Answered step by step

Verified Expert Solution

Question

1 Approved Answer

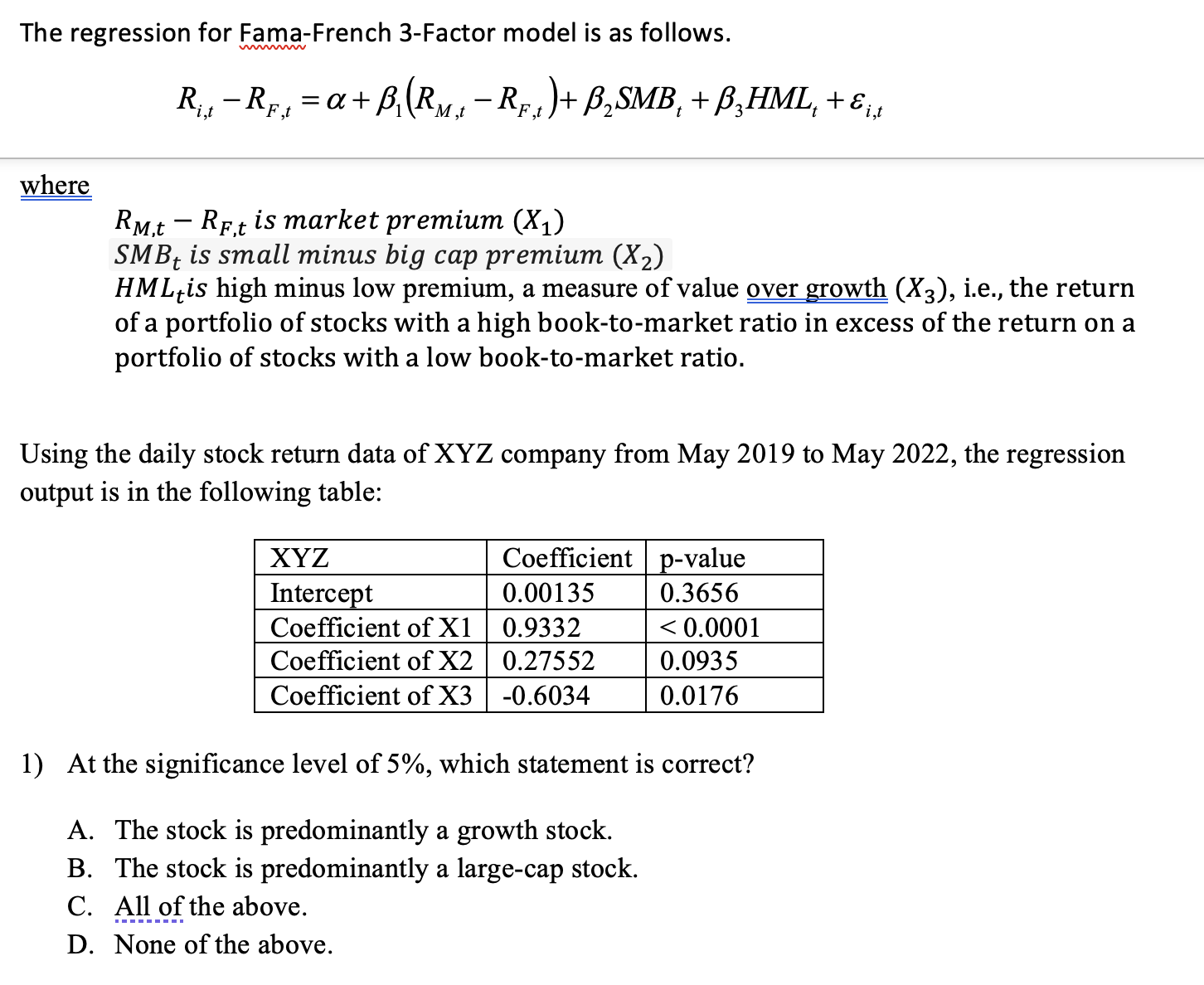

The regression for Fama-French 3-Factor model is as follows. where R - RF = a + (RM - R )+ SMB + HML +&

The regression for Fama-French 3-Factor model is as follows. where R - RF = a + (RM - R )+ SMB + HML +& i,t F,t F,t RM, RE,t is market premium (X) SMB, is small minus big cap premium (X) HML is high minus low premium, a measure of value over growth (X3), i.e., the return of a portfolio of stocks with a high book-to-market ratio in excess of the return on a portfolio of stocks with a low book-to-market ratio. Using the daily stock return data of XYZ company from May 2019 to May 2022, the regression output is in the following table: XYZ Intercept Coefficient of X1 Coefficient of X2 Coefficient of X3 Coefficient p-value 0.3656

Step by Step Solution

There are 3 Steps involved in it

Step: 1

The detailed answer for the above question is provided below To determine which statement is correct ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Finance

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe

10th edition

978-0077511388, 78034779, 9780077511340, 77511387, 9780078034770, 77511344, 978-0077861759