Answered step by step

Verified Expert Solution

Question

1 Approved Answer

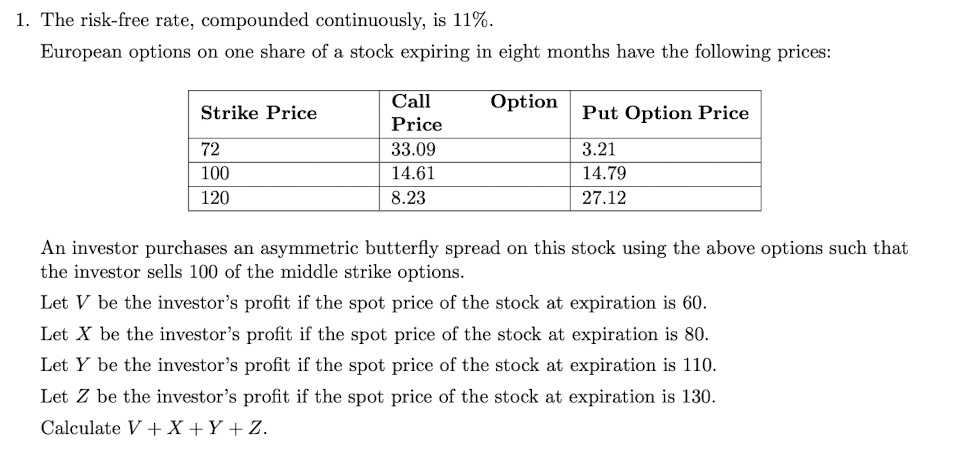

The risk - free rate, compounded continuously, is 1 1 % . European options on one share of a stock expiring in eight months have

The riskfree rate, compounded continuously, is

European options on one share of a stock expiring in eight months have the following prices:

An investor purchases an asymmetric butterfly spread on this stock using the above options such that

the investor sells of the middle strike options.

Let be the investor's profit if the spot price of the stock at expiration is

Let be the investor's profit if the spot price of the stock at expiration is

Let be the investor's profit if the spot price of the stock at expiration is

Let be the investor's profit if the spot price of the stock at expiration is

Calculate

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis For Financial Management

Authors: Robert C. Higgins

5th Edition

0256167036, 9780256167030