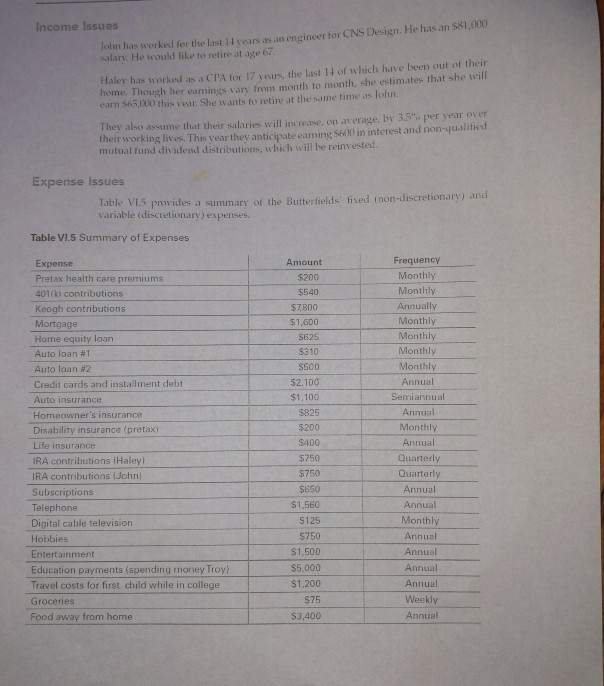

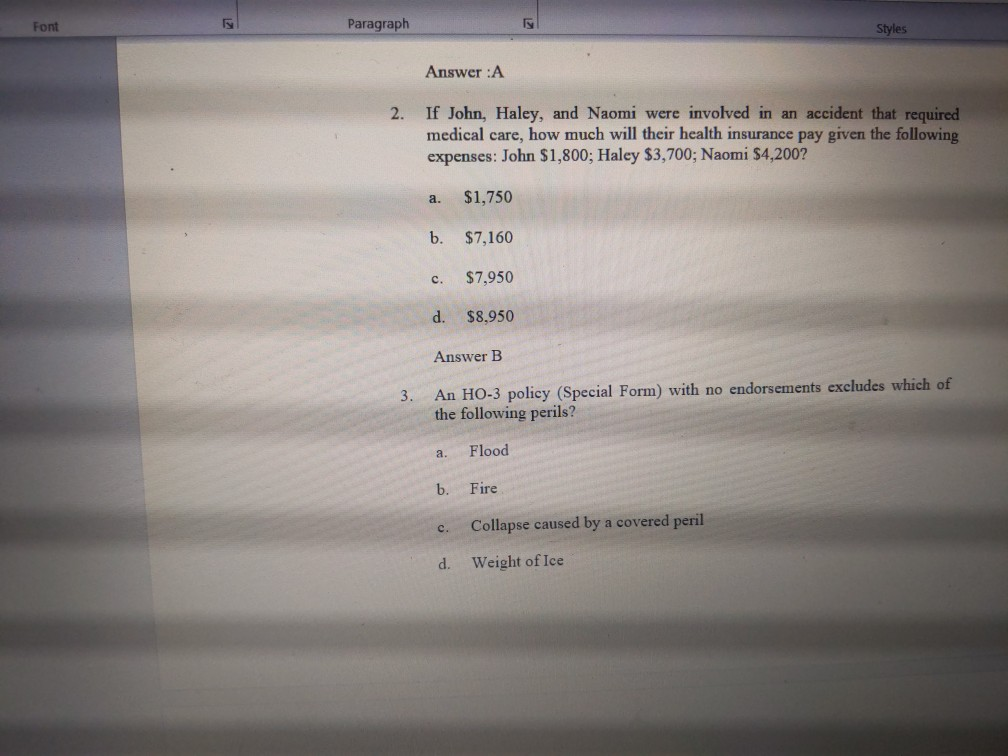

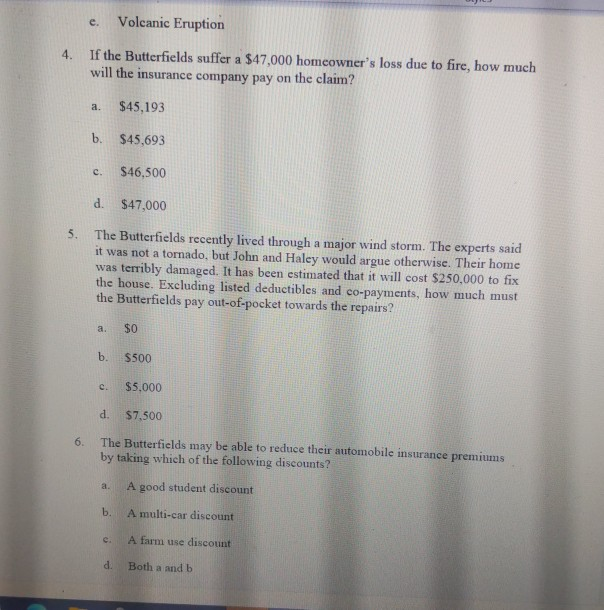

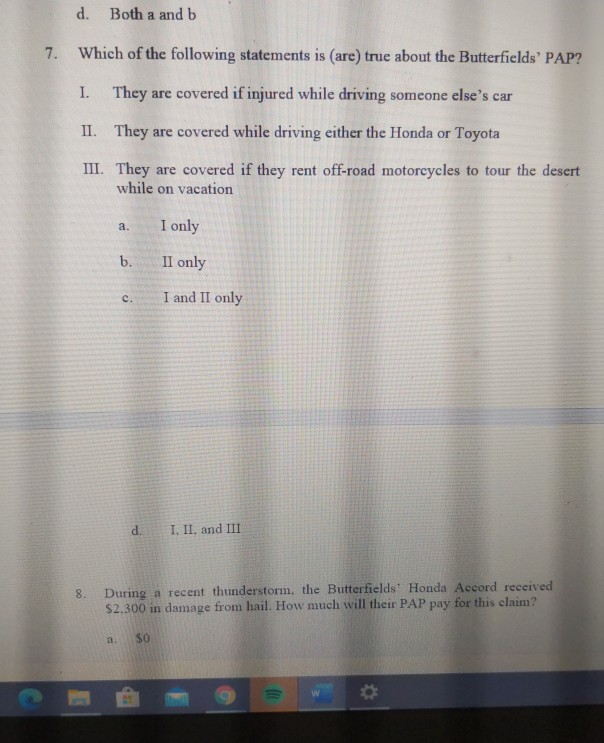

Question: THE QUESTIONS ARE BELOW I appreciate this help very much . The Butterfiells have also allocated $1,200 per vear to help pay for Troy's travel

THE QUESTIONS ARE BELOW

I appreciate this help very much

. The Butterfiells have also allocated $1,200 per vear to help pay for Troy's travel expenses He has completed one vear of college His health insurance is provided under his father's group health plan. Holly wants to attend State University current cost: $10,500/year possible tuition warver) Wants to go to school on an ROTC scholarship and fund any additional expenses out of pocket from money earned during summers. Naomi's college funding goals are unknown, but her parents want to plan for college costs of S16,500 per year in today's dollars). They prefer to use tax-advantaged savings plans to fund any expenses. Retirement Information The Butterfields would like to retire when lohn turns age 67. Based on today's dollars, they are willing to reduce their income by 80'. of current income while retired. At full retirement i.e. age 67) John will receive $18,000 per vear in Social Security benefits: Haler will receive $16.500 in benefits in today's dollars) at age 67. When planning, they are comfortablo assuming a 9.00". rate of return before retirement, and a 5.75" return after retirement. Contributions to their defined contribution plans are anticipated to increase 3.annually. They anticipate being in a combined 25. marginal tax bracket in retirement Inflation before and after retirement will be 3.50, their incomes should keep pace with inflation. John's emplover matches 401(k) contributions $0.50 cents on the dollar. IRA assets are held in Roth accounts. Assumed age at death for John is age 0 and age 92 for Halev. Estate Information They both have simple wills. John leaves his estate to Haley and Haley leaves her state to John. They believe that, on average, their estate will grow by "w after the first spouse's death. Other assumptions include: Funeral expenses are expected to be approximately 512,700 each. Estate administrative expenses will be $5,200 each. . . The Butterfield do not expect to pav anv executor fees. In the event of either spouse's death, the other spouse plans to stop working at age 60 and begin taking early retirement survivor benefits if available) For conservative planning purposes the Butterfields do not plan on using interest and/or dividends as an income source when planning insurance needs. At full retiremente, at age 67) lohn will receive $18.000 per vear in Social Security benefits: Haley will receive $16.500 in benefits in today's dollars). Assumed ages at death for lohny and Haley are 90 and 2, respectively, The assumed gross rate of return on insurance assets, in the event of death, is 9 Health. The Buttertields health insurance is provided by Blue Cross/Blue Shield. The monthly premium of $600 is paid 66 by John's emplover, with the remainder paid out of pocket. The plan has a deductible of $250 per person and a family copayment of 20. The out-of-pocket per family cap on copayments is $1.000 per vear. The lifetime maximum on major medical is $500,000 per person. Long-term care. None Disability. John's disability coverage is a group disability contract provided by his emplover. It pars a $5,000 monthly benefit until age 65. The contract has a liberal own occupation definition. The elimination period is 120 days. Halev does not have a disability policy. In the event of a disability, the Butterhelds would like to continue saving for other goals; however, they do not want to rely on Social Security disability benefits when estimating disability income needs Vacation/medical leave. John has accumulated 30 sick das, which is the maximum he is allowed to carry. He could accrue one week per year if he fell below the maximum He also is eligible for three weeks of vacation per year. He can carry over one week, but this has not previously been done. Education Funding Goals The Butterfields would like to assume that education expenses will increase 6.50 per year. They are comfortable assuming a growth rate of 9.00". per year for educational assets and savings in a tax-advantaged account before and after college begins (675 it assets are held in a taxable account). Each of the children is talented academically GPA 3.0) and in terms of extracurricular activities. Trow is currently enrolled at University of Anystate. Current cost: S11,700/vear Waiver) He is on a fi baseball scholarship. His parents budget $5,000 per rear in extra support; they pay tuition not covered in the scholarship and give Troy what is left from their 55.000 budget as a spending allowance 770 Case Approach to Financial Planning Daluctible: $500 Personal property: 50.of dwelling Bodily injury: S100.000 Personal injury: Other endorsements: None Umbrella None Professional liability: None Business: None Life and Health Life. Haley has a $50,000 universal life policy with XYZ Insurance Co. She pars the annual premium of $100. The policy has a current cash value of $3,800 (the cash value at the beginning of the period was 3,600). John is the primary beneficiary and Halev is the owner. At the time of purchase, policy projections were based on after-tax U.S. Treasury rates of lohnt has an employer-provided term policy that pars one times his annual salar. The face amount of the policy is reduced by 50%. regardless of his salary, at 65 and terminates at age 70. Other lite assumptions: . For planning purposes, the Butterfields would like to use 8. of their combined incomes, before taxes, to represent their total household expenses in the event of a death . Final illness and burial expenses are estimated to be $15,000 each. Estate administration expenses are expected to be approximately $5.200 each. Child care expenses will be $10.000 . Full retirement age, for insurance purposes, is assumed to be age 67 The Butterfields need $100.000 in annual income per year before taxes. while retired. They would like to use this assumption for both insurance and retirement planning purposes Social Security benefit while children are still at home is $32,000 it lohndes and $29,000 il Haley dies, in today's dollars. . At age 60, Haley is eligible for a $13.000 annual Social Security survivor benefit. while lohn is entitled to a $10,000 annual survivor benefit in today's dollars), Additional Case Studies The Butterfields Case: An Insurance Planning Case Study Case Questions 1. Which of the following is true if Haley closes her accounting firm to join a large consulting company this year? a. HIPAA rules guarantee that her new employer will immediately pay for any pre-existing conditions she might currently have. b. She will need to continue her current insurance coverage under COBRA provisions. c. She will be required to drop her current coverage through John's employer if she accepts insurance through her new employer. d. She may remain on John's health insurance policy until she is fully covered under her new employer's insurance plan. Property and Casualty Auto. All vehicles Liability: $300,000 single limit (including uninsured motorist) Medical payments coverage: $1,000 limit per person Deductible: $250 collision: $100 comprehensive Premium: $1,100 every six months Ante l: 20XX Honda Accord LX Sedan Mileage: 30,000 Color: light blue Engine: 6-cylinder Transmission: manual Payment: $310/month Balance: $8,500 with 2.5 years remaining Worth: $17.500 Anto?: 20XX Toyota Sequoia Limited (4x4) Mileage: 5,500 Color: silver Engine: 8-cvlinder Transmission: automatic Payment: $500/month Balance: $25,000 with 57 months remaining Worth: $38,000 Home. Single-family dwelling Insured value: $245,000 Replacement value: 5315,000 Specific Client Goals Under any circumstance, they want to provide 50% of the cost of Holly's and Naomi's college education costs, and all of Troy's education costs that are not covered by scholarships They want to maintain their current standard of living in retirement or in the event of either spouse's premature death They want to protect their income and assets in the event of a catastrophic accident or illness, so that they can pass on their assets to their children, They both want to continue funding their IRAs to the current maximum limit See Table V16 for information on the Butterfields' assets and liabilities. Table VI. 6 The Butterfields' Assets and Liablities Asset Checking account Large-cap mutual fund Checking account Small-cap mutual fund Life insurance cash value Checking account Savings account Money market account Mid-cap mutual fund Artwork 401K Keogh retirement plan Individual retirement account (RA) Individual retirement account (RA) Home Honda Toyota Collectibles Furniture Other assets Misc. assets Liabilities Visa credit card MasterCard Mortgage Home equity loan Honda Toyota Short-term installment debt Amount $950 $9,000 $1,200 $17,250 $3,800 $2,800 $7,500 $10,050 S40,000 $25,000 $62,000 $125,000 S38,000 $41,500 $315,000 $17.500 $38,000 $13,000 $17.500 S69,000 $39.000 Amount $2.500 $4,900 $206,602 $32,000 $8,500 $25.000 $21,000 Ownership Client Client Co-client Co-client Co-client Joint Joint Joint Joint Joint Client Co-client Client Co-client Joint Joint Joint Co-client Client Joint Joint Ownership Co-client Joint Joint Joint Joint Joint Client Financial Planning Case Studies 767 Real estate taxes Household maintenance Utilities Clothing Dry cleaning Personal care Furnishing Allowances Medical copayments Prescriptions Gas Personal property tax Banking fees IR A fees Travel Contributions to church Vacations Christmas gifts $1.300 $2,700 $175 $1.500 $50 S500 $1,000 S2,000 S700 S250 $2,500 $400 S75 SBO $100 S125 $3,000 $2.400 Annual Annual Month Annual Month Annual Annual Annual Annual Annual Annual Semiannual Annual Annual Monthly Monthly Annual Annual Home mortgage. They are eight years into a 30-year 7.5". mortgage that had an original balance of $228,850, with a current outstanding balance of $206,602 Home equity loan. The loan balance was used to pay off credit cards and purchase a vehicle for Troy to useat college. Since the loan was first taken, they have accumulated additional credit card debt. The monthly payment is approximately 2. of the outstanding balance. The credit line expires and will be due and payable in seven years. They have paid $3,000 in interest over the past vear. Auto Payments Auto 1: Balance is $8,500 with 2.5 years remaining Auto 2: Balance is $25,000 with 57 months remaining Tax Issues After reviewing their par stubs, John and Haley calculated that theirtotalannual federal withholdings and/or estimated tax paviments totaled $20.250. Their state withholdings amounted to $8,000. Social Security withheld was $10.985. The Butterfields bile taxes as married filing jointly and have $30,241 in itemized deductions for the year. The Butterfields are eligible for a 55.000 state income tax deduction, and five $1,000-personal exemptions for John, Haley, and the children. The marginal tax bracket for their state is 5.75 Case 5 The Butterfield Case AN INSURANCE PLANNING MINI-CASE lohn Butterfield, 19, and his wite Haley Butterfield, H. live in a relatively new home on the outskirts of Anycity. Anystate. They have been married for 23 years and have three children. Both lohn and Haley are in excellent health. Their son Trow.ope 20.is baseball player on scholarship at the University of Anw state. Daughter Holly, age 17 hopes to attend State University next fall as a cadet to begin pursuing a career in the Marine Corps The choices of their first two children have allowed the Butterfields to concentrate their college saving goals on Naomi, the youngest at age 13. John and Haley have come to you for help in addressing several insurance planning questions and concerns. Use the following information to conduct a review of their financial situation and use your analyses to answer the questions that follow the case narrative Global Assumptions (Valid unless otherwise Specified in certain instances) Intation: 3.5 All income and expense figures are given in today's dollars. Federal marginal tax bracket: 25". State marginal tax bracket: 5.75 Any qualified plan or IRA contribution growth rates are assumed to stop at the federally mandated limit unless otherwise restricted. All nominal rates of return are pretax retums. 765 Income Issues Johan has worked for the last 1 years as an engineer for CNS Design. He has an 581,000 salary. He would like to retire at age 67 Haley has worked as a CPA for 17 years, the last 11 of which have been out of their home. Though her varnings van from month to month, she estimates that she will cam $65.000 this rear. She wants to retire at the same time as lohn. They also assume that their salaries will increase, on average, by 3,5" per vear over their working lives. This year they anticipate eaming 5600 in interest and non-qualified mutual fund dividend distributions, which will be reinvested Expense Issues Table Vis provides a summary of the Butterfields fixed (non-discretionary and variable (discretionary) expenses. Table VI.5 Summary of Expenses Expense Pretax health care premiums 401(k) contributions Keogh contributions Mortgage Home equity loan Auto loan #1 Auto loan 2 Credit cards and installment debt Auto insurance Homeowner's insurance Disability insurance (pretaxi Life insurance IRA contributions Haley! IRA contributions (John Subscriptions Telephone Digital cable television Hobbies Entertainment Education payments (spending money Troy! Travel costs for first child while in college Groceries Food away from home Amount $200 $540 $7,800 $1,500 5625 $310 S500 52.100 $1,100 $825 $200 $400 $750 $750 $650 $1.560 $125 $750 $1,500 $5,000 $1.200 $75 $3,400 Frequency Monthly Monthly Annually Monthly Monthly Monthly Monthly Annual Semiannual Annual Monthly Annual Quarterly Quarterly Annual Annual Monthly Annual Annual Annual Annual Weekly Annual Font Paragraph Styles Answer:A 2. If John, Haley, and Naomi were involved in an accident that required medical care, how much will their health insurance pay given the following expenses: John $1,800; Haley $3,700; Naomi $4,2002 a. $1,750 b. $7,160 c. $7,950 d. $8.950 Answer B 3. An HO-3 policy (Special Form) with no endorsements excludes which of the following perils? a. Flood b. Fire c. Collapse caused by a covered peril d. Weight of Ice e. Volcanic Eruption 4. If the Butterfields suffer a $47,000 homeowner's loss due to fire, how much will the insurance company pay on the claim? a. $45,193 b. $45,693 c. $46,500 d. $47,000 5. The Butterfields recently lived through a major wind storm. The experts said it was not a tornado, but John and Haley would argue otherwise. Their home was terribly damaged. It has been estimated that it will cost $250,000 to fix the house. Excluding listed deductibles and co-payments, how much must the Butterfields pay out-of-pocket towards the repairs? a. $0 b. $500 c. $5.000 d. $7.500 6. The Butterfields may be able to reduce their automobile insurance premiums by taking which of the following discounts? a. A good student discount b. A multi-car discount A farm use discount d. Botha and b d. Both a and b 7. Which of the following statements is (are) true about the Butterfields' PAP? 1. They are covered if injured while driving someone else's car II. They are covered while driving either the Honda or Toyota III. They are covered if they rent off-road motorcycles to tour the desert while on vacation a. I only b. II only c. I and II only d. I. II. and III 8. During a recent thunderstorm, the Butterfields Honda Accord received $2.300 in damage from hail. How much will their PAP pay for this claim? SO 8. During a recent thunderstorm, the Butterfields' Honda Accord received $2,300 in damage from hail. How much will their PAP pay for this claim? $0 b. $2,050 C. $2,200 d. $2,300 9. Haley is worried that her oldest son, Troy, will be without health insurance after he graduates from college in a few years. Which of the following are realistic insurance options for Troy once he graduates? Extend his current coverage through a COBRA extension II. Purchase insurance through an offshore Asian state-sponsored high risk I. pool III. Purchase insurance through a private company a I only b I and II only c I and III only d. II and III only e I. II. and III 10. Which of the following risk management recommendations are most appropriate to help the Butterfields manage their risk exposures? I. Purchase an excess liability insurance policy II Decrease their homeowner's coverage to 80% of the home's value AaBbCcDa AaBbCel AaBbCel AaBbC1 AaBbCcl AaBbc Emphasis 1 Heading 1 1 Heading 2 1 Heading 3 1 Heading 4 1 Headin Paragraph Styles 10. Which of the following risk management recommendations are most appropriate to help the Butterfields manage their risk exposures? I. Purchase an excess liability insurance policy II. Decrease their homeowner's coverage to 80% of the home's value III. Eliminate collision coverage on the Toyota IV. Purchase an endorsement to cover their art collection a. I and III only b. II and IV only c. II and III only d. I and IV only 11. Which of the following strategies can the Butterfields use to increase their current discretionary cash flow situation? a. Increase the deductible in their PAP policy. b. Purchase an umbrella liability insurance policy. c. Decrease the deductible in their HO policy. d. All of the above. 12. The Butterfields are not sure if they are paying an appropriate premium for their universal life insurance policy. Which statement shown below is true in relation to this concern? a. The universal life policy is fairly priced according to the Yearly Price per Thousand formula. b Even though the Yearly Price per Thousand formula states that the policy is over priced, given Haley's health status, she should hold the policy because she probably will not qualify for another policy. c. Even though the universal policy is expensive, they should not replace it because the cost is less than two times the Yearly Price per Thousand formula benchmark price: Haley should replace the universal policy because, according to the Yearly Price per Thousand formula, the cost is more than two times the benchmark price d. 13. Haley would like to know the difference between variable life insurance and 1 life insurance Which of the following statements A cl AaBbc Emphasis 1 Heading 1 1 Heading 2 T Heading 3 1 Heading 4 1 Headir Paragraph Styles 13. Haley would like to know the difference between variable life insurance and universal life insurance. Which of the following statements is most accurate in describing the difference? a. Variable life insurance uses sub-contracts that are invested to generate a guaranteed rate of return. b. Universal life insurance uses a fixed mortality charge, while variable life insurance does not. c. Variable life insurance has a death benefit that varies, while universal life insurance only provides a fixed death benefit. d. Universal life insurance provides a crediting rate based on the insurance company's general account subject to a minimum guarantee, while variable life insurance uses sub-accounts that can fluctuate based on market returns. 12A ALT AaBbCcDa AaBbCcl AaBbCcl AaBbci AaBbCcl Emphasis 1 Heading 1 1 Heading 2 1 Heading 3 1 Heading 4 Font Paragraph Styles 14. Which of the following statements best describes the Butterfields' disability insurance need at this time? I. John has adequate long-term disability coverage II. John does not have adequate short-term disability coverage III. Haley does not need disability coverage at this time IV. John has adequate short-term disability coverage a. II only b. I and IV only c. II and III only d. II and IV only Discussion Points and Questions (Please create a separate Word document to answer each of these questions) Briefly summarize the relevant facts of the case relating to insurance planning to purchase additional life insurance what type 2. If the Butterfields were going to purchase additional life insurance what type of policy, what face value, and what riders would be most appropriate given their age and need? 3. Explain the advantages and disadvantages of having John purchase additional life insurance through his employer. 4. Describe the 80% co-insurance rule and report to the Butterfields how this rule affects their homeowner's coverage. 5. What actions can the Butterfields take to reduce their insurance premiums while maintaining adequate coverage in terms of liability and property coverage? 6. Explain why the Butterfields should consider purchasing an excess liability insurance policy Describe the purpose of long-term care insurance and indicate if and when the Butterfields should consider purchasing this type of insurance. 7. 8. Report on the advantages and disadvantages associated with the Butterfields current health insurance policy. . The Butterfiells have also allocated $1,200 per vear to help pay for Troy's travel expenses He has completed one vear of college His health insurance is provided under his father's group health plan. Holly wants to attend State University current cost: $10,500/year possible tuition warver) Wants to go to school on an ROTC scholarship and fund any additional expenses out of pocket from money earned during summers. Naomi's college funding goals are unknown, but her parents want to plan for college costs of S16,500 per year in today's dollars). They prefer to use tax-advantaged savings plans to fund any expenses. Retirement Information The Butterfields would like to retire when lohn turns age 67. Based on today's dollars, they are willing to reduce their income by 80'. of current income while retired. At full retirement i.e. age 67) John will receive $18,000 per vear in Social Security benefits: Haler will receive $16.500 in benefits in today's dollars) at age 67. When planning, they are comfortablo assuming a 9.00". rate of return before retirement, and a 5.75" return after retirement. Contributions to their defined contribution plans are anticipated to increase 3.annually. They anticipate being in a combined 25. marginal tax bracket in retirement Inflation before and after retirement will be 3.50, their incomes should keep pace with inflation. John's emplover matches 401(k) contributions $0.50 cents on the dollar. IRA assets are held in Roth accounts. Assumed age at death for John is age 0 and age 92 for Halev. Estate Information They both have simple wills. John leaves his estate to Haley and Haley leaves her state to John. They believe that, on average, their estate will grow by "w after the first spouse's death. Other assumptions include: Funeral expenses are expected to be approximately 512,700 each. Estate administrative expenses will be $5,200 each. . . The Butterfield do not expect to pav anv executor fees. In the event of either spouse's death, the other spouse plans to stop working at age 60 and begin taking early retirement survivor benefits if available) For conservative planning purposes the Butterfields do not plan on using interest and/or dividends as an income source when planning insurance needs. At full retiremente, at age 67) lohn will receive $18.000 per vear in Social Security benefits: Haley will receive $16.500 in benefits in today's dollars). Assumed ages at death for lohny and Haley are 90 and 2, respectively, The assumed gross rate of return on insurance assets, in the event of death, is 9 Health. The Buttertields health insurance is provided by Blue Cross/Blue Shield. The monthly premium of $600 is paid 66 by John's emplover, with the remainder paid out of pocket. The plan has a deductible of $250 per person and a family copayment of 20. The out-of-pocket per family cap on copayments is $1.000 per vear. The lifetime maximum on major medical is $500,000 per person. Long-term care. None Disability. John's disability coverage is a group disability contract provided by his emplover. It pars a $5,000 monthly benefit until age 65. The contract has a liberal own occupation definition. The elimination period is 120 days. Halev does not have a disability policy. In the event of a disability, the Butterhelds would like to continue saving for other goals; however, they do not want to rely on Social Security disability benefits when estimating disability income needs Vacation/medical leave. John has accumulated 30 sick das, which is the maximum he is allowed to carry. He could accrue one week per year if he fell below the maximum He also is eligible for three weeks of vacation per year. He can carry over one week, but this has not previously been done. Education Funding Goals The Butterfields would like to assume that education expenses will increase 6.50 per year. They are comfortable assuming a growth rate of 9.00". per year for educational assets and savings in a tax-advantaged account before and after college begins (675 it assets are held in a taxable account). Each of the children is talented academically GPA 3.0) and in terms of extracurricular activities. Trow is currently enrolled at University of Anystate. Current cost: S11,700/vear Waiver) He is on a fi baseball scholarship. His parents budget $5,000 per rear in extra support; they pay tuition not covered in the scholarship and give Troy what is left from their 55.000 budget as a spending allowance 770 Case Approach to Financial Planning Daluctible: $500 Personal property: 50.of dwelling Bodily injury: S100.000 Personal injury: Other endorsements: None Umbrella None Professional liability: None Business: None Life and Health Life. Haley has a $50,000 universal life policy with XYZ Insurance Co. She pars the annual premium of $100. The policy has a current cash value of $3,800 (the cash value at the beginning of the period was 3,600). John is the primary beneficiary and Halev is the owner. At the time of purchase, policy projections were based on after-tax U.S. Treasury rates of lohnt has an employer-provided term policy that pars one times his annual salar. The face amount of the policy is reduced by 50%. regardless of his salary, at 65 and terminates at age 70. Other lite assumptions: . For planning purposes, the Butterfields would like to use 8. of their combined incomes, before taxes, to represent their total household expenses in the event of a death . Final illness and burial expenses are estimated to be $15,000 each. Estate administration expenses are expected to be approximately $5.200 each. Child care expenses will be $10.000 . Full retirement age, for insurance purposes, is assumed to be age 67 The Butterfields need $100.000 in annual income per year before taxes. while retired. They would like to use this assumption for both insurance and retirement planning purposes Social Security benefit while children are still at home is $32,000 it lohndes and $29,000 il Haley dies, in today's dollars. . At age 60, Haley is eligible for a $13.000 annual Social Security survivor benefit. while lohn is entitled to a $10,000 annual survivor benefit in today's dollars), Additional Case Studies The Butterfields Case: An Insurance Planning Case Study Case Questions 1. Which of the following is true if Haley closes her accounting firm to join a large consulting company this year? a. HIPAA rules guarantee that her new employer will immediately pay for any pre-existing conditions she might currently have. b. She will need to continue her current insurance coverage under COBRA provisions. c. She will be required to drop her current coverage through John's employer if she accepts insurance through her new employer. d. She may remain on John's health insurance policy until she is fully covered under her new employer's insurance plan. Property and Casualty Auto. All vehicles Liability: $300,000 single limit (including uninsured motorist) Medical payments coverage: $1,000 limit per person Deductible: $250 collision: $100 comprehensive Premium: $1,100 every six months Ante l: 20XX Honda Accord LX Sedan Mileage: 30,000 Color: light blue Engine: 6-cylinder Transmission: manual Payment: $310/month Balance: $8,500 with 2.5 years remaining Worth: $17.500 Anto?: 20XX Toyota Sequoia Limited (4x4) Mileage: 5,500 Color: silver Engine: 8-cvlinder Transmission: automatic Payment: $500/month Balance: $25,000 with 57 months remaining Worth: $38,000 Home. Single-family dwelling Insured value: $245,000 Replacement value: 5315,000 Specific Client Goals Under any circumstance, they want to provide 50% of the cost of Holly's and Naomi's college education costs, and all of Troy's education costs that are not covered by scholarships They want to maintain their current standard of living in retirement or in the event of either spouse's premature death They want to protect their income and assets in the event of a catastrophic accident or illness, so that they can pass on their assets to their children, They both want to continue funding their IRAs to the current maximum limit See Table V16 for information on the Butterfields' assets and liabilities. Table VI. 6 The Butterfields' Assets and Liablities Asset Checking account Large-cap mutual fund Checking account Small-cap mutual fund Life insurance cash value Checking account Savings account Money market account Mid-cap mutual fund Artwork 401K Keogh retirement plan Individual retirement account (RA) Individual retirement account (RA) Home Honda Toyota Collectibles Furniture Other assets Misc. assets Liabilities Visa credit card MasterCard Mortgage Home equity loan Honda Toyota Short-term installment debt Amount $950 $9,000 $1,200 $17,250 $3,800 $2,800 $7,500 $10,050 S40,000 $25,000 $62,000 $125,000 S38,000 $41,500 $315,000 $17.500 $38,000 $13,000 $17.500 S69,000 $39.000 Amount $2.500 $4,900 $206,602 $32,000 $8,500 $25.000 $21,000 Ownership Client Client Co-client Co-client Co-client Joint Joint Joint Joint Joint Client Co-client Client Co-client Joint Joint Joint Co-client Client Joint Joint Ownership Co-client Joint Joint Joint Joint Joint Client Financial Planning Case Studies 767 Real estate taxes Household maintenance Utilities Clothing Dry cleaning Personal care Furnishing Allowances Medical copayments Prescriptions Gas Personal property tax Banking fees IR A fees Travel Contributions to church Vacations Christmas gifts $1.300 $2,700 $175 $1.500 $50 S500 $1,000 S2,000 S700 S250 $2,500 $400 S75 SBO $100 S125 $3,000 $2.400 Annual Annual Month Annual Month Annual Annual Annual Annual Annual Annual Semiannual Annual Annual Monthly Monthly Annual Annual Home mortgage. They are eight years into a 30-year 7.5". mortgage that had an original balance of $228,850, with a current outstanding balance of $206,602 Home equity loan. The loan balance was used to pay off credit cards and purchase a vehicle for Troy to useat college. Since the loan was first taken, they have accumulated additional credit card debt. The monthly payment is approximately 2. of the outstanding balance. The credit line expires and will be due and payable in seven years. They have paid $3,000 in interest over the past vear. Auto Payments Auto 1: Balance is $8,500 with 2.5 years remaining Auto 2: Balance is $25,000 with 57 months remaining Tax Issues After reviewing their par stubs, John and Haley calculated that theirtotalannual federal withholdings and/or estimated tax paviments totaled $20.250. Their state withholdings amounted to $8,000. Social Security withheld was $10.985. The Butterfields bile taxes as married filing jointly and have $30,241 in itemized deductions for the year. The Butterfields are eligible for a 55.000 state income tax deduction, and five $1,000-personal exemptions for John, Haley, and the children. The marginal tax bracket for their state is 5.75 Case 5 The Butterfield Case AN INSURANCE PLANNING MINI-CASE lohn Butterfield, 19, and his wite Haley Butterfield, H. live in a relatively new home on the outskirts of Anycity. Anystate. They have been married for 23 years and have three children. Both lohn and Haley are in excellent health. Their son Trow.ope 20.is baseball player on scholarship at the University of Anw state. Daughter Holly, age 17 hopes to attend State University next fall as a cadet to begin pursuing a career in the Marine Corps The choices of their first two children have allowed the Butterfields to concentrate their college saving goals on Naomi, the youngest at age 13. John and Haley have come to you for help in addressing several insurance planning questions and concerns. Use the following information to conduct a review of their financial situation and use your analyses to answer the questions that follow the case narrative Global Assumptions (Valid unless otherwise Specified in certain instances) Intation: 3.5 All income and expense figures are given in today's dollars. Federal marginal tax bracket: 25". State marginal tax bracket: 5.75 Any qualified plan or IRA contribution growth rates are assumed to stop at the federally mandated limit unless otherwise restricted. All nominal rates of return are pretax retums. 765 Income Issues Johan has worked for the last 1 years as an engineer for CNS Design. He has an 581,000 salary. He would like to retire at age 67 Haley has worked as a CPA for 17 years, the last 11 of which have been out of their home. Though her varnings van from month to month, she estimates that she will cam $65.000 this rear. She wants to retire at the same time as lohn. They also assume that their salaries will increase, on average, by 3,5" per vear over their working lives. This year they anticipate eaming 5600 in interest and non-qualified mutual fund dividend distributions, which will be reinvested Expense Issues Table Vis provides a summary of the Butterfields fixed (non-discretionary and variable (discretionary) expenses. Table VI.5 Summary of Expenses Expense Pretax health care premiums 401(k) contributions Keogh contributions Mortgage Home equity loan Auto loan #1 Auto loan 2 Credit cards and installment debt Auto insurance Homeowner's insurance Disability insurance (pretaxi Life insurance IRA contributions Haley! IRA contributions (John Subscriptions Telephone Digital cable television Hobbies Entertainment Education payments (spending money Troy! Travel costs for first child while in college Groceries Food away from home Amount $200 $540 $7,800 $1,500 5625 $310 S500 52.100 $1,100 $825 $200 $400 $750 $750 $650 $1.560 $125 $750 $1,500 $5,000 $1.200 $75 $3,400 Frequency Monthly Monthly Annually Monthly Monthly Monthly Monthly Annual Semiannual Annual Monthly Annual Quarterly Quarterly Annual Annual Monthly Annual Annual Annual Annual Weekly Annual Font Paragraph Styles Answer:A 2. If John, Haley, and Naomi were involved in an accident that required medical care, how much will their health insurance pay given the following expenses: John $1,800; Haley $3,700; Naomi $4,2002 a. $1,750 b. $7,160 c. $7,950 d. $8.950 Answer B 3. An HO-3 policy (Special Form) with no endorsements excludes which of the following perils? a. Flood b. Fire c. Collapse caused by a covered peril d. Weight of Ice e. Volcanic Eruption 4. If the Butterfields suffer a $47,000 homeowner's loss due to fire, how much will the insurance company pay on the claim? a. $45,193 b. $45,693 c. $46,500 d. $47,000 5. The Butterfields recently lived through a major wind storm. The experts said it was not a tornado, but John and Haley would argue otherwise. Their home was terribly damaged. It has been estimated that it will cost $250,000 to fix the house. Excluding listed deductibles and co-payments, how much must the Butterfields pay out-of-pocket towards the repairs? a. $0 b. $500 c. $5.000 d. $7.500 6. The Butterfields may be able to reduce their automobile insurance premiums by taking which of the following discounts? a. A good student discount b. A multi-car discount A farm use discount d. Botha and b d. Both a and b 7. Which of the following statements is (are) true about the Butterfields' PAP? 1. They are covered if injured while driving someone else's car II. They are covered while driving either the Honda or Toyota III. They are covered if they rent off-road motorcycles to tour the desert while on vacation a. I only b. II only c. I and II only d. I. II. and III 8. During a recent thunderstorm, the Butterfields Honda Accord received $2.300 in damage from hail. How much will their PAP pay for this claim? SO 8. During a recent thunderstorm, the Butterfields' Honda Accord received $2,300 in damage from hail. How much will their PAP pay for this claim? $0 b. $2,050 C. $2,200 d. $2,300 9. Haley is worried that her oldest son, Troy, will be without health insurance after he graduates from college in a few years. Which of the following are realistic insurance options for Troy once he graduates? Extend his current coverage through a COBRA extension II. Purchase insurance through an offshore Asian state-sponsored high risk I. pool III. Purchase insurance through a private company a I only b I and II only c I and III only d. II and III only e I. II. and III 10. Which of the following risk management recommendations are most appropriate to help the Butterfields manage their risk exposures? I. Purchase an excess liability insurance policy II Decrease their homeowner's coverage to 80% of the home's value AaBbCcDa AaBbCel AaBbCel AaBbC1 AaBbCcl AaBbc Emphasis 1 Heading 1 1 Heading 2 1 Heading 3 1 Heading 4 1 Headin Paragraph Styles 10. Which of the following risk management recommendations are most appropriate to help the Butterfields manage their risk exposures? I. Purchase an excess liability insurance policy II. Decrease their homeowner's coverage to 80% of the home's value III. Eliminate collision coverage on the Toyota IV. Purchase an endorsement to cover their art collection a. I and III only b. II and IV only c. II and III only d. I and IV only 11. Which of the following strategies can the Butterfields use to increase their current discretionary cash flow situation? a. Increase the deductible in their PAP policy. b. Purchase an umbrella liability insurance policy. c. Decrease the deductible in their HO policy. d. All of the above. 12. The Butterfields are not sure if they are paying an appropriate premium for their universal life insurance policy. Which statement shown below is true in relation to this concern? a. The universal life policy is fairly priced according to the Yearly Price per Thousand formula. b Even though the Yearly Price per Thousand formula states that the policy is over priced, given Haley's health status, she should hold the policy because she probably will not qualify for another policy. c. Even though the universal policy is expensive, they should not replace it because the cost is less than two times the Yearly Price per Thousand formula benchmark price: Haley should replace the universal policy because, according to the Yearly Price per Thousand formula, the cost is more than two times the benchmark price d. 13. Haley would like to know the difference between variable life insurance and 1 life insurance Which of the following statements A cl AaBbc Emphasis 1 Heading 1 1 Heading 2 T Heading 3 1 Heading 4 1 Headir Paragraph Styles 13. Haley would like to know the difference between variable life insurance and universal life insurance. Which of the following statements is most accurate in describing the difference? a. Variable life insurance uses sub-contracts that are invested to generate a guaranteed rate of return. b. Universal life insurance uses a fixed mortality charge, while variable life insurance does not. c. Variable life insurance has a death benefit that varies, while universal life insurance only provides a fixed death benefit. d. Universal life insurance provides a crediting rate based on the insurance company's general account subject to a minimum guarantee, while variable life insurance uses sub-accounts that can fluctuate based on market returns. 12A ALT AaBbCcDa AaBbCcl AaBbCcl AaBbci AaBbCcl Emphasis 1 Heading 1 1 Heading 2 1 Heading 3 1 Heading 4 Font Paragraph Styles 14. Which of the following statements best describes the Butterfields' disability insurance need at this time? I. John has adequate long-term disability coverage II. John does not have adequate short-term disability coverage III. Haley does not need disability coverage at this time IV. John has adequate short-term disability coverage a. II only b. I and IV only c. II and III only d. II and IV only Discussion Points and Questions (Please create a separate Word document to answer each of these questions) Briefly summarize the relevant facts of the case relating to insurance planning to purchase additional life insurance what type 2. If the Butterfields were going to purchase additional life insurance what type of policy, what face value, and what riders would be most appropriate given their age and need? 3. Explain the advantages and disadvantages of having John purchase additional life insurance through his employer. 4. Describe the 80% co-insurance rule and report to the Butterfields how this rule affects their homeowner's coverage. 5. What actions can the Butterfields take to reduce their insurance premiums while maintaining adequate coverage in terms of liability and property coverage? 6. Explain why the Butterfields should consider purchasing an excess liability insurance policy Describe the purpose of long-term care insurance and indicate if and when the Butterfields should consider purchasing this type of insurance. 7. 8. Report on the advantages and disadvantages associated with the Butterfields current health insurance policy

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts