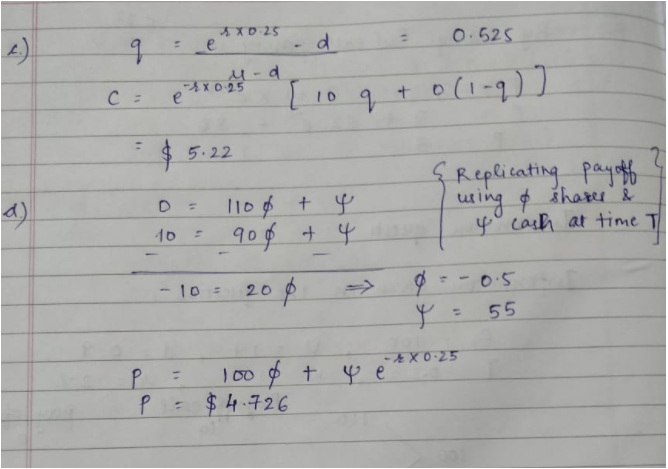

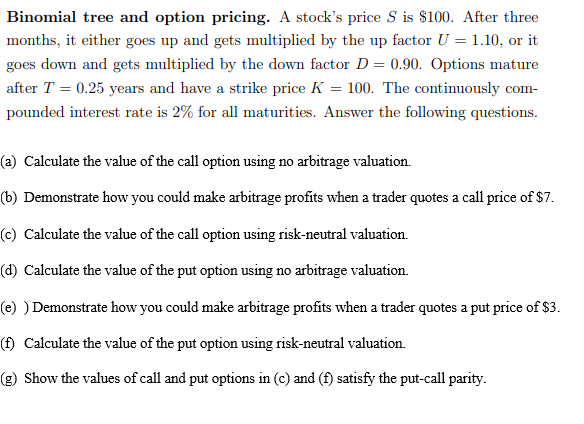

Question

The question does not come with a formula. I have attached answers provided by the other expert for questions a-d. If you could go through

The question does not come with a formula. I have attached answers provided by the other expert for questions a-d. If you could go through this and complete the rest of the questions.

* Please answer the following questions. These questions are a continuation from my last post. Since Chegg policy allows for 4 questions at a time, the first 4 (a-d) has already been answered. I have now posted the remaining 3.

e ) Demonstrate how you could make arbitrage profits when a trader quotes a put price of $3.

f) Calculate the value of the put option using risk-neutral valuation.

g) Show the values of call and put options in (c) and (f) satisfy the put-call parity.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516