Answered step by step

Verified Expert Solution

Question

1 Approved Answer

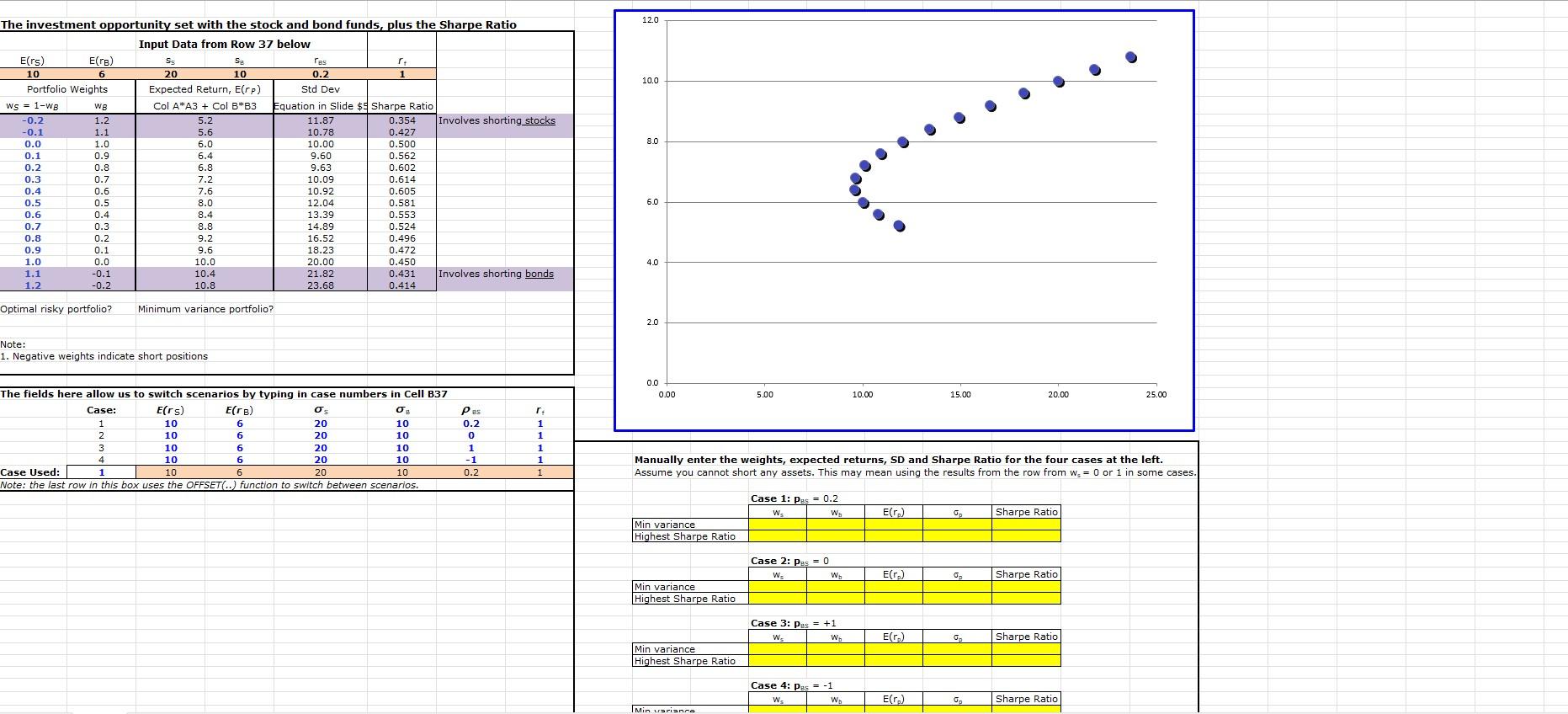

The investment opportunity set with the stock and bond funds, plus the Sharpe Ratio The fielde here allow uc tn cwitch crenarinc ho toninn in

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Data Analytics Theory And Application

Authors: Sinem Derindere Köseo?lu

1st Edition

303083798X,3030837998