Answered step by step

Verified Expert Solution

Question

1 Approved Answer

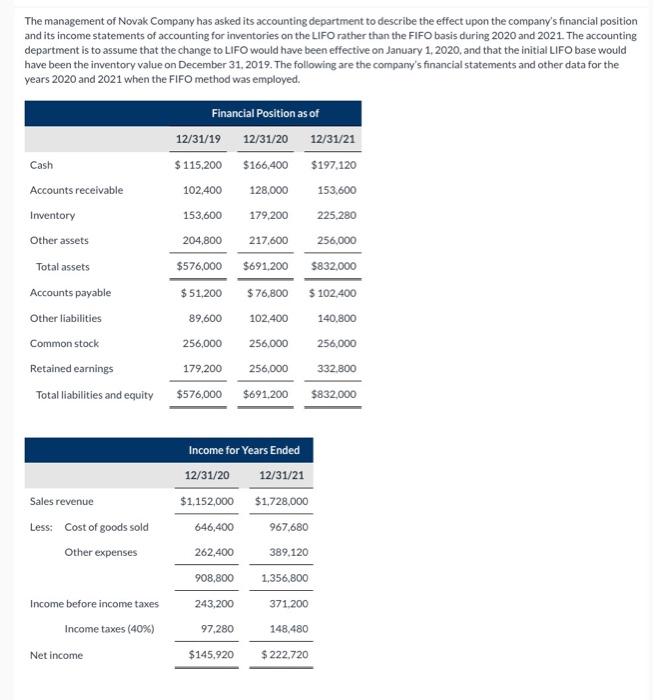

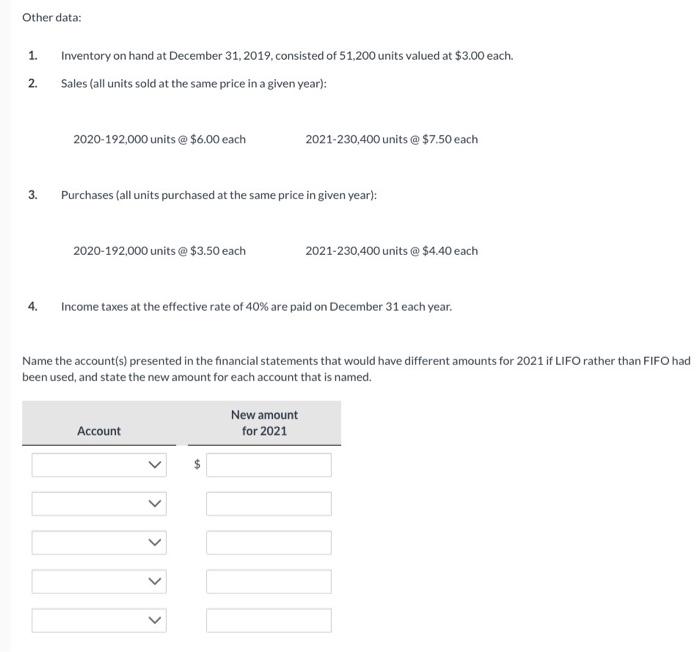

The management of Novak Company has asked its accounting department to describe the effect upon the company's financial position and its income statements of accounting

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing And Systems Exam Questions And Explanations

Authors: Irvin N. Gleim, William A. Hillison

13th Edition

1581945272, 978-1581945270