Question

The production manager was perplexed. We are getting so many orders that our old bottling line cant keep up. It breaks down frequently, has low

The production manager was perplexed. We are getting so many orders that our old bottling line cant keep up. It breaks down frequently, has low throughput, lots of breakage and spills, and creates headaches with bad labeling and uneven filling quantities. If we dont upgrade soon, you can say goodbye to the sales targets. And, if the inspectors test the cleanliness of our facility, Id hate to think about the fines.

You know that employee productivity and morale are falling fast because of this unreliable equipment and the tough work environment marked by breakage and spills. One thing is clear: you need a replacement high-capacity bottling line right away. You call two industrial equipment dealers and ask for quotes on a multi-head bottling system. Your only requirement is that, since you lack the cash on hand to make a major purchase anytime soon, you want proposals that allow you to spread the payments over time. Both dealers promise to have bids to you in a week.

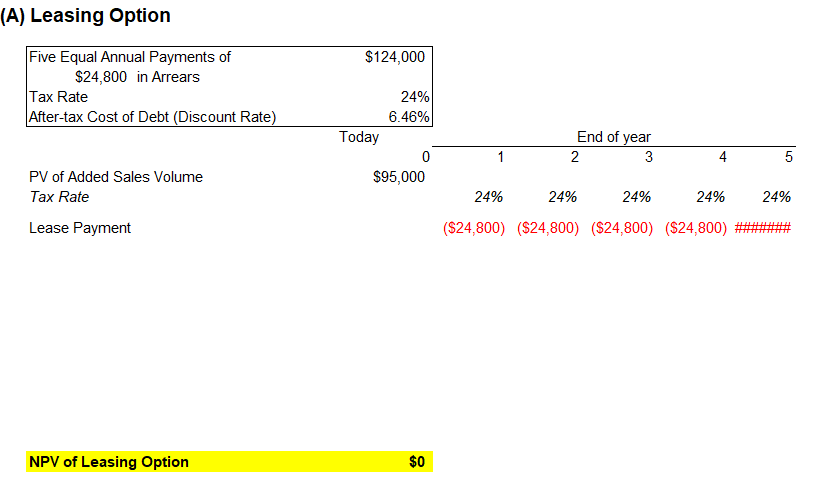

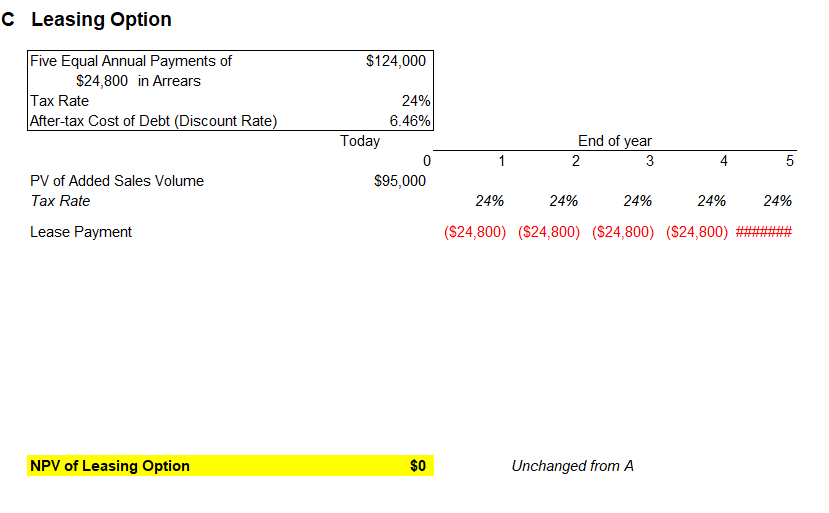

As promised, two bids show up in your email, but they are hard to compare to each other. Barley Equipment is offering a 5-year lease on the FillFast Model M6. The lease is for $24,800 annually payable in arrears, totaling $124,000 over the five years. The lease includes coverage for all major maintenance; but you estimate that you will pay an additional $1,900 annually for incidental maintenance items not covered by the lessor.

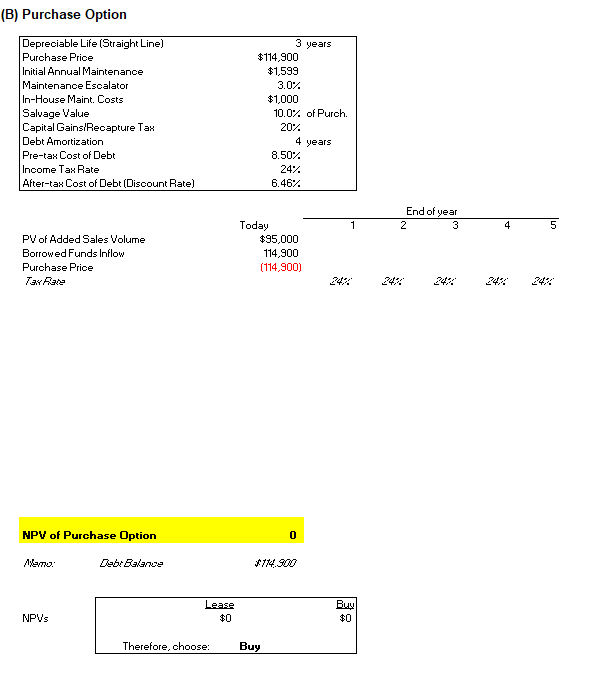

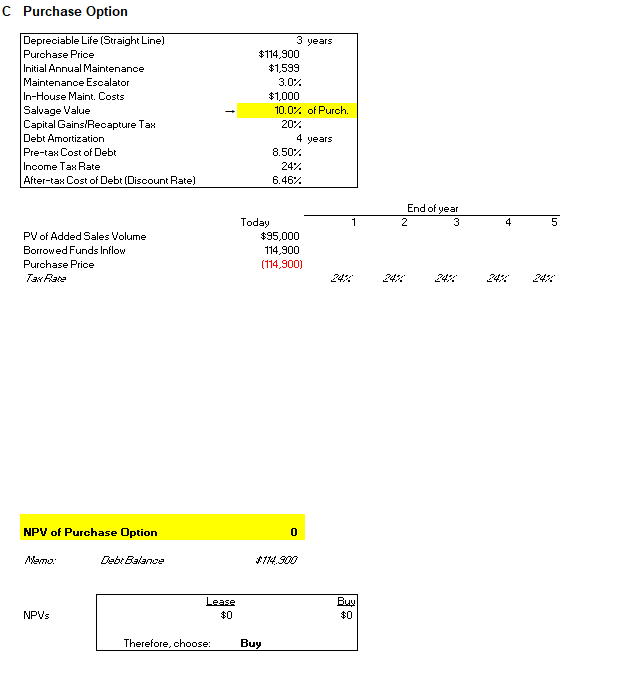

Oast Supply Corporations proposal is different: They are offering to sell an identical FillFast Model M6 to you outright for $114,900. But, knowing that you cant pay for it all at once, Oast offers to finance the entire purchase price at 8.5% interest over four years, with equal annual principal installment payments of $28,725 in arrears plus interest. They also quote a separate major maintenance contract of $1,599 per year for the first year, with an annual renewal clause that includes a 3% annual fee increase. No one at your company has the time or skill to do heavy maintenance of the bottling line, so you know you will have to purchase the add-on maintenance contract. You further estimate that non-covered incidental maintenance will cost an additional $1,000 every year you own the machine.

You decide to gather a few facts and then analyze both proposals to find the one that has the lower cost/higher NPV. First, you estimate that the Present Value today of avoided fines, stockouts, and product waste attributable to the new bottling line is $95,000. This represents a benefit (i.e., cash inflow) at time t=0.

Also, you know that many of the expenses you will pay are tax deductible, meaning that you can reduce the income tax you would have paid otherwise because of expenses associated with equipment use. You decide to discount the cash flows of both proposals by the opportunity cost of funds, which you conclude is the after-tax cost of the proposed 8.5% loan. Since your tax rate is 24%, this means your discount rate is 6.46%. (Your overall anticipated annual profits for the next five years, of which the bottling machinery costs are a small part, are large enough so that you are certain that you will be able to take full advantage of any tax deductions you may claim.)

Your experience tells you that constant usage will lead to wear and tear sufficient to cause you to take the bottling line out of service and replace it after five years. If you choose the lease, the lessor will simply take the bottling equipment back at the end of the 5-year lease. If you own the equipment, you figure that you can sell it for parts to a smaller brewery at the end of 5 years for 10% of its original purchase price

Your accounting manager lets you know that, if you buy the bottling line this year, a special tax incentive program will allow you to depreciate it for tax purposes in a straight line over three (3) years (meaning depreciation expense equal to one-third of the purchase price for years 1, 2, and 3). But if you subsequently sell the equipment for more than its depreciated book value (which is your intention), you will have to pay a recapture capital gains tax at that time equal to 20% of the difference between the actual sale proceeds and the depreciated value of zero.

Just before you start your analysis, you make a few lists to help with this decision. One list is of non-cash charges that are nevertheless tax deductible. The next list is of balance sheet cash flows that have no tax impacts, like the t=0 purchase price (outflow) of $114,900, the original loan (inflow) of $114,900, and the four annual principal repayment outflows. And you continue with a list of cash expenses that will reduce your taxable income, like the major maintenance contract, the incidental upkeep, the interest payments on the loan, and the lease payments.

After you build a lease case and a buy case, you come to a decision.

Questions: A. Build a 5-year pro forma cash flow statement for the lease case and determine its NPV.

B. Build a 5-year pro forma cash flow statement for the buy case and determine its NPV.

C. What salvage value (to the nearest tenth of a percent or xx.x% of original purchase price) makes you indifferent between the two?

To aid in your analysis, please assume all cash flows occur at the end of each relevant period (except the original loan and the bottling line equipment purchase price, which occur at t=0; and the $95,000 imputed benefit cash inflow, also at t=0). Assume interest is paid on the preceding loan balance, and that you then remit both the principal and interest at the same time (year-end). For example, your first (t=1) principal payment will be one-fourth of the loan amount; and your t=1 interest payment will be 8.5% times the previous balance, in this case, $114,900; the following year, the interest will be on the now-lower loan balance. There are no more interest or principal payments once the loan is retired at the end of Year 4.

(A) Leasing Option NPV of Leasing Option $0 (B) Purchase Option C Leasing Option NPV of Leasing Option $0 Unchanged from A Purchase Option (A) Leasing Option NPV of Leasing Option $0 (B) Purchase Option C Leasing Option NPV of Leasing Option $0 Unchanged from A Purchase Option

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Everything Improve Your Credit Book

Authors: Justin Pritchard

1st Edition

1598691554, 978-1598691559