Answered step by step

Verified Expert Solution

Question

1 Approved Answer

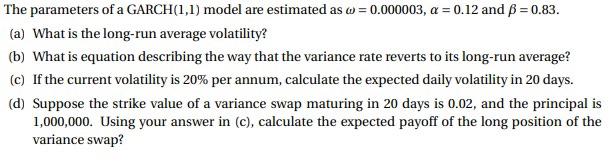

The parameters of a GARCH(1,1) model are estimated as w = 0.000003, a = 0.12 and p = 0.83. (a) What is the long-run average

The parameters of a GARCH(1,1) model are estimated as w = 0.000003, a = 0.12 and p = 0.83. (a) What is the long-run average volatility? (b) What is equation describing the way that the variance rate reverts to its long-run average? (C) If the current volatility is 20% per annum, calculate the expected daily volatility in 20 days. (d) Suppose the strike value of a variance swap maturing in 20 days is 0.02, and the principal is 1,000,000. Using your answer in (c), calculate the expected payoff of the long position of the variance swap

The parameters of a GARCH(1,1) model are estimated as w = 0.000003, a = 0.12 and p = 0.83. (a) What is the long-run average volatility? (b) What is equation describing the way that the variance rate reverts to its long-run average? (C) If the current volatility is 20% per annum, calculate the expected daily volatility in 20 days. (d) Suppose the strike value of a variance swap maturing in 20 days is 0.02, and the principal is 1,000,000. Using your answer in (c), calculate the expected payoff of the long position of the variance swap

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Time Risk What Investors Should Know About FinTech High Frequency Trading And Flash Crashes

Authors: Irene Aldridge , Steven Krawciw

1st Edition

1119318963,1119319048