Answered step by step

Verified Expert Solution

Question

1 Approved Answer

The help for this would be extremely highly appreciated and thanked for! Our controller, Tommy Swain is negotiating with potential new Wood suppliers in Kentucky.

The help for this would be extremely highly appreciated and thanked for!

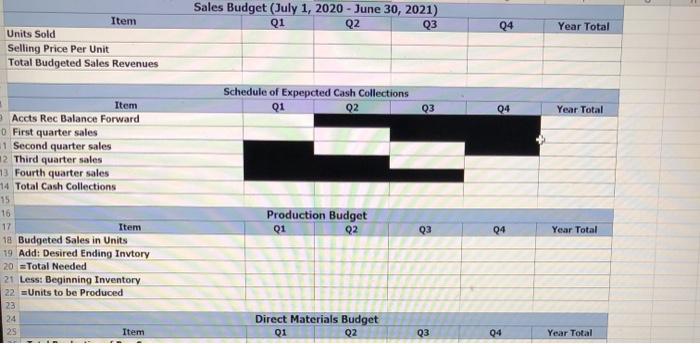

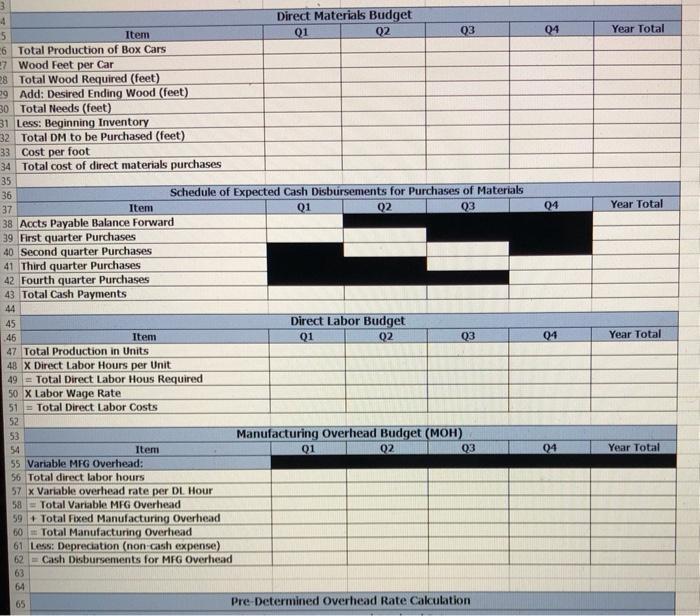

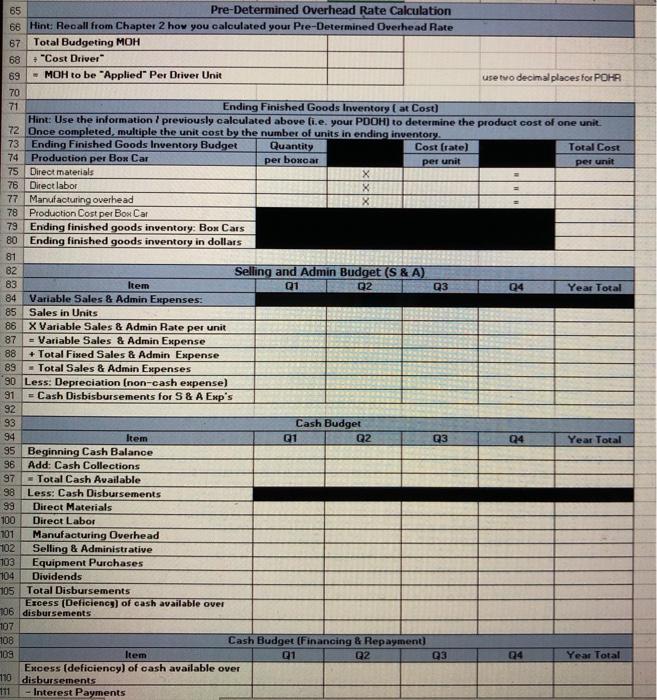

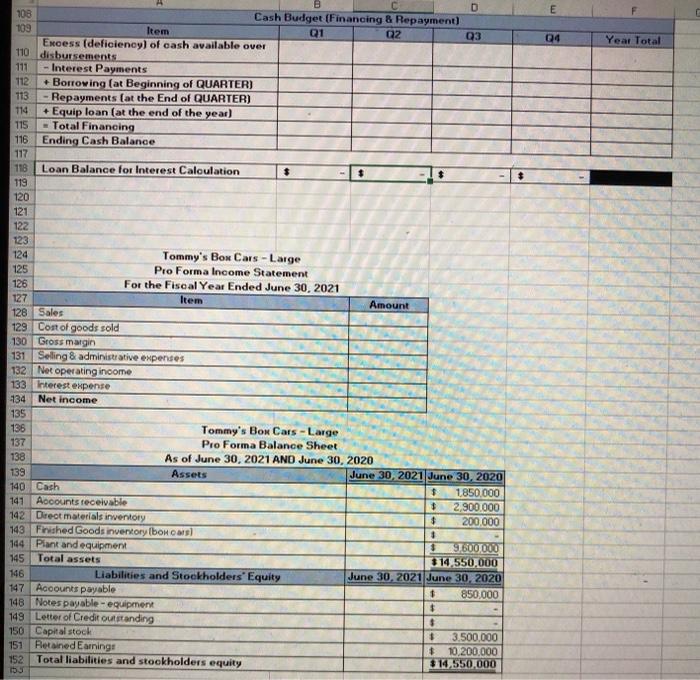

Our controller, Tommy Swain is negotiating with potential new Wood suppliers in Kentucky. We need the Large Box Car Division's Master Budget for the fiscal year ended (36) June 30, 2021 for our corporate strategic planning process, and we cannot wait for Tommy's return from Kentucky. We would like you to prepare the Large Box Car Division's Master Budget for the fiscal year ended June 30, 2021. The deliverables are as follows: 1. Sales budget, including a schedule of expected cash collections. 2. Production budget. 3. Direct materials budget, including a schedule of expected cash disbursements for materials. 4. Direct labor budget. 5. Manufacturing overhead budget. 6. Ending finished goods inventory budget calculating the expected value of the finished goods inventory as of (36) June 30, 2021. * 7. Selling and administrative expense budget. 8. Cash budget. 9. Budgeted Income statement for the year ended (36) June 30, 2021. * 10. Budgeted balance sheet for (36) June 30, 2021. * All the Master Budget schedules except those marked with an asterisk for the Large Box Car Division should include a column for each quarter and a total column for the fiscal year. We only need annual totals for the budgeted financial statements (schedules 9 and 10) and we only need a year-end total for the value of finished goods inventory (schedule 6). The hard copies of these budget schedules should be delivered by the company deadline. You can print more than one schedule per page, but do not have a page break in the middle of a budget schedule. I like to be able to view an entire budget schedule without flipping back and forth between pages. Please also use a type font of between 10-12 points for printing. We also need you to submit (via e-mail) the Excel spreadsheet that you used to create the budget schedules you print so we can use the spreadsheet as a starting point for future budgets. Upload the Excel spreadsheet on Blackboard. We need that spreadsheet file the night before the meeting. I've attached a brief description of the Large Box Car Division to the budget data Tommy gave me before he left for Kentucky. We eagerly await your results. Sincerely, Tommy's Box Cars During 2019-20 fiscal year, the average selling price for large box cars is expected to be (1) $115 per car. The Large Box Car Division forecasts the following units of sales. Fourth Quarter Box Car UNIT Sales (2-5) First 65,000 Second 70,000 Third 60,000 65,000 O The collection pattern for Accounts Receivable is as follows: o (6) 50 percent of all sales are collected within the quarter in which they are sold o (7) 50 percent of all sales are collected in the following quarter. There are no bad debts/uncollectible accounts. Due to high demand last year, the Large Box Car Division expects to have (8) zero finished box cars in inventory on (35) July 1, 2020, the beginning of the first quarter of the new fiscal year (i.e. Beginning Finished Goods Inventory is (8) Zero). To avoid having that problem in the coming fiscal year, the Large Box Car Division would like to have the ending inventory of Box Car at the end of each of the first three quarters equal to (9) 30% of the budgeted sales for the next quarter. They would like to have (10) 10,000 finished Box Cars on hand on (36) June 30, 2021. First Second Third Fourth Quarter Ending FG inventory of Box Cars as a % of the next quarter's budgeted sales (9) Ending FG inventory of Box Cars (10) 30% 30% 30% 2 ? 2 ? 10,000 Each large box car requires an average of (11) 5.0 feet of wood. The Large Box Car Division buys wood for (13) $4.00 per foot and they expect the price to remain constant throughout the year. They expect to have (12) 50,000 feet of wood (RAW MATERIALS) on hand as of July 1, 2019((12) 50,000 * ((13) $4.00 = (14) $200,000 - This is beginning Direct Material Inventory), the beginning of the first quarter of the fiscal year. At the end of each of the first three quarters, the Large Box Car Division would like to have their direct materials inventory quantity to equal (15) 25 percent of the amount required for the following quarter's planned production. On (36) June 30, 2021, the end of the fiscal year, Large Box Car Division would like to have (16) 60,000 feet of wood on hand (This is ending Direct Material Inventory).. Third 25% ? ? ? Quarter First Second Fourth Ending DM inventory as a % of the next quarter's production 25% 25% requirement (15) Ending DM inventory in feet (16) ? 60,000 The Large Box Car Division buys its wood on account. It pays for (17) 30% of its purchases of direct materials in the quarter in which they were purchased and (18) 70% in the quarter after they were purchased. Each large box car requires (19) 5 hours of direct labor. Employees engaged in direct labor will be paid an estimated (20) $11.00 per labor hour. Wages and salaries are paid on the 15 and 30th of each month. Variable manufacturing overhead is estimated to be (21) $3.75 per direct labor hour for the coming fiscal year. All variable manufacturing overhead expenses are paid for in the quarter incurred. 2 Tommy's Box Cars Fixed manufacturing overhead is estimated to total (22) $120,000 each quarter, with (23) $40,000 out of the total amount of (22) $120,000 representing depreciation on machinery, equipment and the factory. All other fixed manufacturing overhead expenses are paid in cash in the quarter they occur. The fixed manufacturing overhead rate will be computed by dividing the year's total fixed manufacturing overhead by the year's budgeted direct labor hours. Round the fixed overhead rate to the nearest penny, Variable selling and administrative expenses are estimated to be (24) $12.00 per box car sold. Fixed seling and administrative expenses are expected to total (25) $95,000 each quarter, with (26) $30,000 out of the total amount of (25) $95,000 representing depreciation on the office space, furniture and equipment. Other than depreciation, all selling and administrative expenses are paid for in the quarter they I occur. On (36) June 30, 2021 the Large Box Car Division plans to buy new machinery and equipment for (27) $1,000,000. The new machinery and equipment will be acquired at the very end of the fiscal year, so it will not be used in production and sales during the coming year and it will not be depreciated until the following year. The Large Box Car Division expects to pay (28) 30% down in cash and finance the remaining (29) 70% of the equipment cost with a note payable from a local bank with whom they do business with. No interest payable will accrue on the equipment note payable until after (33) June 30, 2021. The Division must maintain a minimum cash balance of (30) $100,000. If after accounting for cash receipts and disbursements (including dividends) in the cash budget, the budgeted cash available cash falls below (30) $100,000 in any quarter, the Division will need to borrow cash. They have arranged a line of credit allowing it to borrow in $10,000 increments (t.e. they can borrow $10,000 or $20,000 etc. but not an odd amount). Assume borrowing will take place at the beginning of any quarter in which the available cash would otherwise be below (30) $100,000 so that at no time during the quarter will the cash balance fall below (30) $100,000 (after payment of interest). If there is extra cash at the end of the quarter and there is borrowing outstanding, the division should pay down principal (also in increments of $10,000). The bank charges the Division interest at the rate of (31) 3% per quarter. Interest accrued in the quarter will be paid the first day of the next quarter (e.g. Qi's interest is not paid in cash until Q2 and Q2's Interest will be paid in Q3). As a fully owned subsidiary, the Large Box Car Division does not pay income taxes. All income taxes are charged to Tommy's Box Car's, the parent company. Large Box Car Division will pay dividends of (32) $75,000 each quarter to its corporate parent, Tommy's Box Car's. The dividends must be paid, even if the Large Box Car Division has to borrow on its line of credit to make the payment The budgeted balance sheet for the Large Box Car Division on (34) June 30, 2020 (which is the same as the budgeted balance sheet at the beginning of business (35) July 1, 2020) is presented below. Tommy's Box Cars owns 100% of the Capital Stock of the Large Box Car Division. LARGE BOX CAR DIVISION - TOMMY'S BOX CARS BUDGETED BALANCE SHEET (34) JUNE 30, 2020 ASSETS Cash Accounts Receivable Raw Material Inventory (14) Plant and Equipment $1,850,000 2,900,000 200,000 9,600,000 LIABILITIES & EQUITY Accounts Payable $850,000 Notes Payable 0 Capital Stock 3,500,000 Retained Earnings 10,200,000 I TOTAL ASSETS $14,550,000 TOTAL LIAB. & SE $14,550,000 3 Sales Budget (July 1, 2020 - June 30, 2021) Q1 Q2 Q3 04 Year Total Item Units Sold Selling Price Per Unit Total Budgeted Sales Revenues Schedule of Expected Cash Collections 02 Q1 03 04 Year Total Item Accts Rec Balance Forward First quarter sales 1 Second quarter sales 2 Third quarter sales 73 Fourth quarter sales 14 Total Cash Collections 15 16 17 Item 18 Budgeted Sales in Units 19 Add: Desired Ending Invtory 20 = Total Needed 21 Less: Beginning Inventory 22 = Units to be Produced 23 24 25 Item Production Budget Q1 Q2 Q3 04 Year Total Direct Materials Budget Q1 Q2 Q3 04 Year Total 04 Year Total 04 Year Total 3 4 Direct Materials Budget 5 Item 01 Q2 03 6 Total Production of Box Cars 7 Wood Feet per Car 8 Total Wood Required (feet) 99 Add: Desired Ending Wood (feet) 30 Total Needs (feet) 31 Less: Beginning Inventory 32 Total DM to be purchased (feet) 33 Cost per foot 34 Total cost of direct materials purchases 35 36 Schedule of Expected Cash Disbursements for Purchases of Materials 37 Item Q1 Q2 03 38 Accts Payable Balance Forward 39 First quarter Purchases 40 Second quarter Purchases 41 Third quarter Purchases 42 Fourth quarter Purchases 43 Total Cash Payments 44 45 Direct Labor Budget 45 Item Q1 Q2 Q3 47 Total Production in Units 48 X Direct Labor Hours per Unit 49 = Total Direct Labor Hous Required 50 X Labor Wage Rate 51 = Total Direct Labor Costs 52 53 Manufacturing Overhead Budget (MOH) 54 Item 01 02 Q3 55 Variable MFG Overhead: 56 Total direct labor hours 57 x Variable overhead rate per DL Hour 58 = Total Variable MFG Overhead 59 Total Fixed Manufacturing Overhead 60 Total Manufacturing Overhead 61 Less: Depreciation (non cash expense) 62 Cash Disbursements for MEG Overhead 63 64 65 Pre-Determined Overhead Rate Calculation 04 Year Total 04 Year Total per unit 65 Pre-Determined Overhead Rate Calculation 66 Hint: Recall from Chapter 2 how you calculated your Pre-Determined Overhead Rate 67 Total Budgeting MOH 68 + "Cost Driver 69 - MOH to be Applied Per Driver Unit use to decimal places for POHR 70 71 Ending Finished Goods Inventory (at Cost) Hint: Use the information / previously calculated above li.e. your PDOH) to determine the product cost of one unit. 72 Once completed, multiple the unit cost by the number of units in ending inventory 73 Ending Finished Goods Inventory Budget Quantity Cost (rate) Total Cost 74 Production per Box Car per boxear per unit 75 Direct materials X 76 Direct labor X 77 Manufacturing overhead X 78 Production Cost per Box Car 79 Ending finished goods inventory: Box Cars 80 Ending finished goods inventory in dollars 81 82 Selling and Admin Budget (S & A) 83 Item Q1 Q2 Q3 04 Year Total 84 Variable Sales & Admin Expenses: 85 Sales in Units 86 X Variable Sales & Admin Rate per unit 87 = Variable Sales & Admin Expense 88 + Total Fixed Sales & Admin Expense 89 - Total Sales & Admin Expenses 90 Less: Depreciation (non-cash expense) 91 =Cash Disbisbursements for S & A Exp's 92 93 Cash Budget 94 Item 21 Q2 Q3 Q4 Year Total 95 Beginning Cash Balance 96 Add: Cash Collections 97 -Total Cash Available 98 Less: Cash Disbursements 99 Direct Materials 100 Direct Labor 701 Manufacturing Overhead 102 Selling & Administrative 103 Equipment Purchases 104 Dividends 105 Total Disbursements Excess (Deficiency of cash available over 106 disbursements 107 Cash Budget (Financing & Repayment) 103 Item 21 Q2 @3 04 Year Total Excess (deficiency) of cash available over 110 disbursements 111 - Interest Payments 108 E 109 04 Year Total 115 124 D 108 Cash Budget (Financing & Repayment) Item Q1 Q2 Q3 Excess (deficiency) of cash available over 110 disbursements 111 - Interest Payments 112 Borrowing (at Beginning of QUARTER) 113 - Repayments (at the End of QUARTER) 114 + Equip loan (at the end of the year) - Total Financing 116 Ending Cash Balance 117 118 Loan Balance for Interest Caloulation 119 120 121 122 123 Tommy's Bow Cars - Large 125 Pro Forma Income Statement 126 For the Fiscal Year Ended June 30, 2021 127 Item Amount 128 Sales 129 Cort of goods sold 130 Gross margin 131 Seling & administrative expenses 132 Net operating income 133 Interest expense 134 Net income 135 136 Tommy's Box Cars - Large 137 Pro Forma Balance Sheet 138 As of June 30, 2021 ANO June 30, 2020 139 Assets June 30, 2021 June 30, 2020 140 Cash 1850.000 141 Accounts receivable $ 2,900.000 142 Dreot materials inventory $ 200,000 143 Finished Goods inventory Ibon cars 0 144 Piant and equipment 9 600 000 145 Total assets 314,550,000 146 Liabilities and Stockholders' Equity June 30, 2021 June 30, 2020 147 Accounts payable + 850,000 148 Notes payable - equipment $ 149 Letter of Credit outstanding $ 150 Capital stock + 3.500.000 151 Retained Earnings 10.200.000 152 Total liabilities and stockholders equity 314,550,000 153 Our controller, Tommy Swain is negotiating with potential new Wood suppliers in Kentucky. We need the Large Box Car Division's Master Budget for the fiscal year ended (36) June 30, 2021 for our corporate strategic planning process, and we cannot wait for Tommy's return from Kentucky. We would like you to prepare the Large Box Car Division's Master Budget for the fiscal year ended June 30, 2021. The deliverables are as follows: 1. Sales budget, including a schedule of expected cash collections. 2. Production budget. 3. Direct materials budget, including a schedule of expected cash disbursements for materials. 4. Direct labor budget. 5. Manufacturing overhead budget. 6. Ending finished goods inventory budget calculating the expected value of the finished goods inventory as of (36) June 30, 2021. * 7. Selling and administrative expense budget. 8. Cash budget. 9. Budgeted Income statement for the year ended (36) June 30, 2021. * 10. Budgeted balance sheet for (36) June 30, 2021. * All the Master Budget schedules except those marked with an asterisk for the Large Box Car Division should include a column for each quarter and a total column for the fiscal year. We only need annual totals for the budgeted financial statements (schedules 9 and 10) and we only need a year-end total for the value of finished goods inventory (schedule 6). The hard copies of these budget schedules should be delivered by the company deadline. You can print more than one schedule per page, but do not have a page break in the middle of a budget schedule. I like to be able to view an entire budget schedule without flipping back and forth between pages. Please also use a type font of between 10-12 points for printing. We also need you to submit (via e-mail) the Excel spreadsheet that you used to create the budget schedules you print so we can use the spreadsheet as a starting point for future budgets. Upload the Excel spreadsheet on Blackboard. We need that spreadsheet file the night before the meeting. I've attached a brief description of the Large Box Car Division to the budget data Tommy gave me before he left for Kentucky. We eagerly await your results. Sincerely, Tommy's Box Cars During 2019-20 fiscal year, the average selling price for large box cars is expected to be (1) $115 per car. The Large Box Car Division forecasts the following units of sales. Fourth Quarter Box Car UNIT Sales (2-5) First 65,000 Second 70,000 Third 60,000 65,000 O The collection pattern for Accounts Receivable is as follows: o (6) 50 percent of all sales are collected within the quarter in which they are sold o (7) 50 percent of all sales are collected in the following quarter. There are no bad debts/uncollectible accounts. Due to high demand last year, the Large Box Car Division expects to have (8) zero finished box cars in inventory on (35) July 1, 2020, the beginning of the first quarter of the new fiscal year (i.e. Beginning Finished Goods Inventory is (8) Zero). To avoid having that problem in the coming fiscal year, the Large Box Car Division would like to have the ending inventory of Box Car at the end of each of the first three quarters equal to (9) 30% of the budgeted sales for the next quarter. They would like to have (10) 10,000 finished Box Cars on hand on (36) June 30, 2021. First Second Third Fourth Quarter Ending FG inventory of Box Cars as a % of the next quarter's budgeted sales (9) Ending FG inventory of Box Cars (10) 30% 30% 30% 2 ? 2 ? 10,000 Each large box car requires an average of (11) 5.0 feet of wood. The Large Box Car Division buys wood for (13) $4.00 per foot and they expect the price to remain constant throughout the year. They expect to have (12) 50,000 feet of wood (RAW MATERIALS) on hand as of July 1, 2019((12) 50,000 * ((13) $4.00 = (14) $200,000 - This is beginning Direct Material Inventory), the beginning of the first quarter of the fiscal year. At the end of each of the first three quarters, the Large Box Car Division would like to have their direct materials inventory quantity to equal (15) 25 percent of the amount required for the following quarter's planned production. On (36) June 30, 2021, the end of the fiscal year, Large Box Car Division would like to have (16) 60,000 feet of wood on hand (This is ending Direct Material Inventory).. Third 25% ? ? ? Quarter First Second Fourth Ending DM inventory as a % of the next quarter's production 25% 25% requirement (15) Ending DM inventory in feet (16) ? 60,000 The Large Box Car Division buys its wood on account. It pays for (17) 30% of its purchases of direct materials in the quarter in which they were purchased and (18) 70% in the quarter after they were purchased. Each large box car requires (19) 5 hours of direct labor. Employees engaged in direct labor will be paid an estimated (20) $11.00 per labor hour. Wages and salaries are paid on the 15 and 30th of each month. Variable manufacturing overhead is estimated to be (21) $3.75 per direct labor hour for the coming fiscal year. All variable manufacturing overhead expenses are paid for in the quarter incurred. 2 Tommy's Box Cars Fixed manufacturing overhead is estimated to total (22) $120,000 each quarter, with (23) $40,000 out of the total amount of (22) $120,000 representing depreciation on machinery, equipment and the factory. All other fixed manufacturing overhead expenses are paid in cash in the quarter they occur. The fixed manufacturing overhead rate will be computed by dividing the year's total fixed manufacturing overhead by the year's budgeted direct labor hours. Round the fixed overhead rate to the nearest penny, Variable selling and administrative expenses are estimated to be (24) $12.00 per box car sold. Fixed seling and administrative expenses are expected to total (25) $95,000 each quarter, with (26) $30,000 out of the total amount of (25) $95,000 representing depreciation on the office space, furniture and equipment. Other than depreciation, all selling and administrative expenses are paid for in the quarter they I occur. On (36) June 30, 2021 the Large Box Car Division plans to buy new machinery and equipment for (27) $1,000,000. The new machinery and equipment will be acquired at the very end of the fiscal year, so it will not be used in production and sales during the coming year and it will not be depreciated until the following year. The Large Box Car Division expects to pay (28) 30% down in cash and finance the remaining (29) 70% of the equipment cost with a note payable from a local bank with whom they do business with. No interest payable will accrue on the equipment note payable until after (33) June 30, 2021. The Division must maintain a minimum cash balance of (30) $100,000. If after accounting for cash receipts and disbursements (including dividends) in the cash budget, the budgeted cash available cash falls below (30) $100,000 in any quarter, the Division will need to borrow cash. They have arranged a line of credit allowing it to borrow in $10,000 increments (t.e. they can borrow $10,000 or $20,000 etc. but not an odd amount). Assume borrowing will take place at the beginning of any quarter in which the available cash would otherwise be below (30) $100,000 so that at no time during the quarter will the cash balance fall below (30) $100,000 (after payment of interest). If there is extra cash at the end of the quarter and there is borrowing outstanding, the division should pay down principal (also in increments of $10,000). The bank charges the Division interest at the rate of (31) 3% per quarter. Interest accrued in the quarter will be paid the first day of the next quarter (e.g. Qi's interest is not paid in cash until Q2 and Q2's Interest will be paid in Q3). As a fully owned subsidiary, the Large Box Car Division does not pay income taxes. All income taxes are charged to Tommy's Box Car's, the parent company. Large Box Car Division will pay dividends of (32) $75,000 each quarter to its corporate parent, Tommy's Box Car's. The dividends must be paid, even if the Large Box Car Division has to borrow on its line of credit to make the payment The budgeted balance sheet for the Large Box Car Division on (34) June 30, 2020 (which is the same as the budgeted balance sheet at the beginning of business (35) July 1, 2020) is presented below. Tommy's Box Cars owns 100% of the Capital Stock of the Large Box Car Division. LARGE BOX CAR DIVISION - TOMMY'S BOX CARS BUDGETED BALANCE SHEET (34) JUNE 30, 2020 ASSETS Cash Accounts Receivable Raw Material Inventory (14) Plant and Equipment $1,850,000 2,900,000 200,000 9,600,000 LIABILITIES & EQUITY Accounts Payable $850,000 Notes Payable 0 Capital Stock 3,500,000 Retained Earnings 10,200,000 I TOTAL ASSETS $14,550,000 TOTAL LIAB. & SE $14,550,000 3 Sales Budget (July 1, 2020 - June 30, 2021) Q1 Q2 Q3 04 Year Total Item Units Sold Selling Price Per Unit Total Budgeted Sales Revenues Schedule of Expected Cash Collections 02 Q1 03 04 Year Total Item Accts Rec Balance Forward First quarter sales 1 Second quarter sales 2 Third quarter sales 73 Fourth quarter sales 14 Total Cash Collections 15 16 17 Item 18 Budgeted Sales in Units 19 Add: Desired Ending Invtory 20 = Total Needed 21 Less: Beginning Inventory 22 = Units to be Produced 23 24 25 Item Production Budget Q1 Q2 Q3 04 Year Total Direct Materials Budget Q1 Q2 Q3 04 Year Total 04 Year Total 04 Year Total 3 4 Direct Materials Budget 5 Item 01 Q2 03 6 Total Production of Box Cars 7 Wood Feet per Car 8 Total Wood Required (feet) 99 Add: Desired Ending Wood (feet) 30 Total Needs (feet) 31 Less: Beginning Inventory 32 Total DM to be purchased (feet) 33 Cost per foot 34 Total cost of direct materials purchases 35 36 Schedule of Expected Cash Disbursements for Purchases of Materials 37 Item Q1 Q2 03 38 Accts Payable Balance Forward 39 First quarter Purchases 40 Second quarter Purchases 41 Third quarter Purchases 42 Fourth quarter Purchases 43 Total Cash Payments 44 45 Direct Labor Budget 45 Item Q1 Q2 Q3 47 Total Production in Units 48 X Direct Labor Hours per Unit 49 = Total Direct Labor Hous Required 50 X Labor Wage Rate 51 = Total Direct Labor Costs 52 53 Manufacturing Overhead Budget (MOH) 54 Item 01 02 Q3 55 Variable MFG Overhead: 56 Total direct labor hours 57 x Variable overhead rate per DL Hour 58 = Total Variable MFG Overhead 59 Total Fixed Manufacturing Overhead 60 Total Manufacturing Overhead 61 Less: Depreciation (non cash expense) 62 Cash Disbursements for MEG Overhead 63 64 65 Pre-Determined Overhead Rate Calculation 04 Year Total 04 Year Total per unit 65 Pre-Determined Overhead Rate Calculation 66 Hint: Recall from Chapter 2 how you calculated your Pre-Determined Overhead Rate 67 Total Budgeting MOH 68 + "Cost Driver 69 - MOH to be Applied Per Driver Unit use to decimal places for POHR 70 71 Ending Finished Goods Inventory (at Cost) Hint: Use the information / previously calculated above li.e. your PDOH) to determine the product cost of one unit. 72 Once completed, multiple the unit cost by the number of units in ending inventory 73 Ending Finished Goods Inventory Budget Quantity Cost (rate) Total Cost 74 Production per Box Car per boxear per unit 75 Direct materials X 76 Direct labor X 77 Manufacturing overhead X 78 Production Cost per Box Car 79 Ending finished goods inventory: Box Cars 80 Ending finished goods inventory in dollars 81 82 Selling and Admin Budget (S & A) 83 Item Q1 Q2 Q3 04 Year Total 84 Variable Sales & Admin Expenses: 85 Sales in Units 86 X Variable Sales & Admin Rate per unit 87 = Variable Sales & Admin Expense 88 + Total Fixed Sales & Admin Expense 89 - Total Sales & Admin Expenses 90 Less: Depreciation (non-cash expense) 91 =Cash Disbisbursements for S & A Exp's 92 93 Cash Budget 94 Item 21 Q2 Q3 Q4 Year Total 95 Beginning Cash Balance 96 Add: Cash Collections 97 -Total Cash Available 98 Less: Cash Disbursements 99 Direct Materials 100 Direct Labor 701 Manufacturing Overhead 102 Selling & Administrative 103 Equipment Purchases 104 Dividends 105 Total Disbursements Excess (Deficiency of cash available over 106 disbursements 107 Cash Budget (Financing & Repayment) 103 Item 21 Q2 @3 04 Year Total Excess (deficiency) of cash available over 110 disbursements 111 - Interest Payments 108 E 109 04 Year Total 115 124 D 108 Cash Budget (Financing & Repayment) Item Q1 Q2 Q3 Excess (deficiency) of cash available over 110 disbursements 111 - Interest Payments 112 Borrowing (at Beginning of QUARTER) 113 - Repayments (at the End of QUARTER) 114 + Equip loan (at the end of the year) - Total Financing 116 Ending Cash Balance 117 118 Loan Balance for Interest Caloulation 119 120 121 122 123 Tommy's Bow Cars - Large 125 Pro Forma Income Statement 126 For the Fiscal Year Ended June 30, 2021 127 Item Amount 128 Sales 129 Cort of goods sold 130 Gross margin 131 Seling & administrative expenses 132 Net operating income 133 Interest expense 134 Net income 135 136 Tommy's Box Cars - Large 137 Pro Forma Balance Sheet 138 As of June 30, 2021 ANO June 30, 2020 139 Assets June 30, 2021 June 30, 2020 140 Cash 1850.000 141 Accounts receivable $ 2,900.000 142 Dreot materials inventory $ 200,000 143 Finished Goods inventory Ibon cars 0 144 Piant and equipment 9 600 000 145 Total assets 314,550,000 146 Liabilities and Stockholders' Equity June 30, 2021 June 30, 2020 147 Accounts payable + 850,000 148 Notes payable - equipment $ 149 Letter of Credit outstanding $ 150 Capital stock + 3.500.000 151 Retained Earnings 10.200.000 152 Total liabilities and stockholders equity 314,550,000 153 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Government Auditing Standards 2011 Revision

Authors: U. S. Government Accountability Office, Comptroller General Of The United States

1st Edition

1482311372, 978-1482311372