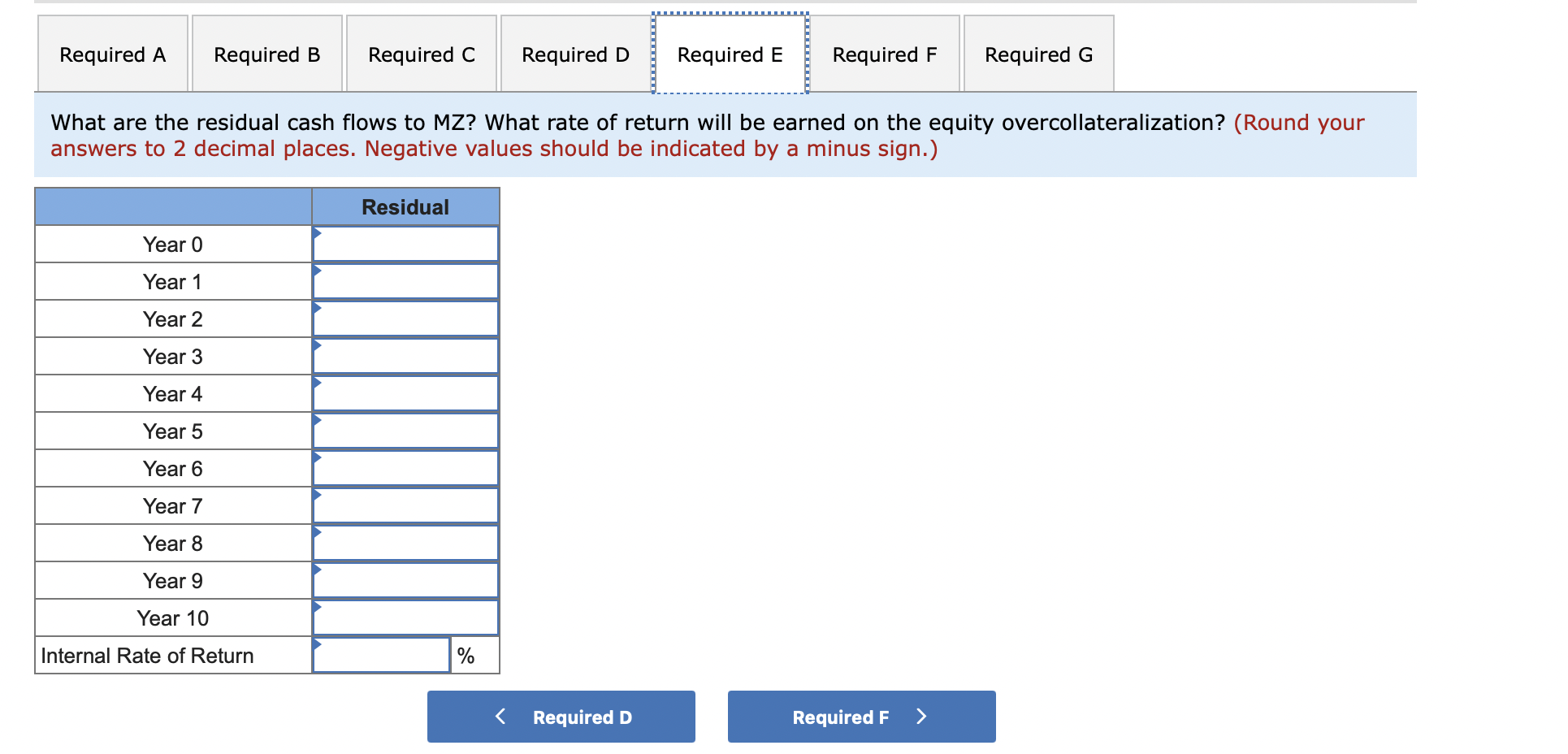

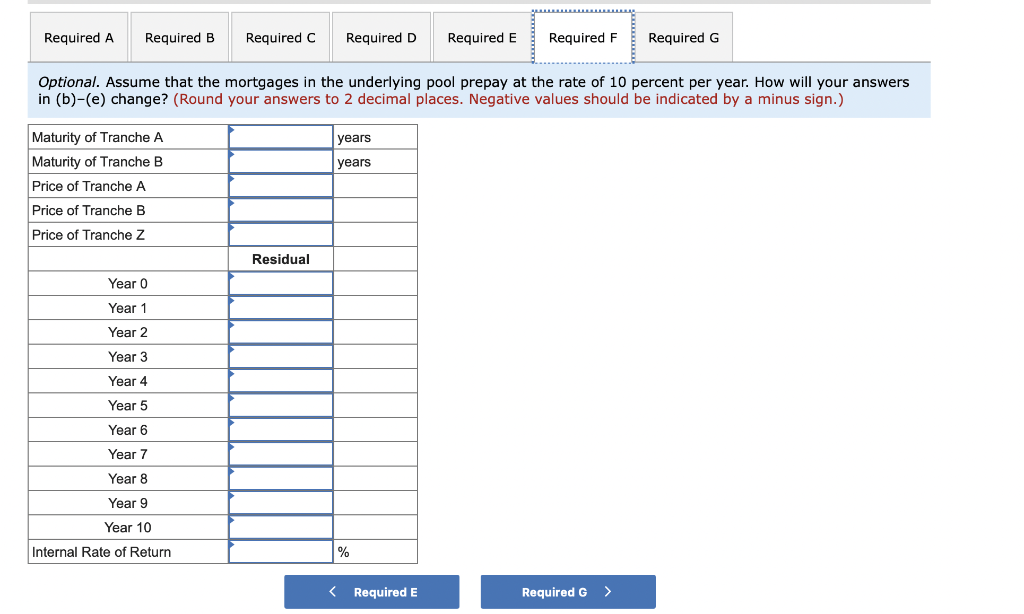

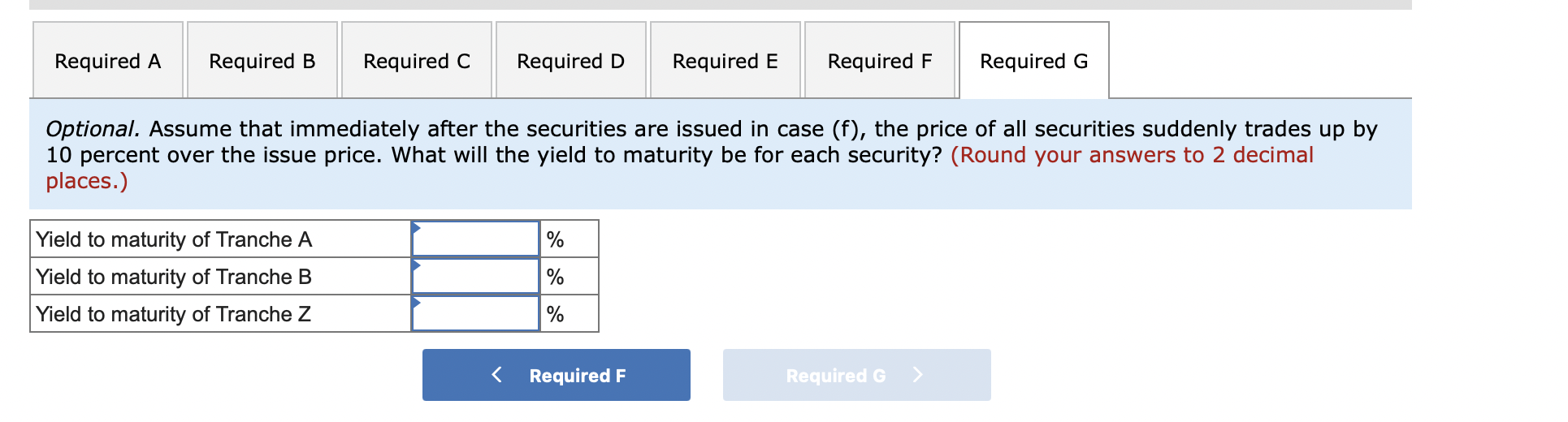

The MZ Mortgage Company is issuing a CMO with three tranches. The A tranche will consist of $40.5 million with a coupon of 8.25 percent. The B tranche will be issued with a coupon of 9.0 percent and a principal of $22.5 million. The Z tranche will carry a coupon of 10.0 percent with a principal of $45 million. The mortgages backing the security issue were originated at a fixed rate of 10 percent with a maturity of 10 years (annual payments). The issue will be overcollateralized by $4.5 million, and the issuer will receive all net cash flows after priority payments are made to each class of securities. Priority payments will be made to the class A tranche and will include the promised coupon, all amortization from the mortgage pool, and interest that will be accrued to the Z class until the principal of $40.5 million due to the A tranche is repaid. The B class securities will receive interest-only payments until the A class is repaid, and then will receive priority payments of amortization and accrued interest. The Z class will accrue interest at 10 percent until both A and B classes are repaid. It will receive current interest and principal payments at that time. Required A Required B Required C Required D Required E Required F Required G What will be the maturity of each tranche assuming no prepayment of mortgages in the pool? years Maturity of Tranche A Maturity of Tranche B years Required A Required B Required C Required D Required E Required F Required G What are the residual cash flows to MZ? What rate of return will be earned on the equity overcollateralization? (Round your answers to 2 decimal places. Negative values should be indicated by a minus sign.) Residual Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Internal Rate of Return % Required A Required B Required C Required D Required E Required F Required G Optional. Assume that the mortgages in the underlying pool prepay at the rate of 10 percent per year. How will your answers in (b)-(e) change? (Round your answers to 2 decimal places. Negative values should be indicated by a minus sign.) years years Maturity of Tranche A Maturity of Tranche B Price of Tranche A Price of Tranche B Price of Tranche Z Residual Year o Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10 Internal Rate of Return % Required A Required B Required C Required D Required E Required F Required G Optional. Assume that immediately after the securities are issued in case (f), the price of all securities suddenly trades up by 10 percent over the issue price. What will the yield to maturity be for each security? (Round your answers to 2 decimal places.) % Yield to maturity of Tranche A Yield to maturity of Tranche B Yield to maturity of Tranche Z % % Required F Required G