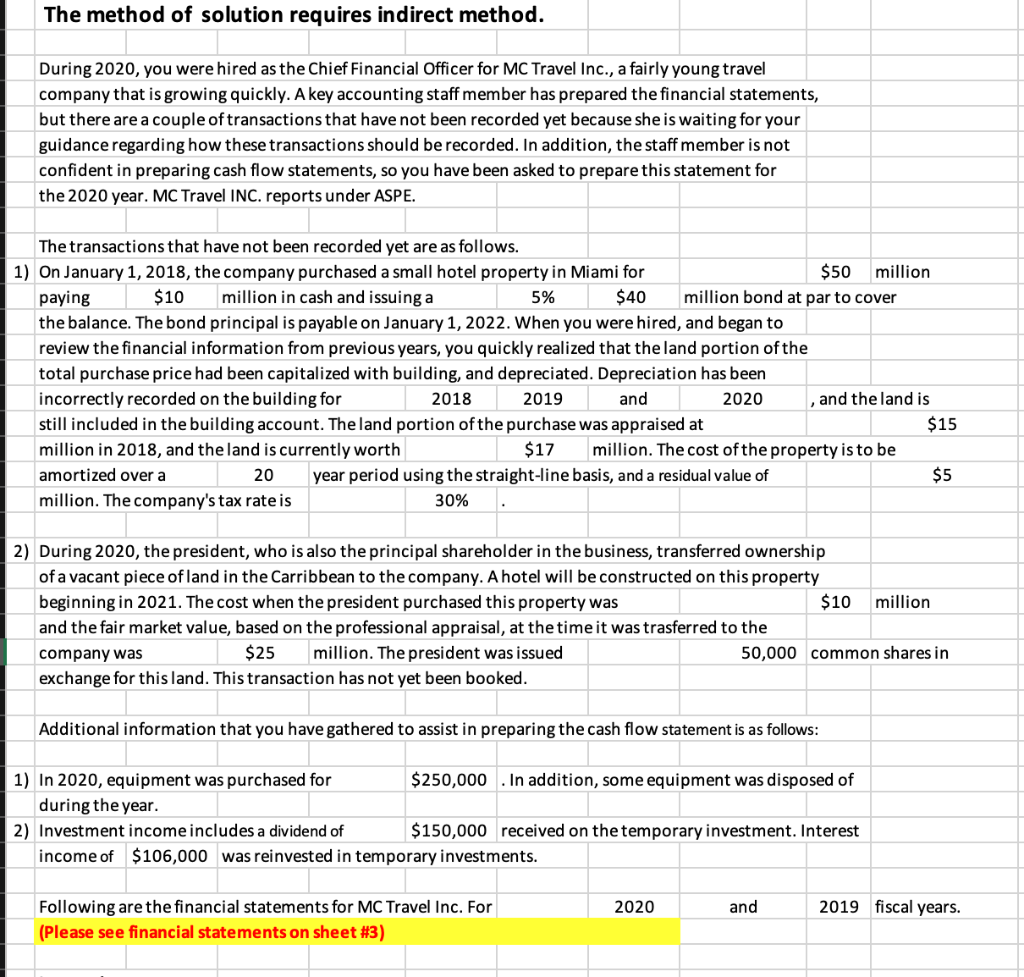

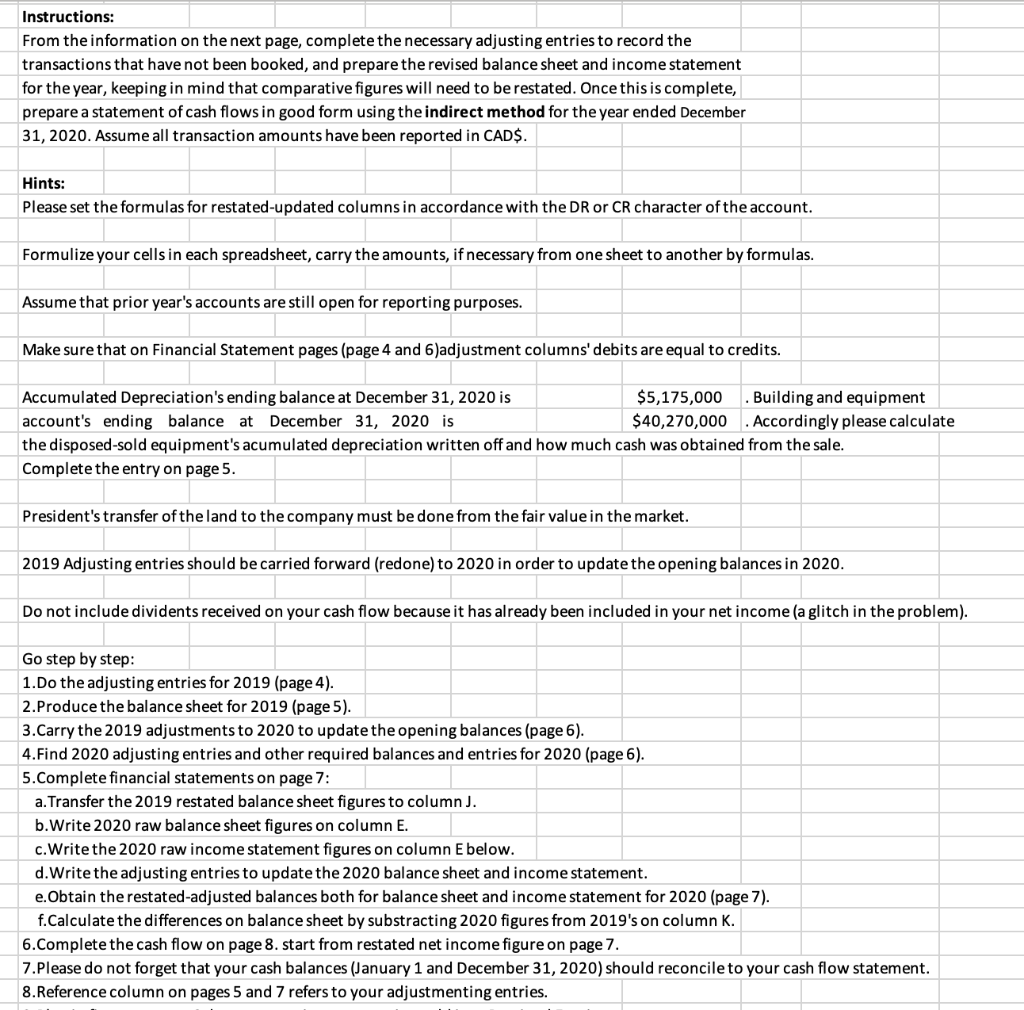

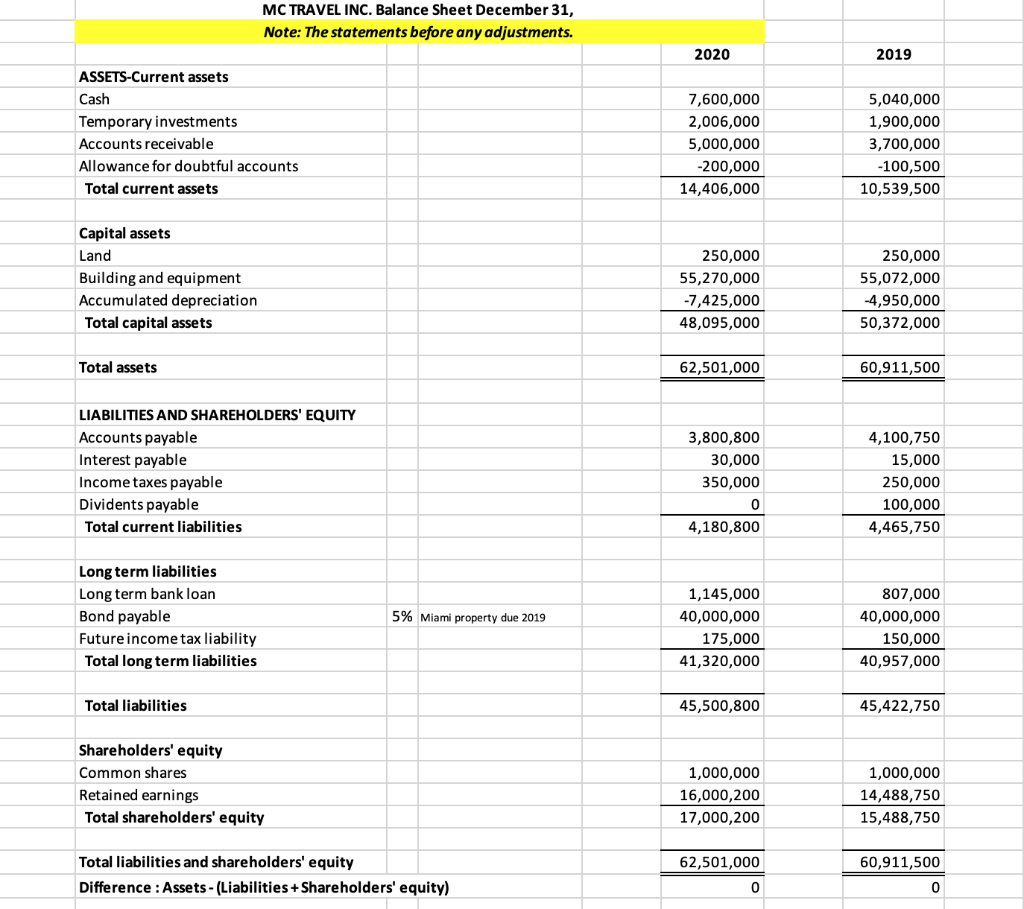

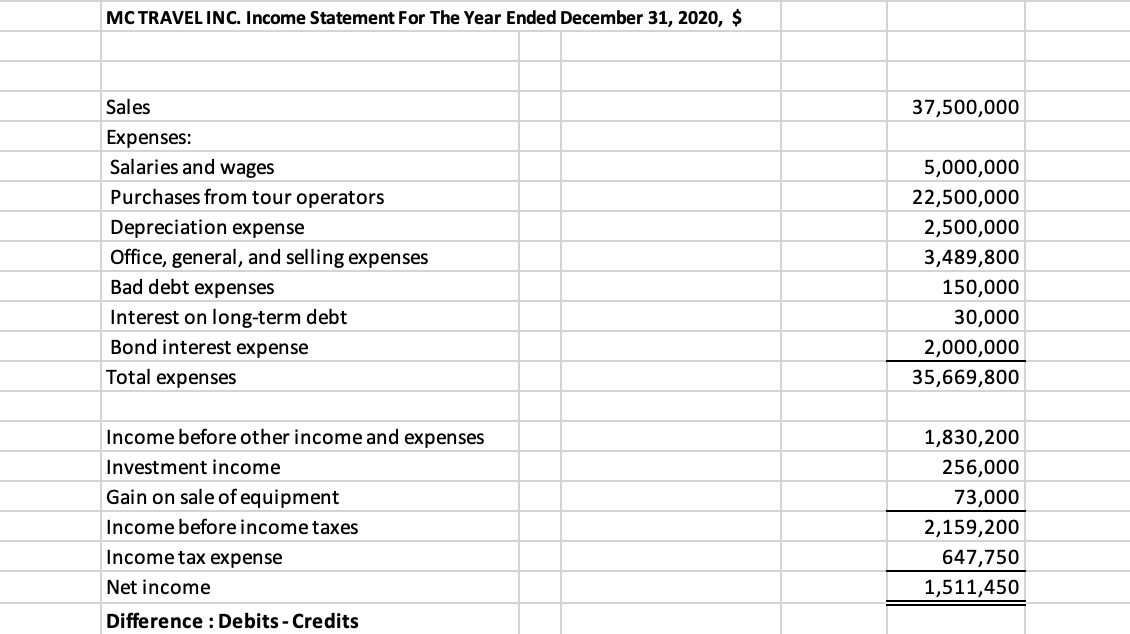

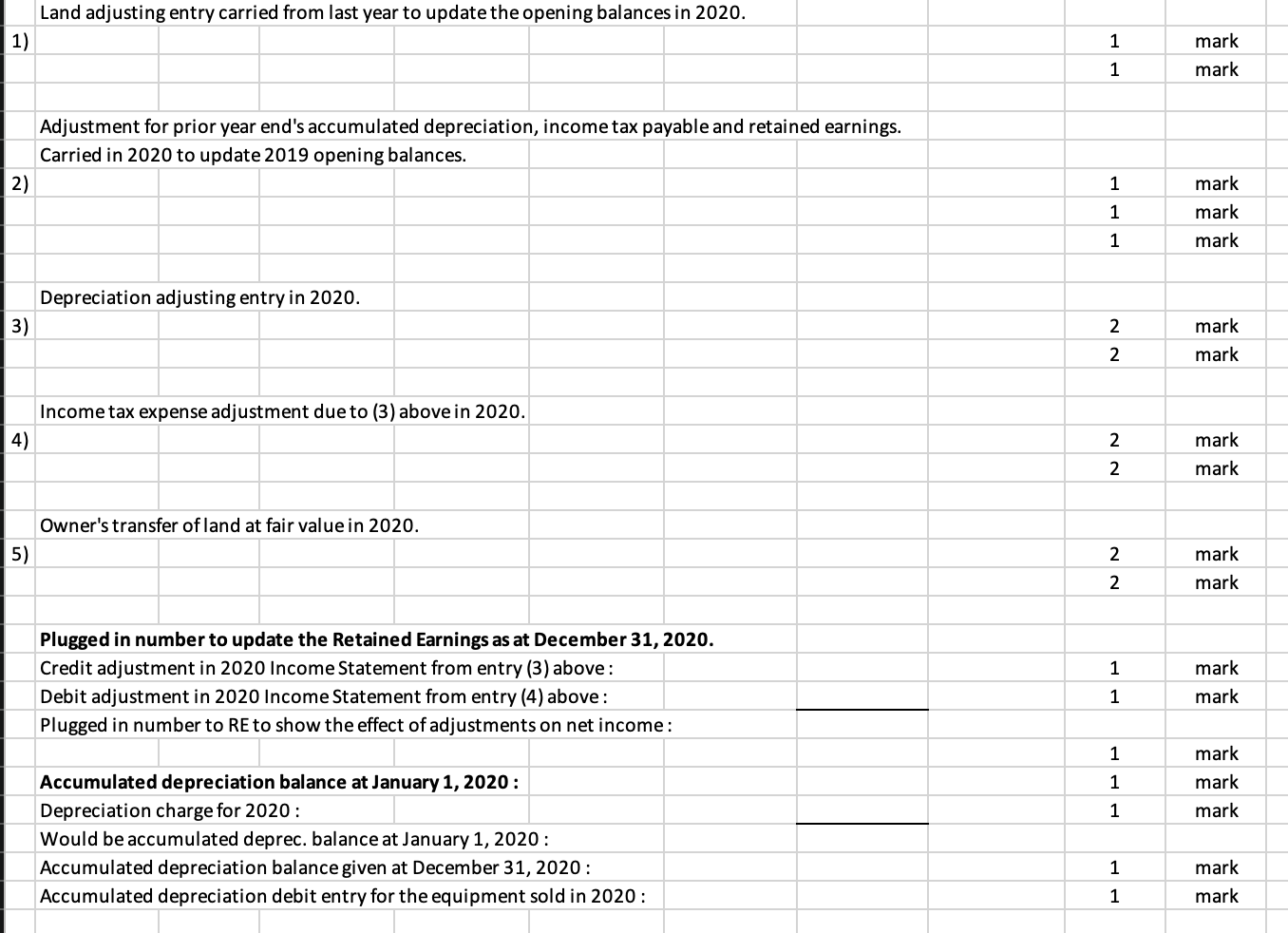

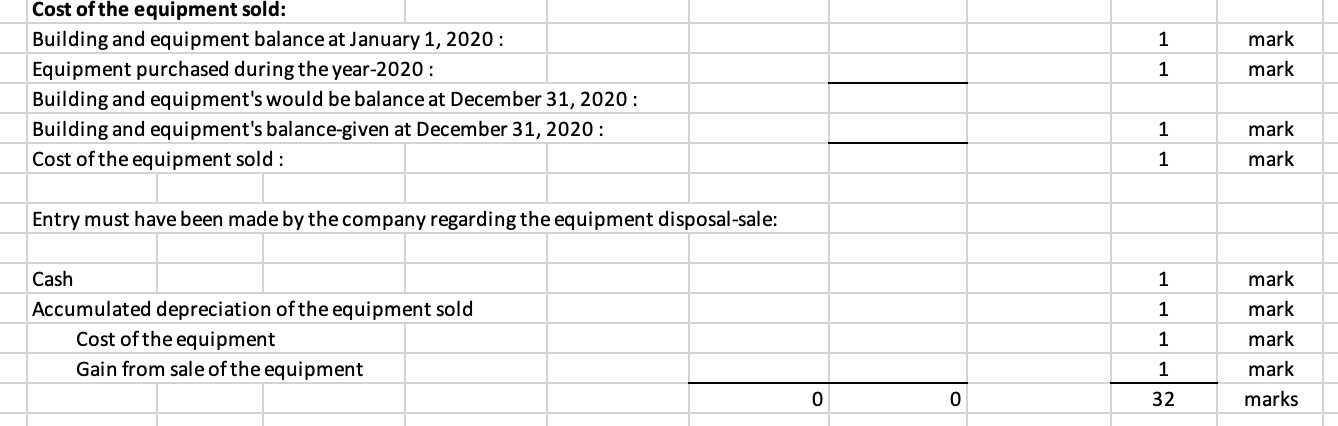

The method of solution requires indirect method. During 2020, you were hired as the Chief Financial Officer for MC Travel Inc., a fairly young travel company that is growing quickly. A key accounting staff member has prepared the financial statements, but there are a couple of transactions that have not been recorded yet because she is waiting for your guidance regarding how these transactions should be recorded. In addition, the staff member is not confident in preparing cash flow statements, so you have been asked to prepare this statement for the 2020 year. MC Travel INC. reports under ASPE. The transactions that have not been recorded yet are as follows. 1) On January 1, 2018, the company purchased a small hotel property in Miami for $50 million paying $10 million in cash and issuing a 5% $40 million bond at par to cover the balance. The bond principal is payable on January 1, 2022. When you were hired, and began to review the financial information from previous years, you quickly realized that the land portion of the total purchase price had been capitalized with building, and depreciated. Depreciation has been incorrectly recorded on the building for 2018 2019 and 2020 and the land is still included in the building account. The land portion of the purchase was appraised at $15 million in 2018, and the land is currently worth $17 million. The cost of the property is to be amortized over a 20 year period using the straight-line basis, and a residual value of $5 million. The company's tax rate is 30% 2) During 2020, the president, who is also the principal shareholder in the business, transferred ownership of a vacant piece of land in the Carribbean to the company. A hotel will be constructed on this property beginning in 2021. The cost when the president purchased this property was $10 million and the fair market value, based on the professional appraisal, at the time it was trasferred to the company was $25 million. The president was issued 50,000 common shares in exchange for this land. This transaction has not yet been booked. Additional information that you have gathered to assist in preparing the cash flow statement is as follows: 1) In 2020, equipment was purchased for $250,000 . In addition, some equipment was disposed of during the year. 2) Investment income includes a dividend of $150,000 received on the temporary investment. Interest income of $106,000 was reinvested in temporary investments. 2020 and 2019 fiscal years. Following are the financial statements for MC Travel Inc. For (Please see financial statements on sheet #3) Instructions: From the information on the next page, complete the necessary adjusting entries to record the transactions that have not been booked, and prepare the revised balance sheet and income statement for the year, keeping in mind that comparative figures will need to be restated. Once this is complete, prepare a statement of cash flows in good form using the indirect method for the year ended December 31, 2020. Assume all transaction amounts have been reported in CAD$. Hints: Please set the formulas for restated-updated columns in accordance with the DR or CR character of the account. Formulize your cells in each spreadsheet, carry the amounts, if necessary from one sheet to another by formulas. Assume that prior year's accounts are still open for reporting purposes. Make sure that on Financial Statement pages (page 4 and 6)adjustment columns' debits are equal to credits. Accumulated Depreciation's ending balance at December 31, 2020 is $5,175,000 Building and equipment account's ending balance at December 31, 2020 is $40,270,000 Accordingly please calculate the disposed-sold equipment's acumulated depreciation written off and how much cash was obtained from the sale. Complete the entry on page 5. President's transfer of the land to the company must be done from the fair value in the market. 2019 Adjusting entries should be carried forward (redone) to 2020 in order to update the opening balances in 2020. Do not include dividents received on your cash flow because it has already been included in your net income (a glitch in the problem). Go step by step: 1.Do the adjusting entries for 2019 (page 4). 2.Produce the balance sheet for 2019 (page 5). 3.Carry the 2019 adjustments to 2020 to update the opening balances (page 6). 4.Find 2020 adjusting entries and other required balances and entries for 2020 (page 6). 5.Complete financial statements on page 7: a. Transfer the 2019 restated balance sheet figures to column). b.Write 2020 raw balance sheet figures on column E. c. Write the 2020 raw income statement figures on column E below. d.Write the adjusting entries to update the 2020 balance sheet and income statement. e.Obtain the restated-adjusted balances both for balance sheet and income statement for 2020 (page 7). f.Calculate the differences on balance sheet by substracting 2020 figures from 2019's on column K. 6.Complete the cash flow on page 8. start from restated net income figure on page 7. 7.Please do not forget that your cash balances (January 1 and December 31, 2020) should reconcile to your cash flow statement. 8.Reference column on pages 5 and 7 refers to your adjustmenting entries. MC TRAVEL INC. Balance Sheet December 31, Note: The statements before any adjustments. 2020 2019 ASSETS-Current assets Cash Temporary investments Accounts receivable Allowance for doubtful accounts Total current assets 7,600,000 2,006,000 5,000,000 -200,000 14,406,000 5,040,000 1,900,000 3,700,000 -100,500 10,539,500 Capital assets Land Building and equipment Accumulated depreciation Total capital assets 250,000 55,270,000 -7,425,000 48,095,000 250,000 55,072,000 -4,950,000 50,372,000 Total assets 62,501,000 60,911,500 LIABILITIES AND SHAREHOLDERS' EQUITY Accounts payable Interest payable Income taxes payable Dividents payable Total current liabilities 3,800,800 30,000 350,000 0 4,180,800 4,100,750 15,000 250,000 100,000 4,465,750 Long term liabilities Long term bank loan Bond payable Future income tax liability Total long term liabilities 5% Miami property due 2019 1,145,000 40,000,000 175,000 41,320,000 807,000 40,000,000 150,000 40,957,000 Total liabilities 45,500,800 45,422,750 Shareholders' equity Common shares Retained earnings Total shareholders' equity 1,000,000 16,000,200 17,000,200 1,000,000 14,488,750 15,488,750 Total liabilities and shareholders' equity Difference : Assets - (Liabilities + Shareholders' equity) 62,501,000 0 60,911,500 0 MC TRAVEL INC. Income Statement For The Year Ended December 31, 2020, $ 37,500,000 Sales Expenses: Salaries and wages Purchases from tour operators Depreciation expense Office, general, and selling expenses Bad debt expenses Interest on long-term debt Bond interest expense Total expenses 5,000,000 22,500,000 2,500,000 3,489,800 150,000 30,000 2,000,000 35,669,800 Income before other income and expenses Investment income Gain on sale of equipment Income before income taxes Income tax expense Net income Difference : Debits - Credits 1,830,200 256,000 73,000 2,159,200 647,750 1,511,450 Land adjusting entry carried from last year to update the opening balances in 2020. 1) 1 mark 1 mark Adjustment for prior year end's accumulated depreciation, income tax payable and retained earnings. Carried in 2020 to update 2019 opening balances. 2) 1 1 mark mark mark 1 Depreciation adjusting entry in 2020. 3) 2 mark mark 2. Income tax expense adjustment due to (3) above in 2020. 4) 2 mar! mark 2 Owner's transfer of land at fair value in 2020. 5) 2 mark mark 2 1 Plugged in number to update the retained Earnings as at December 31, 2020. Credit adjustment in 2020 Income Statement from entry (3) above: Debit adjustment in 2020 Income Statement from entry (4) above: Plugged in number to RE to show the effect of adjustments on net income: mark mark 1 1 1 mark mark mark 1 Accumulated depreciation balance at January 1, 2020: Depreciation charge for 2020: Would be accumulated deprec. balance at January 1, 2020: Accumulated depreciation balance given at December 31, 2020: Accumulated depreciation debit entry for the equipment sold in 2020: 1 mark mark 1 1 mark mark 1 Cost of the equipment sold: Building and equipment balance at January 1, 2020: Equipment purchased during the year-2020: Building and equipment's would be balance at December 31, 2020: Building and equipment's balance-given at December 31, 2020: Cost of the equipment sold: 1 mark mark 1 Entry must have been made by the company regarding the equipment disposal-sale: 1 1 Cash Accumulated depreciation of the equipment sold Cost of the equipment Gain from sale of the equipment 1 mark mark mark mark marks 1 0 0 32 The method of solution requires indirect method. During 2020, you were hired as the Chief Financial Officer for MC Travel Inc., a fairly young travel company that is growing quickly. A key accounting staff member has prepared the financial statements, but there are a couple of transactions that have not been recorded yet because she is waiting for your guidance regarding how these transactions should be recorded. In addition, the staff member is not confident in preparing cash flow statements, so you have been asked to prepare this statement for the 2020 year. MC Travel INC. reports under ASPE. The transactions that have not been recorded yet are as follows. 1) On January 1, 2018, the company purchased a small hotel property in Miami for $50 million paying $10 million in cash and issuing a 5% $40 million bond at par to cover the balance. The bond principal is payable on January 1, 2022. When you were hired, and began to review the financial information from previous years, you quickly realized that the land portion of the total purchase price had been capitalized with building, and depreciated. Depreciation has been incorrectly recorded on the building for 2018 2019 and 2020 and the land is still included in the building account. The land portion of the purchase was appraised at $15 million in 2018, and the land is currently worth $17 million. The cost of the property is to be amortized over a 20 year period using the straight-line basis, and a residual value of $5 million. The company's tax rate is 30% 2) During 2020, the president, who is also the principal shareholder in the business, transferred ownership of a vacant piece of land in the Carribbean to the company. A hotel will be constructed on this property beginning in 2021. The cost when the president purchased this property was $10 million and the fair market value, based on the professional appraisal, at the time it was trasferred to the company was $25 million. The president was issued 50,000 common shares in exchange for this land. This transaction has not yet been booked. Additional information that you have gathered to assist in preparing the cash flow statement is as follows: 1) In 2020, equipment was purchased for $250,000 . In addition, some equipment was disposed of during the year. 2) Investment income includes a dividend of $150,000 received on the temporary investment. Interest income of $106,000 was reinvested in temporary investments. 2020 and 2019 fiscal years. Following are the financial statements for MC Travel Inc. For (Please see financial statements on sheet #3) Instructions: From the information on the next page, complete the necessary adjusting entries to record the transactions that have not been booked, and prepare the revised balance sheet and income statement for the year, keeping in mind that comparative figures will need to be restated. Once this is complete, prepare a statement of cash flows in good form using the indirect method for the year ended December 31, 2020. Assume all transaction amounts have been reported in CAD$. Hints: Please set the formulas for restated-updated columns in accordance with the DR or CR character of the account. Formulize your cells in each spreadsheet, carry the amounts, if necessary from one sheet to another by formulas. Assume that prior year's accounts are still open for reporting purposes. Make sure that on Financial Statement pages (page 4 and 6)adjustment columns' debits are equal to credits. Accumulated Depreciation's ending balance at December 31, 2020 is $5,175,000 Building and equipment account's ending balance at December 31, 2020 is $40,270,000 Accordingly please calculate the disposed-sold equipment's acumulated depreciation written off and how much cash was obtained from the sale. Complete the entry on page 5. President's transfer of the land to the company must be done from the fair value in the market. 2019 Adjusting entries should be carried forward (redone) to 2020 in order to update the opening balances in 2020. Do not include dividents received on your cash flow because it has already been included in your net income (a glitch in the problem). Go step by step: 1.Do the adjusting entries for 2019 (page 4). 2.Produce the balance sheet for 2019 (page 5). 3.Carry the 2019 adjustments to 2020 to update the opening balances (page 6). 4.Find 2020 adjusting entries and other required balances and entries for 2020 (page 6). 5.Complete financial statements on page 7: a. Transfer the 2019 restated balance sheet figures to column). b.Write 2020 raw balance sheet figures on column E. c. Write the 2020 raw income statement figures on column E below. d.Write the adjusting entries to update the 2020 balance sheet and income statement. e.Obtain the restated-adjusted balances both for balance sheet and income statement for 2020 (page 7). f.Calculate the differences on balance sheet by substracting 2020 figures from 2019's on column K. 6.Complete the cash flow on page 8. start from restated net income figure on page 7. 7.Please do not forget that your cash balances (January 1 and December 31, 2020) should reconcile to your cash flow statement. 8.Reference column on pages 5 and 7 refers to your adjustmenting entries. MC TRAVEL INC. Balance Sheet December 31, Note: The statements before any adjustments. 2020 2019 ASSETS-Current assets Cash Temporary investments Accounts receivable Allowance for doubtful accounts Total current assets 7,600,000 2,006,000 5,000,000 -200,000 14,406,000 5,040,000 1,900,000 3,700,000 -100,500 10,539,500 Capital assets Land Building and equipment Accumulated depreciation Total capital assets 250,000 55,270,000 -7,425,000 48,095,000 250,000 55,072,000 -4,950,000 50,372,000 Total assets 62,501,000 60,911,500 LIABILITIES AND SHAREHOLDERS' EQUITY Accounts payable Interest payable Income taxes payable Dividents payable Total current liabilities 3,800,800 30,000 350,000 0 4,180,800 4,100,750 15,000 250,000 100,000 4,465,750 Long term liabilities Long term bank loan Bond payable Future income tax liability Total long term liabilities 5% Miami property due 2019 1,145,000 40,000,000 175,000 41,320,000 807,000 40,000,000 150,000 40,957,000 Total liabilities 45,500,800 45,422,750 Shareholders' equity Common shares Retained earnings Total shareholders' equity 1,000,000 16,000,200 17,000,200 1,000,000 14,488,750 15,488,750 Total liabilities and shareholders' equity Difference : Assets - (Liabilities + Shareholders' equity) 62,501,000 0 60,911,500 0 MC TRAVEL INC. Income Statement For The Year Ended December 31, 2020, $ 37,500,000 Sales Expenses: Salaries and wages Purchases from tour operators Depreciation expense Office, general, and selling expenses Bad debt expenses Interest on long-term debt Bond interest expense Total expenses 5,000,000 22,500,000 2,500,000 3,489,800 150,000 30,000 2,000,000 35,669,800 Income before other income and expenses Investment income Gain on sale of equipment Income before income taxes Income tax expense Net income Difference : Debits - Credits 1,830,200 256,000 73,000 2,159,200 647,750 1,511,450 Land adjusting entry carried from last year to update the opening balances in 2020. 1) 1 mark 1 mark Adjustment for prior year end's accumulated depreciation, income tax payable and retained earnings. Carried in 2020 to update 2019 opening balances. 2) 1 1 mark mark mark 1 Depreciation adjusting entry in 2020. 3) 2 mark mark 2. Income tax expense adjustment due to (3) above in 2020. 4) 2 mar! mark 2 Owner's transfer of land at fair value in 2020. 5) 2 mark mark 2 1 Plugged in number to update the retained Earnings as at December 31, 2020. Credit adjustment in 2020 Income Statement from entry (3) above: Debit adjustment in 2020 Income Statement from entry (4) above: Plugged in number to RE to show the effect of adjustments on net income: mark mark 1 1 1 mark mark mark 1 Accumulated depreciation balance at January 1, 2020: Depreciation charge for 2020: Would be accumulated deprec. balance at January 1, 2020: Accumulated depreciation balance given at December 31, 2020: Accumulated depreciation debit entry for the equipment sold in 2020: 1 mark mark 1 1 mark mark 1 Cost of the equipment sold: Building and equipment balance at January 1, 2020: Equipment purchased during the year-2020: Building and equipment's would be balance at December 31, 2020: Building and equipment's balance-given at December 31, 2020: Cost of the equipment sold: 1 mark mark 1 Entry must have been made by the company regarding the equipment disposal-sale: 1 1 Cash Accumulated depreciation of the equipment sold Cost of the equipment Gain from sale of the equipment 1 mark mark mark mark marks 1 0 0 32