Answered step by step

Verified Expert Solution

Question

1 Approved Answer

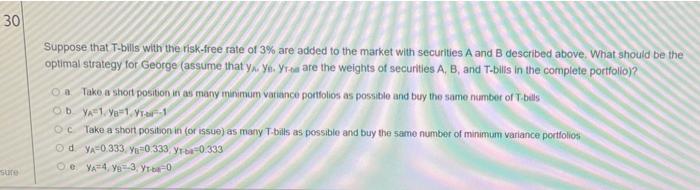

The next three questions are based on the following problem. Consider the market with no T-bills and two risky securities A and B such that

The next three questions are based on the following problem. Consider the market with no T-bills and two risky securities A and B such that E(A) =8.00%, a A =30.00%, E(rB)=15.00%, 0B

=40.00% with the correlation coefficient equal to +1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Securities Trader Qualification Examination Series 57 Study Guide

Authors: Philip Martin Mccaulay

1st Edition

979-8363665240