Answered step by step

Verified Expert Solution

Question

1 Approved Answer

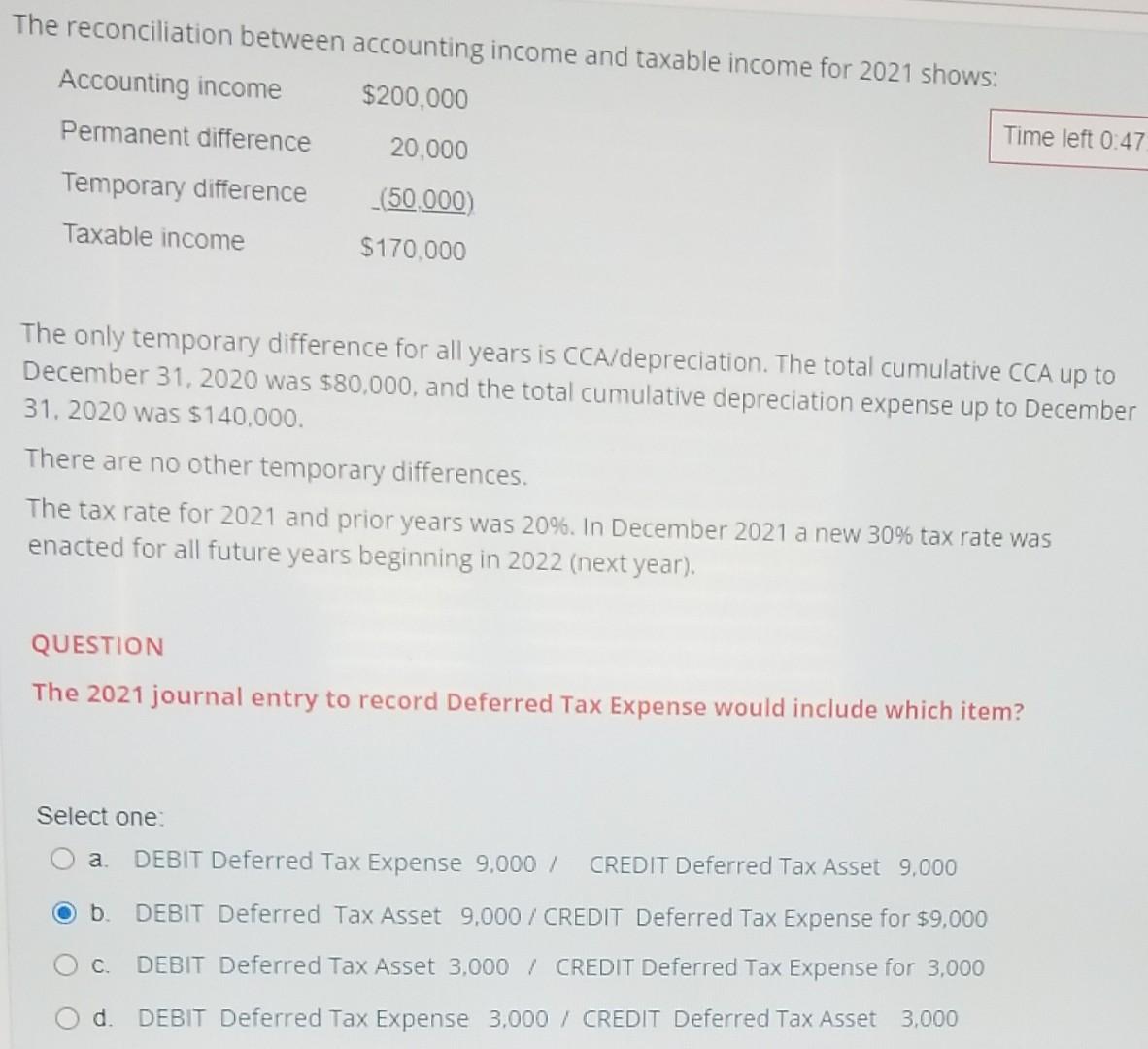

The reconciliation between accounting income and taxable income for 2021 shows: Accounting income $200,000 Time left 0:47 Permanent difference 20.000 Temporary difference _(50.000) Taxable income

The reconciliation between accounting income and taxable income for 2021 shows: Accounting income $200,000 Time left 0:47 Permanent difference 20.000 Temporary difference _(50.000) Taxable income $170.000 The only temporary difference for all years is CCA/depreciation. The total cumulative CCA up to December 31, 2020 was $80,000, and the total cumulative depreciation expense up to December 31. 2020 was $140,000. There are no other temporary differences. The tax rate for 2021 and prior years was 20%. In December 2021 a new 30% tax rate was enacted for all future years beginning in 2022 (next year). QUESTION The 2021 journal entry to record Deferred Tax Expense would include which item? Select one: . DEBIT Deferred Tax Expense 9,000 / CREDIT Deferred Tax Asset 9.000 . DEBIT Deferred Tax Asset 9,000/ CREDIT Deferred Tax Expense for $9,000 C. DEBIT Deferred Tax Asset 3.000 / CREDIT Deferred Tax Expense for 3,000 d. DEBIT Deferred Tax Expense 3.000 / CREDIT Deferred Tax Asset 3,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Just Leave Me Alone Audit Clerk Knows What To Do Blank Lined Journal Funny Auditor Gifts For Women Men Funny Gift For Auditor Fun Finance Gifts An Auditor Who Loves Accounting And Auditing

Authors: Awesome Auditor

1st Edition

1659112699, 978-1659112696