Question

The golf Shore Time Value Analysis: Instructions: From the Casebook , use Case #11 and answer the following questions: 1. As a starting point, use

The golf Shore Time Value Analysis:

The golf Shore Time Value Analysis:

Instructions: From the Casebook , use Case #11 and answer the following questions:

1. As a starting point, use last years allocation of $600,000 for base salary and $120,000 for bonuses. What would be the total compensation of each physician if performance pay is based solely on a productivity measure only? That is, 100 percent of performance pay based on patient visits (0 percent for all other productivity, financial, and quality measures), 100 percent based on work RVUs, or 100 percent based on professional procedures.

2. Now, focus exclusively on a financial performance measure. That is, 100 percent of performance pay based on gross charges (0 percent for all other productivity, financial and quality measures), 100 percent based on net collections, or 100 percent based on net income before physician compensation.

3.Finally,what if only a quality measure is used? That is, 100 percent of performance pay based on average patient satisfaction score (0 percent for all other productivity, financial and quality measures), 100 percent based on blood pressure control target met, or 100 percent based on breast cancer screening target met.

4. One physician wants to base all compensation on performance. Assume that all of last years total compensation of $720,000 is allocated based on a single performance measure. What would be the total compensation of each physician based on each financial, productivity and quality measure? Would it be wise to use this approach?

Please be as descriptive as possible elementry level! thanks

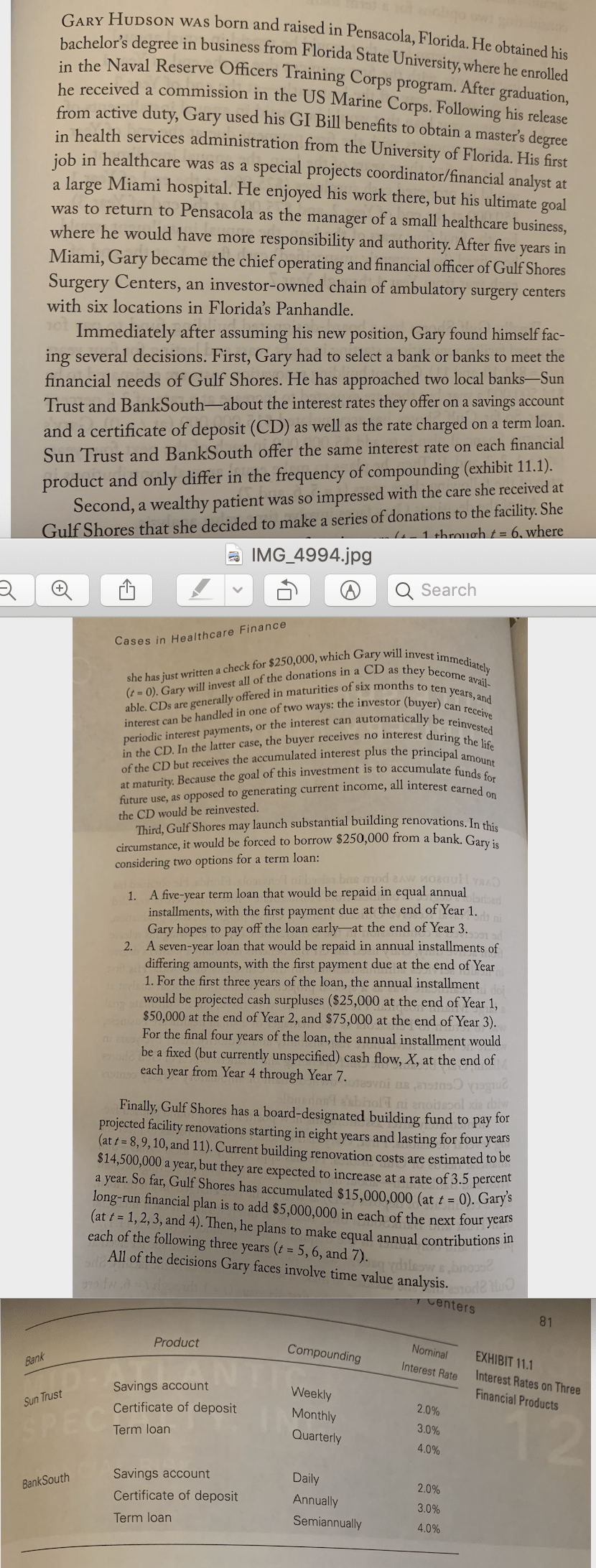

GARY HUDSON WAS born and raised in SON was born and raised in Pensacola, Florida. He obtained his bachelor's degree in business from Florid erree in business from Florida State University, where he enrolled in the Naval Reserve Officers Training Corps program. After graduation, he received a commission in the US Marine Corps. Following his release from active duty, Gary used his GI Bill benefits to obtain a master's degree in health services administration from the University of Florida. His first job in healthcare was as a special projects coordinator/financial analyst at a large Miami hospital. He enjoyed his work there, but his ultimate goal was to return to Pensacola as the manager of a small healthcare business, where he would have more responsibility and authority. After five years in Miami, Gary became the chief operating and financial officer of Gulf Shores Surgery Centers, an investor-owned chain of ambulatory surgery centers with six locations in Florida's Panhandle. Immediately after assuming his new position, Gary found himself fac- ing several decisions. First, Gary had to select a bank or banks to meet the financial needs of Gulf Shores. He has approached two local banksSun Trust and BankSouth-about the interest rates they offer on a savings account and a certificate of deposit (CD) as well as the rate charged on a term loan. Sun Trust and BankSouth offer the same interest rate on each financial product and only differ in the frequency of compounding (exhibit 11.1). Second, a wealthy patient was so impressed with the care she received at Gulf Shores that she decided to make a series of donations to the facility. She 1.1 through t = 6, where a IMG_4994.jpg R Q v @ Q Search Cases in Healthcare Finance Il invest immediately as they become avail- nths to ten years, and restor (buyer) can receive she has just written a check for $250,000, which Gary will in (1 - 0). Gary will invest all of the donations in a CD as they able. CDs are generally offered in maturities of six mont interest can be handled in one of two ways: the investor (bu est payments, or the interest can automatically be in the CD. In the latter case, the buyer receives no interest du of the CD but receives the accumulated interest plus the princin at maturity. Because the goal of this investment is to accumulate future use, as opposed to generating current income, all interest the CD would be reinvested. Third, Gulf Shores may launch substantial building renovations. In the circumstance, it would be forced to borrow $250,000 from a bank C. considering two options for a term loan: interest during the life us the principal amount accumulate funds for all interest earned on od 10 1. A five-year term loan that would be repaid in equal annual installments, with the first payment due at the end of Year 1. Gary hopes to pay off the loan early-at the end of Year 3. 2. A seven-year loan that would be repaid in annual installments of differing amounts, with the first payment due at the end of Year 1. For the first three years of the loan, the annual installment would be projected cash surpluses ($25,000 at the end of Year 1, $50,000 at the end of Year 2, and $75,000 at the end of Year 3). For the final four years of the loan, the annual installment would be a fixed (but currently unspecified) cash flow, X, at the end of each year from fear 4 through rear 7. V G bhole ni anonoolib Finally, Gulf Shores has a board-designated building fund to pay for projected facility renovations starting in eight years and lasting for four years (at t = 8,9,10, and 11). Current building renovation costs are estimated to be $14,500,000 a year, but they are expected to increase at a rate of 3.5 percent a year. So far, Gulf Shores has accumulated $15,000,000 (at t = 0). Gary long-run financial plan is to add $5,000,000 in each of the next four years (at t = 1, 2, 3, and 4). Then, he plans to make equal annual contributions each of the following three years (t = 5, 6, and 7). All of the decisions Gary faces involve time value analysis. lesbro centers 81 Product Compounding Nominal Interest Rate EXHIBIT 11.1 Interest Rates on Three Financial Products Weekly Sun Trust Savings account Certificate of deposit Term loan 2.0% Monthly Quarterly 3.0% 4.0% BankSouth 2.0% Savings account Certificate of deposit Term loan Daily Annually Semiannually 3.0% 4.0% GARY HUDSON WAS born and raised in SON was born and raised in Pensacola, Florida. He obtained his bachelor's degree in business from Florid erree in business from Florida State University, where he enrolled in the Naval Reserve Officers Training Corps program. After graduation, he received a commission in the US Marine Corps. Following his release from active duty, Gary used his GI Bill benefits to obtain a master's degree in health services administration from the University of Florida. His first job in healthcare was as a special projects coordinator/financial analyst at a large Miami hospital. He enjoyed his work there, but his ultimate goal was to return to Pensacola as the manager of a small healthcare business, where he would have more responsibility and authority. After five years in Miami, Gary became the chief operating and financial officer of Gulf Shores Surgery Centers, an investor-owned chain of ambulatory surgery centers with six locations in Florida's Panhandle. Immediately after assuming his new position, Gary found himself fac- ing several decisions. First, Gary had to select a bank or banks to meet the financial needs of Gulf Shores. He has approached two local banksSun Trust and BankSouth-about the interest rates they offer on a savings account and a certificate of deposit (CD) as well as the rate charged on a term loan. Sun Trust and BankSouth offer the same interest rate on each financial product and only differ in the frequency of compounding (exhibit 11.1). Second, a wealthy patient was so impressed with the care she received at Gulf Shores that she decided to make a series of donations to the facility. She 1.1 through t = 6, where a IMG_4994.jpg R Q v @ Q Search Cases in Healthcare Finance Il invest immediately as they become avail- nths to ten years, and restor (buyer) can receive she has just written a check for $250,000, which Gary will in (1 - 0). Gary will invest all of the donations in a CD as they able. CDs are generally offered in maturities of six mont interest can be handled in one of two ways: the investor (bu est payments, or the interest can automatically be in the CD. In the latter case, the buyer receives no interest du of the CD but receives the accumulated interest plus the princin at maturity. Because the goal of this investment is to accumulate future use, as opposed to generating current income, all interest the CD would be reinvested. Third, Gulf Shores may launch substantial building renovations. In the circumstance, it would be forced to borrow $250,000 from a bank C. considering two options for a term loan: interest during the life us the principal amount accumulate funds for all interest earned on od 10 1. A five-year term loan that would be repaid in equal annual installments, with the first payment due at the end of Year 1. Gary hopes to pay off the loan early-at the end of Year 3. 2. A seven-year loan that would be repaid in annual installments of differing amounts, with the first payment due at the end of Year 1. For the first three years of the loan, the annual installment would be projected cash surpluses ($25,000 at the end of Year 1, $50,000 at the end of Year 2, and $75,000 at the end of Year 3). For the final four years of the loan, the annual installment would be a fixed (but currently unspecified) cash flow, X, at the end of each year from fear 4 through rear 7. V G bhole ni anonoolib Finally, Gulf Shores has a board-designated building fund to pay for projected facility renovations starting in eight years and lasting for four years (at t = 8,9,10, and 11). Current building renovation costs are estimated to be $14,500,000 a year, but they are expected to increase at a rate of 3.5 percent a year. So far, Gulf Shores has accumulated $15,000,000 (at t = 0). Gary long-run financial plan is to add $5,000,000 in each of the next four years (at t = 1, 2, 3, and 4). Then, he plans to make equal annual contributions each of the following three years (t = 5, 6, and 7). All of the decisions Gary faces involve time value analysis. lesbro centers 81 Product Compounding Nominal Interest Rate EXHIBIT 11.1 Interest Rates on Three Financial Products Weekly Sun Trust Savings account Certificate of deposit Term loan 2.0% Monthly Quarterly 3.0% 4.0% BankSouth 2.0% Savings account Certificate of deposit Term loan Daily Annually Semiannually 3.0% 4.0%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Theory

Authors: Craig Deegan

3rd Edition

0070277265, 978-0070277267