Answered step by step

Verified Expert Solution

Question

1 Approved Answer

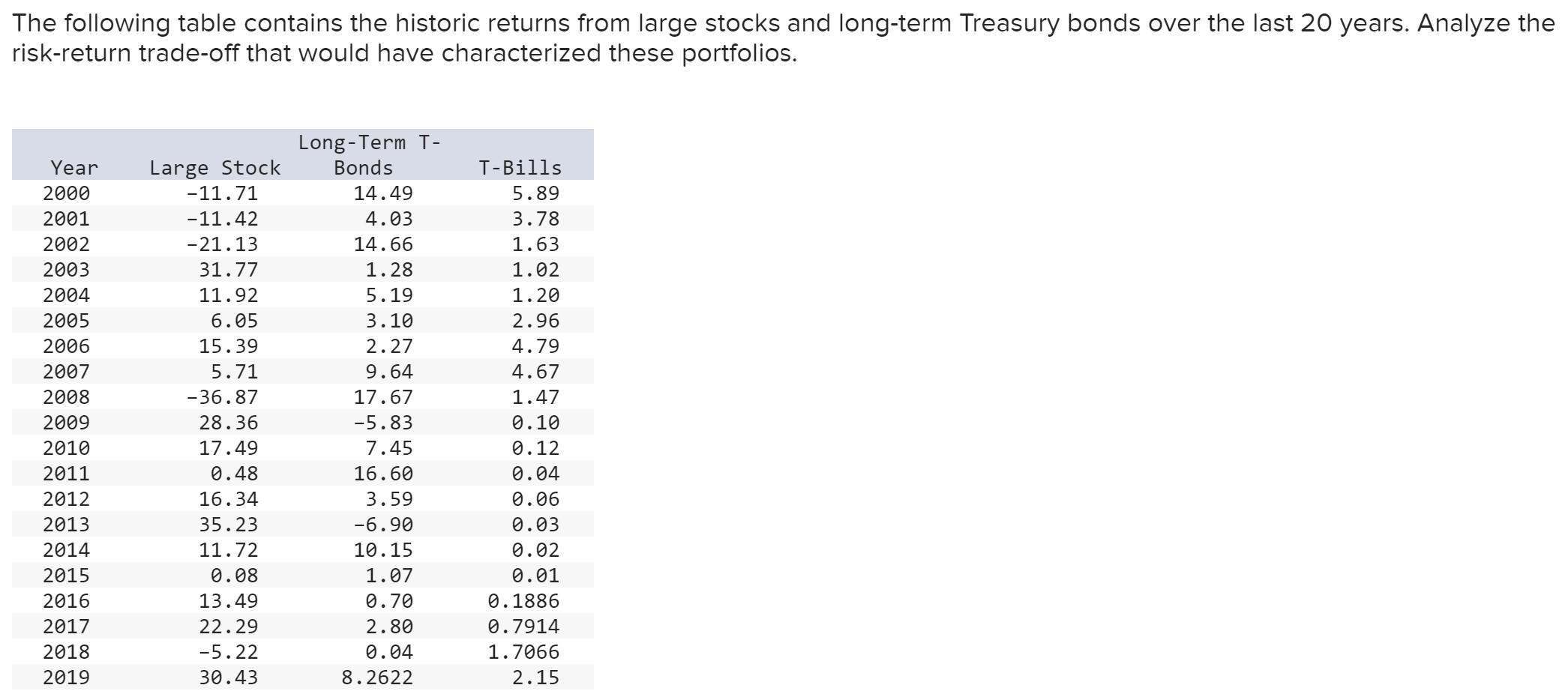

The following table contains the historic returns from large stocks and long-term Treasury bonds over the last 20 years. Analyze the risk-return trade-off that would

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The New Reality Of Wall Street An Investors Survival Guide To Triple Waterfalls And Other Stock Market Perils

Authors: Donald Coxe

1st Edition

0071417532