The problems are attached below.

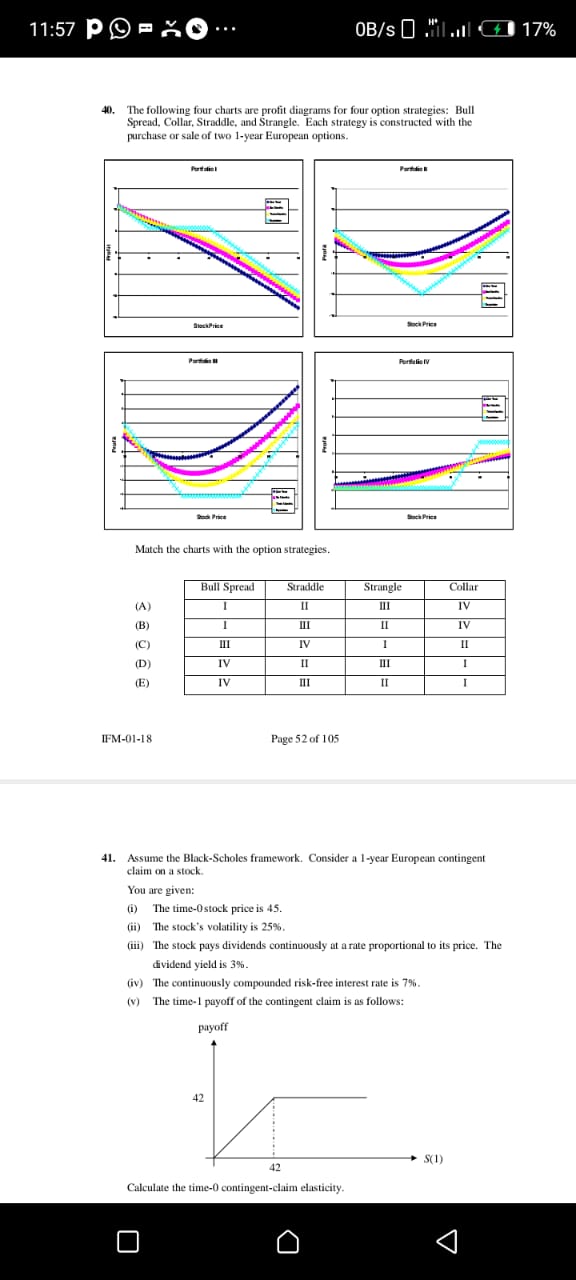

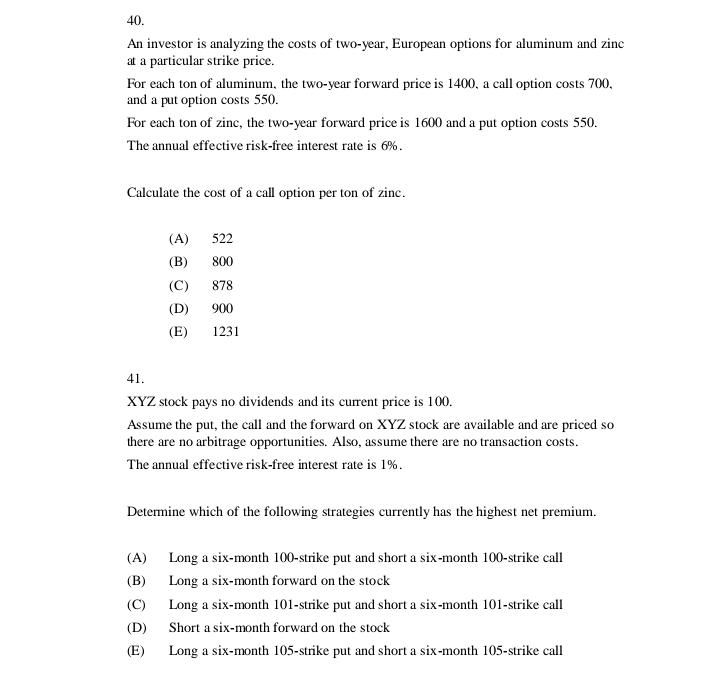

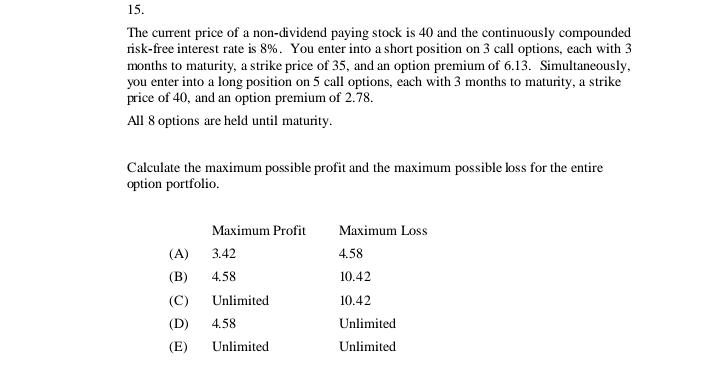

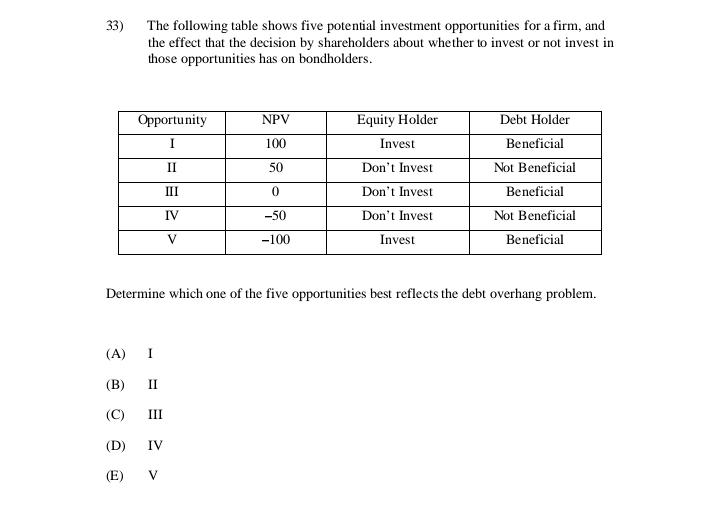

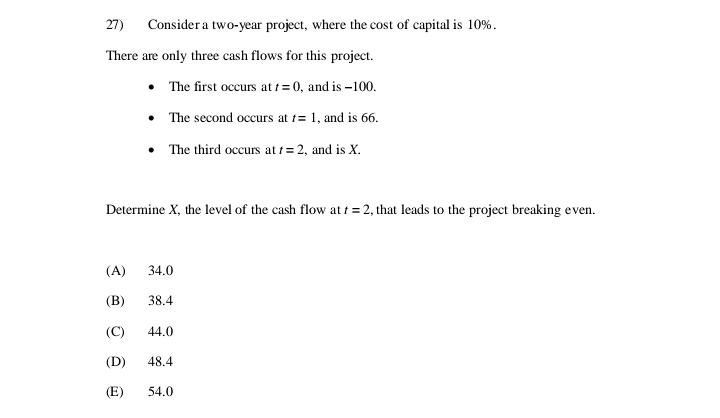

11:57 PO - XO ... OB/s O Mil all +1 17% 40. The following four charts are profit diagrams for four option strategies: Bull Spread, Collar, Straddle, and Strangle. Each strategy is constructed with the purchase or sale of two I-year European options. Shea Pries Match the charts with the option strategies. Bull Spread Straddle Strangle Collar (A) II IV (B) III IV (C) III IV I (D) IV II III I (E) IV IT IFM-01-18 Page 52 of 105 41. Assume the Black-Scholes framework. Consider a 1-year European contingent claim on a stock. You are given: (i) The time-0stock price is 45. (i) The stock's volatility is 25%. fill) The stock pays dividends continuously at a rate proportional to its price. The dividend yield is 3%. iv) The continuously compounded risk-free interest rate is 7%. (v) The time-I payoff of the contingent claim is as follows: payoff 42 S(1) 42 Calculate the time-0 contingent-claim elasticity. O O40. An investor is analyzing the costs of two-year, European options for aluminum and zinc at a particular strike price. For each ton of aluminum. the two-year forward price is 1400. a call option costs 700. and a put option costs $50. For each ton of zinc, the two-year forward price is 1600 and a put option costs $50. The annual effective risk-free interest rate is 6%. Calculate the cost of a call option per ton of zinc. (A) 522 (B) 800 (C) 878 (D) 900 (E) 1231 41. XYZ stock pays no dividends and its current price is 100. Assume the put, the call and the forward on XYZ stock are available and are priced so there are no arbitrage opportunities. Also, assume there are no transaction costs. The annual effective risk-free interest rate is 1%. Determine which of the following strategies currently has the highest net premium. (A) Long a six-month 100-strike put and short a six-month 100-strike call (B) Long a six-month forward on the stock (C) Long a six-month 101-strike put and short a six-month 101-strike call (D) Short a six-month forward on the stock (E) Long a six-month 105-strike put and short a six-month 105-strike call15. What assumptions must be made for the uncovered interest parity condition to hold? Explain what you would expect to happen to the domestic interest rate and the exchange rate in a small open economy following a rise in the demand for money, making clear the role of the UIP condition in this chain of events.10. In Japan, the price of real estate dropped dramatically in the late 1980s. Many Japanese firms have long-term relationships with a so-called main bank. How would you expect a deterioration of the balance sheets of Japanese firms and of their main banks to affect investment? Would you expect smaller or larger firms to be most affected?15. The current price of a non-dividend paying stock is 40 and the continuously compounded risk-free interest rate is 8%. You enter into a short position on 3 call options, each with 3 months to maturity, a strike price of 35, and an option premium of 6.13. Simultaneously, you enter into a long position on 5 call options, each with 3 months to maturity, a strike price of 40, and an option premium of 2.78. All 8 options are held until maturity. Calculate the maximum possible profit and the maximum possible loss for the entire option portfolio. Maximum Profit Maximum Loss (A) 3.42 4.58 (B) 4.58 10.42 (C) Unlimited 10.42 (D) 4.58 Unlimited (E) Unlimited Unlimited33) The following table shows five potential investment opportunities for a firm, and the effect that the decision by shareholders about whether to invest or not invest in those opportunities has on bondholders. Opportunity NPV Equity Holder Debt Holder I 100 Invest Beneficial II 50 Don't Invest Not Beneficial III 0 Don't Invest Beneficial IV -50 Don't Invest Not Beneficial V -100 Invest Beneficial Determine which one of the five opportunities best reflects the debt overhang problem. (A) I (B) II (C) III (D) IV (E) V27) Consider a two-year project, where the cost of capital is 10%. There are only three cash flows for this project. . The first occurs at / = 0, and is -100. . The second occurs at /= 1, and is 66. . The third occurs at / = 2, and is X. Determine X, the level of the cash flow at / = 2, that leads to the project breaking even. (A) 34.0 (B) 38.4 (C) 44.0 (D) 48.4 (E) 54.0