loans; OR the fact that your first job is NYC and you barely have enough to pay rent, let alone save for retirement.

In what follows we will consider monthly payments into a 401(k) sponsored by your first company. If you dont know what a 401(k) is, I stolen some info., from Charles Schwab (since the UCONN Foundation pays them lots of commissions, I dont suppose they will object to me using their material ESPECIALLY if I give them credit and use it for educational purposes). Appendix II sets out background on 401(k)s. To give an alternative view I have included a recent article from CNNMoney in appendix III. If you are fortunate enough to have begun full-time work with a large financial firm. The firm offers a 401(k). How much do you need to retire what should be your goal? There are many rules of thumb that exist in practice. There is the 10x rule plan on saving 10x your final salary for retirement of course, maybe difficult to know your final salary when your currently 22! But possibly, if you have an idea of what type of profession you wish to be in, you can likely find data on expected salaries at retirement. Thus, if you estimate your final salary as $500K before you retire, $5million in retirement assets is sometimes used as a rule of thumb. There is the following method also taken from Charles Schwab: To estimate how much annual income youll need from your portfolio only, take the amount you expect to spend in your first year of retirement and subtract pensions, Social Security and other non-savings sources of income. In terms of savings, a common rule of thumb is to aim for a portfolio that is 25 times the size of that initial portfolio withdrawal by the time you retire to have a high degree of confidence that your savings will go the distance (see Do the math, below).

In what follows, suppose you wish to have saved $4million by the time you retire at the age of 65. You will assume that social security will pay nothing by then, thus, only your savings for retirement will get you to the $4million goal. At the age of 25 you finally have enough salary to begin saving and intend to make monthly payments from your paycheck into your firms 401(k) plan (I have included an article from CNN Money explaining the basics of a 401(k) in appendix III)

a. You decide to invest in a broad market ETF, the SPY. If the monthly return on the market is expected to be .6% per month, how much will you have saved in your 401(k) by the time you retire?

b. You have read somewhere online about the 60/40 rule (see Appendices IV and V), and instead decide to invest in a mix of stocks and bonds. If the monthly expected rate of return of this strategy is .5%, how will this change you answer?

c. Having decided, based on the answers to a) and b), that you will remain 100% invested in the SPY, how much will you need to save per month if you wait until your 30th birthday to start saving?

d. How about your 40th birthday?

here is the appendix

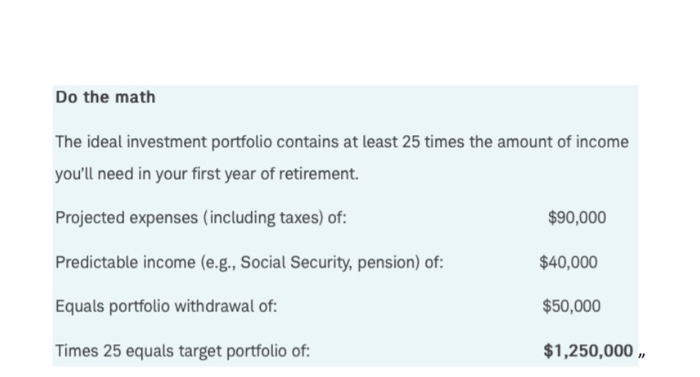

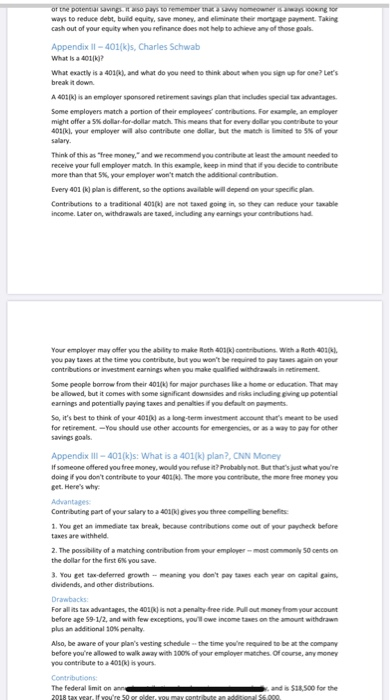

Do the math The ideal investment portfolio contains at least 25 times the amount of income you'll need in your first year of retirement. Projected expenses (including taxes) of: $90,000 Predictable income (e.g., Social Security, pension) of: $40,000 Equals portfolio withdrawal of: $50,000 Times 25 equals target portfolio of: $1,250,000, of the potenting to pays to remember that a wy homeowners ongo ways to reduce debt, build equity. Save money, and eliminate the mortgage payment. Taking cash out of your equity when you refinance does not help to achieve any of those goals Appendix il-401(k), Charles Schwab What is a 401 for one? Let's What exactly is a 401(k), and what do you need to think about when you break it down A 401(k) is an employer sponsored retirement savings plan that includes special advantages Some employers match a portion of their employees' contributions. For comple, an employer might offer a 5 dollar-for-dollar match. This means that for every dollar you contribute to your 401Kl. your employer will also contribution dollar, but the match is limited to 5% of your salary. Think of this as "free money and we recommend you contribute at least the amount needed to receive your full employer match. In this example, keep in mind that if you decide to contribute more than that 5% your employer won't match the additional contribution Every 401(k) plan is different, so the options available will depend on your specific plan Contributions to a traditional 4011) e notted going in so they can reduce your taxable income. Later on, withdrawals are taxed, including any earning your contributions had Your employer may offer you the ability to make Roth 403) contribution. With a Roth 401) you pay taxes at the time you contribute, but you won't be required to pay we again on your contributions or investment earnings when you make qualified withdrawals in retirement Some people borrow from their 401(k) for major purchases like a home or education. That may be allowed, but it comes with some slicant downsides and includinging up potential earnings and potentially paying taxes and penalties if you default on payments So, it's best to think of your 4010) as a long-term investment account that's meant to be used for retirement. You should use other accounts for emergencies, or as a way to pay for other Appendix lll-401(k)s: What is a 401(k) plan?, CNN Money If someone offered you free money, would you refuse? Probably not. But that's just what you're doing if you don't contribute to your 4011). The more you contribute the more free money you get. Here's why Advantages Contributing part of your salary to a 401 gives you three compelling benefits 1. You get an immediate tax break, because contributions come out of your paycheck before taxes are withheld. 2. The possibility of a matching contribution from your employer most commonly 50 cents on the dollar for the first 6 you save. 3. You get tax-deferred growth -- meaning you don't pay to each year on capital gains, dividends, and other distributions. Drawbacks For all its tax advantages, the 401) is not a penalty free ride Pull out money from your account before age 59-1/2, and with few exceptions, you'll we income taxes on the amount withdrawn plus an additional 10% penalty Also, be aware of your plan's vesting schedule the time you're required to be at the company before you're allowed to walk away with 100% of your employer matches. Of course, any money you contribute to a 401(k) is yours. Contributions The federal limit on 2018 tax year. If you're 50 or older, you and is $18.500 for the 56 000 contribute to Appendix lll - 401(k)s: What is a 401(k) plan?, CNN Money If someone offered you free money, would you refuse it? Probably not. But that's just what you're doing if you don't contribute to your 401(k). The more you contribute the more free money you get. Here's why Advantages Contributing part of your salary to a 401) gives you three compelling benefits 1. You get an immediate tax break, because contributions come out of your paycheck before taxes are withheld. 2. The powubility of a matching contribution from your employer most commonly 50 cents on the dollar for the first you save. 3. You get tax deferred growth - meaning you don't pay taxes each year on capital gains, dividends, and other distributions Drawbacks For all its tax advantages, the 4011) is not a penalty-free ride Pull out money from your account before age 59-1/2, and with few exceptions, you'll owe income taxes on the amount withdrawn plus an additional 10 penalty. Also, be aware of your plan's vesting schedule - the time you're required to be at the company before you're allowed to walk away with 100% of your employer matches. Of course, any money you contribute to a 401(k) is yours. Contributions The federal limit on annual contributions has been increasing gradually, and is $18,500 for the 2018 tax year. If you're 50 or older, you may contribute an additional $6,000 Keep in mind, however, that while federal low sets the puidelines for what's permissible in 4011) plans, your employer may set tighter restrictions What's more, there are other federal non-discrimination tests a 4011) plan must meet, one of which applies to "highly compensated employees. So if you make more than $120,000 a year in 2018, you may not be permitted to contribute as high a percentage of your salary as some of your lower paid colleagues So how much should you put away? First you need to consider how much you'll need and how many years you have until retirement. Typically, financial planners recommend you save at least 10% of your income if possible. If you can't afford to sock away 30%, contribute at least enough to get the full employer match, For starters, figure out what your mix of stocks, bonds, and cash or asset allocation should be. There are two key factors to consider when picking your a t allocation your risk tolerance and how many years you have left before retirement. (For help in figuring out the best allocation for yow, try our asset allocator) But not all 4011)s are created equal. Some are better than others, particularly when it comes to the breadth of investment choices. There are four things to look for in picking a good fund Better than average returns: A fund, if it's worth your while, should have performed in the top half, and ideally the top 25% of its peer group over a three, five, and 10-year time span. Low price A fund's expense ratio - what you are charged annually and what will lower your overall return should not exceed the average among the funds peers. Solid management: If you're opting for an actively managed fund (as opposed to an index fund). the manager should have a solid track record of experience. Reasonable size: Sometimes when a fund becomes too popular, its asset base - the dollars invested in the fund -gets bloated. That means the manager can't move in and out of a stock too quickly without moving the market. In picking the right funds for your portfolio, make sure you diversify your investments. That means don't over-invest in n e investment style such as growth stocks or value stocks. Do the math The ideal investment portfolio contains at least 25 times the amount of income you'll need in your first year of retirement. Projected expenses (including taxes) of: $90,000 Predictable income (e.g., Social Security, pension) of: $40,000 Equals portfolio withdrawal of: $50,000 Times 25 equals target portfolio of: $1,250,000, of the potenting to pays to remember that a wy homeowners ongo ways to reduce debt, build equity. Save money, and eliminate the mortgage payment. Taking cash out of your equity when you refinance does not help to achieve any of those goals Appendix il-401(k), Charles Schwab What is a 401 for one? Let's What exactly is a 401(k), and what do you need to think about when you break it down A 401(k) is an employer sponsored retirement savings plan that includes special advantages Some employers match a portion of their employees' contributions. For comple, an employer might offer a 5 dollar-for-dollar match. This means that for every dollar you contribute to your 401Kl. your employer will also contribution dollar, but the match is limited to 5% of your salary. Think of this as "free money and we recommend you contribute at least the amount needed to receive your full employer match. In this example, keep in mind that if you decide to contribute more than that 5% your employer won't match the additional contribution Every 401(k) plan is different, so the options available will depend on your specific plan Contributions to a traditional 4011) e notted going in so they can reduce your taxable income. Later on, withdrawals are taxed, including any earning your contributions had Your employer may offer you the ability to make Roth 403) contribution. With a Roth 401) you pay taxes at the time you contribute, but you won't be required to pay we again on your contributions or investment earnings when you make qualified withdrawals in retirement Some people borrow from their 401(k) for major purchases like a home or education. That may be allowed, but it comes with some slicant downsides and includinging up potential earnings and potentially paying taxes and penalties if you default on payments So, it's best to think of your 4010) as a long-term investment account that's meant to be used for retirement. You should use other accounts for emergencies, or as a way to pay for other Appendix lll-401(k)s: What is a 401(k) plan?, CNN Money If someone offered you free money, would you refuse? Probably not. But that's just what you're doing if you don't contribute to your 4011). The more you contribute the more free money you get. Here's why Advantages Contributing part of your salary to a 401 gives you three compelling benefits 1. You get an immediate tax break, because contributions come out of your paycheck before taxes are withheld. 2. The possibility of a matching contribution from your employer most commonly 50 cents on the dollar for the first 6 you save. 3. You get tax-deferred growth -- meaning you don't pay to each year on capital gains, dividends, and other distributions. Drawbacks For all its tax advantages, the 401) is not a penalty free ride Pull out money from your account before age 59-1/2, and with few exceptions, you'll we income taxes on the amount withdrawn plus an additional 10% penalty Also, be aware of your plan's vesting schedule the time you're required to be at the company before you're allowed to walk away with 100% of your employer matches. Of course, any money you contribute to a 401(k) is yours. Contributions The federal limit on 2018 tax year. If you're 50 or older, you and is $18.500 for the 56 000 contribute to Appendix lll - 401(k)s: What is a 401(k) plan?, CNN Money If someone offered you free money, would you refuse it? Probably not. But that's just what you're doing if you don't contribute to your 401(k). The more you contribute the more free money you get. Here's why Advantages Contributing part of your salary to a 401) gives you three compelling benefits 1. You get an immediate tax break, because contributions come out of your paycheck before taxes are withheld. 2. The powubility of a matching contribution from your employer most commonly 50 cents on the dollar for the first you save. 3. You get tax deferred growth - meaning you don't pay taxes each year on capital gains, dividends, and other distributions Drawbacks For all its tax advantages, the 4011) is not a penalty-free ride Pull out money from your account before age 59-1/2, and with few exceptions, you'll owe income taxes on the amount withdrawn plus an additional 10 penalty. Also, be aware of your plan's vesting schedule - the time you're required to be at the company before you're allowed to walk away with 100% of your employer matches. Of course, any money you contribute to a 401(k) is yours. Contributions The federal limit on annual contributions has been increasing gradually, and is $18,500 for the 2018 tax year. If you're 50 or older, you may contribute an additional $6,000 Keep in mind, however, that while federal low sets the puidelines for what's permissible in 4011) plans, your employer may set tighter restrictions What's more, there are other federal non-discrimination tests a 4011) plan must meet, one of which applies to "highly compensated employees. So if you make more than $120,000 a year in 2018, you may not be permitted to contribute as high a percentage of your salary as some of your lower paid colleagues So how much should you put away? First you need to consider how much you'll need and how many years you have until retirement. Typically, financial planners recommend you save at least 10% of your income if possible. If you can't afford to sock away 30%, contribute at least enough to get the full employer match, For starters, figure out what your mix of stocks, bonds, and cash or asset allocation should be. There are two key factors to consider when picking your a t allocation your risk tolerance and how many years you have left before retirement. (For help in figuring out the best allocation for yow, try our asset allocator) But not all 4011)s are created equal. Some are better than others, particularly when it comes to the breadth of investment choices. There are four things to look for in picking a good fund Better than average returns: A fund, if it's worth your while, should have performed in the top half, and ideally the top 25% of its peer group over a three, five, and 10-year time span. Low price A fund's expense ratio - what you are charged annually and what will lower your overall return should not exceed the average among the funds peers. Solid management: If you're opting for an actively managed fund (as opposed to an index fund). the manager should have a solid track record of experience. Reasonable size: Sometimes when a fund becomes too popular, its asset base - the dollars invested in the fund -gets bloated. That means the manager can't move in and out of a stock too quickly without moving the market. In picking the right funds for your portfolio, make sure you diversify your investments. That means don't over-invest in n e investment style such as growth stocks or value stocks