the last 3 pictures are the same question

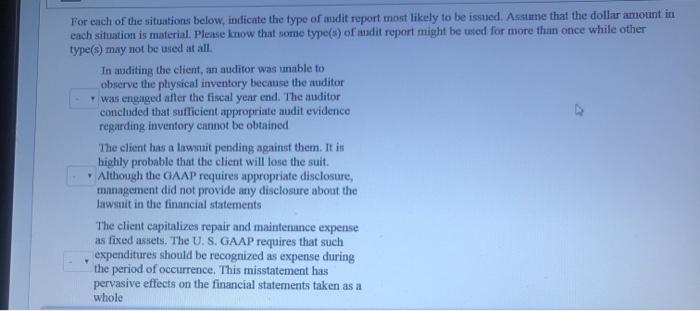

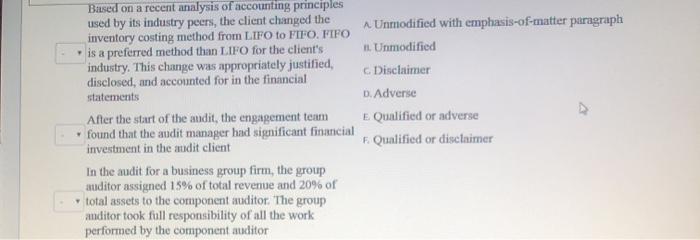

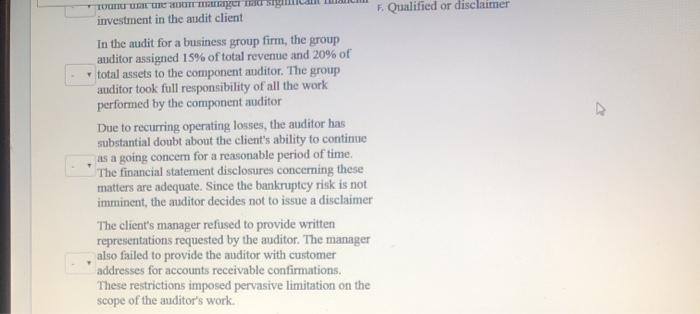

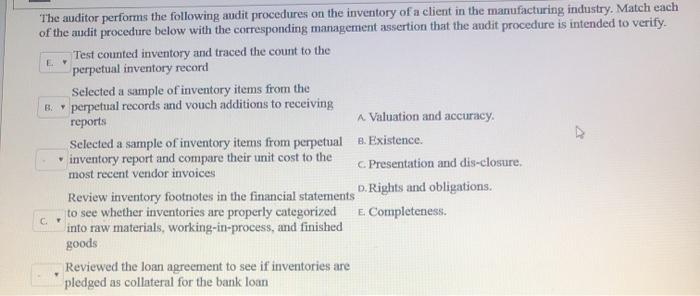

L. The auditor performs the following audit procedures on the inventory of a client in the manufacturing industry. Match each of the audit procedure below with the corresponding management assertion that the audit procedure is intended to verify. Test counted inventory and traced the count to the perpetual inventory record Selected a sample of inventory items from the B. perpetual records and vouch additions to receiving reports A. Valuation and accuracy Selected a sample of inventory items from perpetual B. Existence. inventory report and compare their unit cost to the most recent vendor invoices Presentation and dis-closure. Review inventory footnotes in the financial statements D. Rights and obligations. to see whether inventories are properly categorized E Completeness. into raw materials, working-in-process, and finished goods Reviewed the loan agreement to see if inventories are pledged as collateral for the bank loan C For each of the situation below, indicate the type of dit report most likely to be issued. Assume that the dollar amount in each situation is material. Please know that some type(s) of dit report might be used for more than once while other type(s) may not be used at all. In additing the client, an auditor was unable to observe the physical inventory becanse the auditor was engaged after the fiscal year end. The auditor concluded that sufficient appropriate audit evidence regarding inventory cannot be obtained The client has a lawsuit pending against them. It is highly probable that the client will lose the suit. Although the GAAP requires appropriate disclosure, management did not provide any disclosure about the lawsuit in the financial statements The client capitalizes repair and maintenance expense as fixed assets. The U.S. GAAP requires that such expenditures should be recognized as expense during the period of occurrence. This misstatement has pervasive effects on the financial statements taken as a whole Based on a recent analysis of accounting principles used by its industry peers, the client changed the inventory costing method from LIFO to FIFO. FIFO is a preferred method than LIFO for the client's industry. This change was appropriately justified, disclosed, and accounted for in the financial statements After the start of the audit, the engagement team found that the audit manager had significant financial investment in the audit client In the audit for a business group firm, the group auditor assigned 15% of total revenue and 20% of total assets to the component auditor. The group anditor took full responsibility of all the work performed by the component auditor A Unmodified with emphasis-of-matter paragraph n. Unmodified Disclaimer D. Adverse E Qualified or adverse F. Qualified or disclaimer TUNTURI CU WITTE investment in the audit client 5. Qualified or disclaimer In the audit for a business group firm, the group auditor assigned 15% of total revenue and 20% of total assets to the component auditor. The group auditor took full responsibility of all the work performed by the component auditor Due to recurring operating losses, the auditor has substantial doubt about the client's ability to contime as a going concern for a reasonable period of time. The financial statement disclosures concerning these matters are adequate. Since the bankruptcy risk is not imminent, the auditor decides not to issue a disclaimer The client's manager refused to provide written representations requested by the auditor. The manager also failed to provide the auditor with customer addresses for accounts receivable confirmations These restrictions imposed pervasive limitation on the scope of the auditor's work